2150

Views

196

Downloads |

Leading indicators of financial stress in Croatia: a regime switching approach

Tihana Škrinjarić*

Article | Year: 2023 | Pages: 205 - 232 | Volume: 47 | Issue: 2 Received: June 1, 2022 | Accepted: November 21, 2022 | Published online: June 12, 2023

|

FULL ARTICLE

FIGURES & DATA

REFERENCES

CROSSMARK POLICY

METRICS

LICENCING

PDF

|

Category

|

Variables

|

Transformations

|

|

Credit

dynamics

|

Narrow and

broad credit

Narrow and broad credit-to-GDP ratio

Household (HH) credit

Non-financial corporations (NFC) credit

HH credit-to-GDP ratio

NFC credit-to-GDP ratio

(nominal and real variants of credit)

|

1YG

1YC

|

A2YG

A2YC

|

HP gap

25K

85K

125K

400K

|

|

Potential

overvaluation of property prices

|

House price

index (nominal and real)

Price to rent ratio (nominal and real)

Price to income ratio (nominal and real)

Price to cost ratio (nominal and real)

Construction work index ratio

Indicator of overvaluation of property prices

|

1YG

1YC

|

A2YG

A2YC

|

HP gap

1600

25K

85K

125K

400K

|

|

External

imbalances

|

Gross

external debt (GED)

Net external debt (NED)

GED-to-GDP ratio

NED-to-GDP ratio

Terms of trade

Current account to GDP ratio

Net export to GDP ratio

|

1YG

1YC

|

A2YG

A2YC

|

HP gap

1600

25K

85K

125K

400K

|

|

Strength of

bank balance sheets

|

Deposit to

credit ratio

Capital to assets ratio

Assets to GDP ratio

|

1YG

1YC

|

A2YG

A2YC

|

HP gap

1600

25K

85K

125K

400K

|

|

Private

sector debt burden

|

Debt service

ratio (household and nonfinancial corporations separately)

Total debt to income ratio

Total debt to gross operating surplus ratio

|

1YG

1YC

|

A2YG

A2YC

|

HP gap

25K

85K

125K

400K

|

|

Mispricing of

risks

|

Stock market

index CROBEX

HH credit interest rate margin8

NFC credit interest rate margin

Bank prudence indicator8

|

1YG

1YC

|

A2YG

A2YC

|

HP gap 1600

25K

85K

|

Source: CNB (2022).

Source: CNB (2022) and author’s calculation (for probabilities).

wertzd

|

Parameter/values

|

Regime

1

|

Regime

2

|

|

Constant

|

0.1718

(0.014)***

|

0.0657

(0.006)***

|

|

Variance

|

0.0081

(0.005)*

|

0.0004

(0.000)***

|

|

βij

|

0.7912

(0.149)***

|

0.0385

(0.027)

|

|

AR(1)

|

0.7351

(0.110)***

|

|

AR(2)

|

-0.2186

(0.102)**

|

|

AIC

|

-247.566

|

|

Log L

|

131.873

|

|

RCM

|

14.776

|

Note: β ij is the estimated parameter for constant governing the regime switching in eq. (3). AIC and Log L denote the Akaike information criterion and log likelihood value respectively. Values in parentheses denote standard error of the estimator. *, ** and *** denote statistical significance at 10%, 5% and 1% respectively. Source: Author’s calculation.

Note: Shaded areas denote 95% confidence interval for the median value. “balance sheets”, “burden”, “credit”, “external”, “house” and “mispricing” denote the six categories of measures from table 1: strength of balance sheets, private sector debt burden, credit dynamics, external imbalances, potential overvaluation of house prices and mispricing of risks respectively. t_4, t_5, t_6 and t_7 denote models that include indicator variables lagged for 4, 5, 6 and 7 quarters respectively. Source: Author’s calculation.

Note: Shaded areas denote 95% confidence interval for the median value. “balance sheets”, “burden”, “credit”, “external”, “house” and “mispricing” denote the six categories of measures from table 1: strength of balance sheets, private sector debt burden, credit dynamics, external imbalances, potential overvaluation of house prices and mispricing of risks respectively. t_4, t_5, t_6 and t_7 denote models that include indicator variables lagged for 4, 5, 6 and 7 quarters respectively. Source: Author’s calculation.

Note: “balance sheets”, “burden”, “credit”, “external”, “house” and “mispricing” denote the six categories of measures from table 1: strength of balance sheets, private sector debt burden, credit dynamics, external imbalances, potential overvaluation of house prices and mispricing of risks respectively. t_4, t_5, t_6 and t_7 denote models that include indicator variables lagged for 4, 5, 6 and 7 quarters respectively. Source: Author’s calculation.

|

Indicator

|

t-7

|

t-6

|

t-5

|

t-4

|

|

HPI 2y growth

rate

|

0.187

|

0.164

|

0.152

|

0.163

|

|

HPI real, gap

25K

|

0.176

|

0.130

|

0.131

|

0.161

|

|

Capital/Assets,

gap 1600

|

0.147

|

0.100

|

0.130

|

0.119

|

|

CNFP real 1y

change

|

0.072

|

0.091

|

0.171

|

0.131

|

|

Basel gap,

25K

|

0.277

|

0.238

|

0.381

|

0.456

|

|

Broad credit

1y change

|

0.069

|

0.075

|

0.066

|

0.071

|

|

Broad credit

real 1y change

|

0.046

|

0.050

|

0.044

|

0.047

|

|

Narrow credit

gap, 125K

|

0.654

|

0.748

|

0.740

|

0.689

|

|

Narrow credit

gap, 25K

|

0.740

|

0.833

|

0.836

|

0.777

|

|

Narrow credit

gap, 400K

|

0.645

|

0.737

|

0.727

|

0.675

|

|

Narrow credit

gap, 85K

|

0.663

|

0.757

|

0.754

|

0.705

|

|

|

|

|

|

|

|

CNFC 2y

growth rate

|

0.128

|

0.139

|

0.156

|

0.147

|

|

H D-to-I 2y

change

|

0.019

|

0.018

|

0.019

|

0.016

|

|

CNFC, 25K

|

0.185

|

0.181

|

0.187

|

0.163

|

|

P-to-Income,

400K

|

0.110

|

0.055

|

0.143

|

0.165

|

|

Deposits/Credit,

1600

|

0.019

|

0.018

|

0.020

|

0.023

|

|

HPI real 1y

growth rate

|

0.149

|

0.150

|

0.177

|

0.187

|

|

P-to-I 2y

growth rate

|

0.190

|

0.181

|

0.198

|

0.231

|

|

P-to-I real

2y growth rate

|

0.164

|

0.171

|

0.199

|

0.238

|

|

Narrow credit

1y growth rate

|

0.149

|

0.175

|

0.230

|

0.268

|

|

Narrow credit

2y growth rate

|

0.149

|

0.175

|

0.230

|

0.268

|

|

NX, cumsum

|

0.407

|

0.359

|

0.321

|

0.311

|

|

Net ext debt,

125K

|

0.332

|

0.310

|

0.404

|

0.332

|

|

Net ext debt,

25K

|

0.310

|

0.404

|

0.332

|

0.332

|

|

Net ext debt,

400K

|

0.332

|

0.310

|

0.404

|

0.332

|

|

Net ext debt,

85K

|

0.332

|

0.310

|

0.404

|

0.332

|

|

NX

|

0.327

|

0.291

|

0.301

|

0.392

|

|

HH 1y change

|

0.509

|

0.294

|

0.300

|

0.556

|

Note: 1600, 25K, 85K, 125K and 400K denote the value of the smoothing parameter in HP gap, in values of 1,600, 25,000, 85,000, 125,000 and 400,000 respectively. 1y and 2y are one and two years, CNFP is credit to nonfinancial corporations, HPI is house price index, Capital/Assets is the capital-to-assets ratio. t-4, t-5, t-6 and t-7 denote models that include indicator variables lagged for 4, 5, 6 and 7 quarters respectively. HH denotes credit to households, Net ext debt denotes net external debt, NX is net exports share in GDP, whereas NX cumsum is sum of net exports over 4 quarters share in sum of GDP over 4 quarters, P-to-I is the price to income ratio, HPI is house price index, Deposits/Credit denotes the deposit-to-credit ratio, P-to-Income is house price-to-income ratio, CNFC is credit to nonfinancial corporations, H D-to-I is household debt to income ratio. Source: Author’s calculation.

|

AR/MA

|

0

|

1

|

2

|

3

|

|

0

|

-1.964473

|

-2.521833

|

-2.679371

|

-2.664269

|

|

1

|

-2.591213

|

-2.672851

|

-2.653948

|

-2.597705

|

|

2

|

-2.683885

|

-2.638946

|

-2.603793

|

-2.553256

|

Source: Author’s calculation.

Note: “balance sheets”, “burden”, “credit”, “external”, “house” and “mispricing” denote the six categories of measures from table 1: strength of balance sheets, private sector debt burden, credit dynamics, external imbalances, potential overvaluation of house prices and mispricing of risks respectively. t_4, t_5, t_6 and t_7 denote models that include indicator variables lagged for 4, 5, 6 and 7 quarters respectively. Source: Author’s calculation.

|

|

|

Abstract

This research focuses on the prediction of the probability of (re)entering high financial stress (via a large set of cyclical risk accumulation indicators). The focus is placed on a specific single-country analysis to obtain answers to questions about which indicators are best in explaining the future probability of (re)entering a high-stress regime. This allows the policymaker to get a better focus on the best-performing variables. It is challenging to monitor a whole set of indicators of cyclical risk build-up; the results could bring into focus a smaller group of the essential variables. The contribution of this paper is in finding a set of indicators that help in forecasting financial stress, in terms of switching from one regime to another. The regime-switching models’ results indicate that some credit specifications, house price dynamics, and debt burden could be best monitored for the case of Croatian data.

Keywords: financial stress; macro-prudential policy; Regime-switching models; Croatia

JEL: C54, G01, G15

1 Introduction

Macroprudential policy has the difficult task of identifying sources of financial system instability alongside detecting appropriate indicators to measure the accumulation of systemic risks. Timely and high-quality measures and instruments can then be devised and put into action so that the potential risks are mitigated, and the adverse effects that risk materialization causes to the rest of the real economy are reduced. That is why much research today focuses on quantifying the build-up of vulnerabilities in the financial system, as well as on quantifying risk materialization in the forms of financial stress that occurs in the system itself. One goal is to predict the turning points of a financial cycle or financial crisis and another is to measure the state of the financial system’s instability. The amount of literature that focuses on one or the other important aspects has grown in the last decade as macroprudential policy has developed. However, there is still a lack of research linking the build-up of vulnerabilities to the risk materialization approach. This paper tries to fill that gap. The research has endeavoured to combine the two approaches in order to try to evaluate the potential predictability of risk materialization measured via the financial stress indicator, based on the indicators that are preferred in EWS (early warning system) models. The first paper to attempt this was that of Duprey and Klaus ( 2017), in which a potential is seen in combining the best of both approaches. Thus, this research applies the regime-switching methodology of modelling the financial stress indicator for Croatia, to evaluate predictive possibilities of a number of indicators usually used in the EWS approach to the build-up of financial system vulnerabilities. 2017), in which a potential is seen in combining the best of both approaches. Thus, this research applies the regime-switching methodology of modelling the financial stress indicator for Croatia, to evaluate predictive possibilities of a number of indicators usually used in the EWS approach to the build-up of financial system vulnerabilities.

The main contribution of this study is in its identification of finding a set of indicators that help forecast financial stress, switching from one regime to another, while utilizing techniques to reduce their number. This study observes many different variables and their transformations in order to find the best ones. This allows the policymaker to focus on the variables that were found to be best in the modelling process. It is challenging to monitor a whole set of indicators of cyclical risk buildup but the results of this research could bring into clear focus a smaller group of essential variables. Furthermore, most existing research focuses on predicting the value of future stress and concludes that it is challenging to predict stress levels. However, as Christensen and Li ( 2014) point out, the decision-making process should rely on point forecasts and insights into the likelihood of the occurrence of the stress event. That is why this study focuses on estimating the effects of the dynamics of indicators on the future probability of entering a stress event, which is rarely found in the literature; to the knowledge of the author, the only other existing study framed in such terms is Duprey and Klaus ( 2017; 20222). Furthermore, an extensive analysis is made of over several hundred variants of indicators of cyclical risk accumulation. In that way, the quality of regime-switching models is examined in a fashion that has never been accomplished previously (to the author’s knowledge). Namely, the usual criteria used in the model comparison are contrasted over six categories of measures, for four different lags of the indicators, with a particular focus on the empirical distributions of the results. This enables the policymaker to determine the characteristics of each category for every lag. Moreover, those individual variables that were found to be the best in adding relevant information to the model are used in a simple simulation, involving the construction of a composite indicator of risk accumulation that can be used to monitor financial cycle dynamics.

There are a couple of reasons why we focus on the regime-switching approach: Croatian data, and the combination of both approaches. First, regime-switching models have been extensively used and found to be useful in modelling business cycles (see, e.g. Doz, Ferrara and Pionnier, 2020) and financial markets (Ang and Timmermann, 2012) 1. Furthermore, research has found that the interaction between financial stress and the real economy is not linear. Quite the opposite, the relationship is asymmetric and exhibits nonlinear behaviour, as seen in Giglio, Bryan and Pruitt ( 2016), Cardarelli, Elekdag and Lall ( 2011), or O’Brien and Wosser ( 2021). Moreover, Vermeulen et al. ( 2015) show that spikes in financial stress occur abruptly. Finally, Misina and Tkacz ( 2009) think that nonlinear models are more suitable for capturing the asymmetry in the behaviour of financial market participants. Thus, regime-switching models capture the nonlinearities and asymmetric behaviour that cannot be adequately modelled via linear models. Another important issue is that forecasting future crises does not rely solely on the value of a variable (i.e. the value of the stress indicator itself). Still, the probability of crisis occurrence is also important (Gneitinga and Ranjanb, 2011) and it is more important when making policy decisions. Next, Croatian data are observed as this area of macroprudential policy practice is not sufficiently explored for this country. On the other hand, the country has known an extensive macroprudential approach over the last two decades 2. There exist just a few related papers regarding the Croatian financial system: Dumičić ( 2015a), where the financial stress indicator is constructed for the first time for the Croatian case; Duraković ( 2021) upgraded the stress indicator in the approach of Holló, Kremer and Lo Duca ( 2012) and its interaction with the real economy was tested and found to be significant and asymmetric; and Dumičić ( 2015b), where the first attempt at constructing a composite indicator of cyclical systemic risk accumulation was made. Countries with an economy similar to the Croatian could thus acquire some insight into potential outcomes regarding their financial systems.

Although researchers are often prejudiced against single country analysis, there is actually a potential in focusing on one system, as compared to panel data analysis. For example, Klomp ( 2010) examined 110 different countries and found heterogeneity in the causes of banking crises, alongside an overview of previous related research that found different variables to be significant in predicting future crises, alongside different estimated signs. Although panel analyses are very important due to their advantages over single-country analysis, countries cannot copy measures and instruments one from another directly due to country specificities. In fact, previous research that focused on early warning systems of crises has often incorporated country-specific analysis: Kaminsky and Reinhart ( 1999) estimate country-specific thresholds in minimizing the noise-to-signal ratio in the modelling process. There are significant differences between the country-specific and global thresholds in the EWS results found in Davis and Karim ( 2008), who, focusing on banking crises conclude that generalized global models cannot replace country specific macroprudential surveillance.

2 Literature review

The first group of research that focuses on the build-up of vulnerabilities in the financial system is focused on exploring the possibilities of predicting turning points of the financial cycle. The rise of interest in forecasting financial crises has risen especially after the GFC (Global Financial Crisis), due to the severe consequences it entailed for the rest of the real economy. Early-warning systems became very popular, as their purpose is to give an early enough warning of a turning point in the financial cycle (Reinhart and Rogoff, 2009). Here, the idea is to evaluate individual or group possibilities in signalling a future crisis of selected variables that should capture the changes in the accumulation of cyclical systemic risk. Empirical work has focused on the six categories of measures of the build-up of system-wide risk as recommended in ESRB (2014). The best predictors of previous crises are closely observed in the practices of central banks to make decisions about macroprudential instruments to mitigate systemic risks, with a special focus on cyclical systemic risk. For example, some central banks utilize from 6 to 35 individual indicators (Arbatli-Saxegaard and Muneer, 2020), with many of them monitoring over 20 indicators when making decisions about the countercyclical capital buffer. Thus, one strain of literature has focused on defining a binary variable depending on the definition of financial, banking, currency, or related crises dates (based on the criteria in ESRB, 2018; ECB, 2017; and Dimova, Kongsamut and Vandenbussche, 2016). The EWS approach is, thus, based on predetermined dates of crisis or non-crisis state in the financial system, and the idea is to evaluate the signalling properties of potential indicators regarding the binary variable defining a vulnerable period before a crisis happens.

The second group of works in the literature concerned with monitoring systemic stress is focused on the composite indicator of financial stress. An influential paper by Holló, Kremer and Lo Duca ( 2012) has opened a path to measuring the realization of risks in financial markets. Here, the composite indicator indicates the current state of instability of the financial system, together with the frictions and strains affecting it. Holló, Kremer and Lo Duca ( 2012) state that such a measure is helpful in determining episodes of financial crises. This means that the realizations of the stress captured in the financial stress indicator can be utilized to estimate the crisis and non-crisis states of the system, as well as corresponding dates. This is useful due to previous research having found evidence of the negative effects of financial stress on the economic activity (Borio and Drehmann, 2009; Bloom, 2009; Hubrich and Tetlow, 2015; Chavleishvili and Manganelli, 2019; Dumičić,, 2015a; and an overview in Škrinjarić, 2022), which is especially true for the downside risks of economic growth (e.g. Adrian, Boyarchenko and Giannone, 2019; and a general overview in Plagborg-Moller et al., 2020) 3.

Misina and Tkacz ( 2009) utilize a linear and threshold regression approach in forecasting the FSI (financial stress index) based on values in k (= 1 to 12) periods ahead of selected indicators. The empirical part of their research focused on Canadian data on credit developments, asset prices, GDP, and crude oil prices (various definitions of variables, with quarterly and yearly growth rates). Forecast quality was contrasted among all different variants of considered models, with horizons of k = 4 and 8 being the best for credit and asset price variables. Another single-country analysis is found in Hanschel and Monnin ( 2005), where the authors model stress in the banking sector of Switzerland. 13 OECD countries are examined in Slingenberg and de Haan ( 2011), in which the authors in a fashion similar to the models in Misina and Tkacz ( 2009) observe the predictive power of similar variables. The main findings include that credit growth has some predictive power for most of countries, but other variables are significant for some countries and not for others. This also goes in favour of single country analysis. Lo Duca and Peltonen ( 2011) define a stress event when the stress variable exceeds its 90-th percentile value in the analysis, and then construct a binary variable depending on this value. The EWS approach was done here as well, in which in total 28 countries were observed. Asset prices and credit developments were found to be the best predictors of future crises. A signal extraction approach was made in Christensen and Li ( 2014), where 13 OECD countries were observed in understanding the behaviour of selected economic indicators preceding financial stress. However, a financial stress event is defined via a subjective selection of a threshold value that is between some values used in related approaches 4. Vašiček et al. ( 2017) observed 25 OECD countries in the BMA (Bayesian model averaging) approach in determining the leading indicators of financial stress. Here, the authors obtain the following results: the panel approach does not yield good results in terms of successful prediction of future FSI movements; country-level analysis produces better results; and in general, FSI movements are hard to predict, as out of sample predictions are worse than in-sample analysis. Pietrzak ( 2021) has compared several approaches to predicting financial distress for 43 countries, in the period 1990 to 2016. Thus, this is not an analysis methodologically comparable to this one, but the results are interesting, as the results show that specific variables such as capital adequacy, leverage, and return on assets predict future financial distress 5. Duprey and Klaus ( 2017; 20222) is the closest study to this one, the authors evaluating 27 indicators for 15 EU countries and in the unbalanced sample from Q1 1970 to 4Q 2018 analysing the potential of the binary-logit model and the regime-switching approach. The main results indicate that the debt service ratio, credit dynamics, and property market variables are useful in predicting higher financial stress periods. The analysis that included post-GFC data was better than the pre-GFC one. Based on these results, the authors concluded that before the GFC, it was more difficult to predict the future movement of the financial stress probabilities.

Dumičić ( 2015a) has constructed an earlier version of a financial stress indicator (FSI) for Croatia. In the second phase of the research, FSI indicators were used in a regime-switching model to see their performance in boom and bust phases, alongside the sources of risk increases during regimes of more stress. Based on an extensive analysis of higher and lower stress sub-periods, the author concluded that the FSIs defined in this paper are a good starting point for use in practice. Duraković ( 2021) is a newer variant of a composite indicator of systemic stress. The author followed the Holló, Kremer and Lo Duca ( 2012) approach in constructing the indicator with some specifics for Croatian data. In this work, the author observed the threshold VAR model in estimating the effects of higher or lower financial stress on real economy growth. Asymmetric findings confirm the aforementioned nonlinearities in the introduction. Compared to the previous two papers, this paper looks beyond current realizations of financial stress in the financial markets in Croatia. Here, we observe the information obtained from MRS models regarding the effects of cyclical risk indicators that could have affected switching from one regime to another. This gives the policymaker some insights into the possibility of affecting those indicators via certain measures or instruments, which could, in turn, reduce future financial stress.

Generally speaking, after reviewing the related literature, it seems reasonable to analyse the effects of early warning indicators on the probability of future higher or lower stress, as the value of the stress variable is hard to predict. However, the selected indicators were found useful in the early warning literature, regarding the signalling approach to future crisis modelling. Variables utilized in this study are based on the literature within this group of papers.

3 Data and methodology description

3.1 Data description

Quarterly data on the following six (according to the ESRB (2014) Recommendation) categories of measures of cyclical risk build-up have been collected from CNB (2022a): credit dynamics, potential overvaluation of property prices, external imbalances, the strength of bank balance sheets, private sector debt burden and potential mispricing of risks. As the availability of data varies depending on the variable category (or even within the category itself), to produce comparability of the estimation results, all of the variables after the initial transformations were brought to the same initial starting point of 4Q 2005. The last available data are for 3Q 2021. Although this results in a short timespan dataset, future work should focus on this issue. Besides the indicators, values on HIFS6 (Croatian indicator of financial stress) have been collected from internal CNB calculations, and quarterly averages were calculated for the HIFS levels. This indicator is in line with the methodology of Holló, Kremer and Lo Duca (2012) and is described in detail in Duraković (2021). Table 1 gives an overview and description of the variables used in the study alongside the data transformations. Every category consists of transformed variables in terms of one-year growth rates or differences, annualized growth rates or changes, and the HP (Hodrick-Prescott, 1997) gap.

The smoothing parameter values in the filtering were based on previous studies of the length of the financial cycle. For example, Galán ( 2019) finds that the value of 25.600 for the smoothing of the credit-to-GDP gap parameter is better in the signalling the future crisis, whereas Wezel ( 2019) found that CEE (Central and Eastern Europe) countries have shorter credit cycles, which is also in favour of a smaller smoothing parameter. Furthermore, other studies utilize the values of 85,000, 125,000, and 400,000 for the smoothing parameter in the HP filtering, as the length of the financial cycle is assumed to be 2 to 4 times longer than the business cycle: Drehmann et al. ( 2010) focused on OECD countries and higher values of the parameter, whereas Galati et al. (2016) for 5 eurozone countries conclude that their financial cycle lasts between 8 and 25 years. Moreover, Schüler ( 2018), in his empirical analysis, concludes that the value of 400.000 for the smoothing parameter in the ESRB ( 2014) Recommendation could result in omitting relevant fluctuations in relevant financial series. Thus, based on these mixed results, this study allows for different smoothing parameters in the HP filtering process.

Furthermore, it should be noted that the decision-making process of the policymaker is in real-time, meaning that all of the filters are calculated recursively, i.e. as one-sided gaps. Smaller values of the smoothing parameters are related to the assumption of a shorter length of the financial cycle or the fact that some variables could be linked more to the business cycle (parameter 1,600). In total, 241 different variables are examined in the study. All variables are interpreted in such a way that the greater the value, the greater the risk accumulation. This means that some variables were multiplied with value -1 to provide such interpretation (e.g. interest rate margins, net exports, etc.).

Table 1Brief description of variables used in the study DISPLAY Table

3.2 Methodology of regime switching

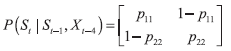

The basic approach of the present research is to observe how different measures of risk accumulation affect the future probability of transitioning from one regime to another regarding the financial stress variable. Thus, the Markov regime switching models (MRS) are the most appropriate, and we follow the usual literature in the brief description of MRS (Gray, 1996; Kim, 1994; Franses and van Dijk, 2000). It is assumed that the financial stress variable (HIFS) is defined via the following data generating process (DGP): | HIFSt= ai + φHIFSt-1 + εi,t, i ∈ {1, 2}, εi,t ~ N(0,σi2) | (1) |

| (2) |

| (3) |

is the one-step-ahead probability of entering regime j in period t from regime i in period t-1, Xt-4 is a vector of variables that determine the switching behaviour between the two regimes, as in Duprey and Klaus ( 2017; 20222). In practice, X will be one variable as an indicator in testing its predictive probability of future shifts between the low and high regime of the financial stress variable. The selection of lag 4 quarters in practice for the variable X is explained in Duprey and Klaus ( 2017; 20222) as being consistent with data that the financial stress, conditional on the shift in regimes, does not depend on Xt-4 beyond the information contained in the shift in the regime. Moreover, it can be added that the variables used as X are usually published with lags. This means that using t-1 or t-2 periods ahead does not make sense, as the stress realization in quarter t would be documented before the data on Xt-1 or Xt-2 were available. On the other hand, the idea of using variables in X is founded on the early warning model (EWM) literature, which finds that such variables should signal the future turning point of the financial crises or cycle from 12 to 5 quarters ahead (ECB, 2017). Longer horizons such as 12 quarters ahead are proven to have low forecasting power (see Misina and Tkascz, ( 2009). Finally, short time series such as the Croatian data cannot afford to observe long horizons, due to data loss at the beginning of the sample. Vašíček et al. (2017) add that there needs to be a balance between the informative criterion (information provided in a variable declines with a longer forecast horizon) and the criterion of allowing for timely policy action. Finally, several other lags will be considered in the empirical analysis, t-5, t-6 and t-7.

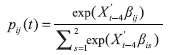

When estimating the switching model, we will observe the estimated signs and significance of betas in equation (3). If we denote regime 1 as being the more stressful (a greater value of the variance as well as a greater average value of the stress series), positive significant betas corresponding to the indicator variables that are tested in the analysis indicate that their greater values increase the probability of transitioning from the less risky to riskier regime; and increasing the probability of staying in the same riskier regime as well. The model is estimated via the usual approach of the likelihood maximization of the function where the HIFS value is estimated with respect to given information I in the previous period, alongside the information about being in regime i, to estimate unknown parameters in θ f( HIFSt | It-1, Δ t = i; θ) = P( HIFSt | It-1, Δ t = i; θ), where θ = ( β(Δ), pij, σi2). The log likelihood function is defined as the sum of log values of probabilities P( HIFSt | It-1, Δ t = i; θ) for every regime. As it is unknown what the true regime is in period t-1, true probabilities to be estimated are unknown. Thus, the inferential and smoothed probabilities are estimated recursively as in the definition of Gray ( 1996). It should be noted that the decision-making process is in real time, which means that smoothed probabilities are not available in such a scenario. Thus, the macroprudential policymaker is observing the one-step-ahead probability and eventually filtered.

4 Empirical results

4.1 Initial results

Firstly, the Box-Jenkins approach was made in determining the adequate ARMA(p,q) model for the HIFS variable behaviour. Table A1 in the appendix depicts the Schwartz information criterion table, where the AR(2) model is chosen as the best one. Thus, the rest of the analysis will be made according to this model specification. Figure 1 depicts the dynamics of the stress variable HIFS in the observed period (solid black curve), with the one-step-ahead and filtered probabilities of being in the regime of higher stress (grey curves). These probabilities are estimated according to a two-regime model, in which it is assumed that the average value of the HIFS and the variance of the error term are regime dependent. The AR terms are assumed to be non-regime dependent. The corresponding estimated model is shown in table 2 and it will be the basis for comparisons with its extensions with the risk build-up variables. Other model specifications were estimated and contrasted against the one given in table 2, in terms of the information criterion, log-likelihood, and Wald test for parameter equality over the regimes. It was found that this is the best specification of the DGP of HIFS if it is assumed that it follows a regime-switching process. Ang and Bekaert (2002a; 2002b) defined RCM (regime classification measure) to quantify how well the regime-switching model classifies the regimes. It is calculated as follows: | (4) |

where K is the number of regimes in the model, T is the number of observations, pit is the smoothed probability of being in regime i at time t. The value is between 0 and 100, and the closer to zero it is, the better the classification of the regimes. The value is given in table 2, alongside other results.

Firstly, figure 1 indicates that the regime-switching approach successfully captures the dynamics in the stress variable. The reactions of financial markets when the GFC, the EU sovereign debt crisis hit, and other impactful events, such as the COVID-19 crisis are pronounced in the dynamics. Moreover, the probability of being in the regime of higher stress is greater for the two aforementioned crises, whereas turbulences in 2014-2015 and the COVID-19 crisis were characterized by lower values of the high-stress probability. This indicates that the regime-switching approach is appropriate for such analysis 9 . The results in table 2 also provide insights into the baseline model: the RCM measure is very low, the values of the average HIFS value and its volatility are fairly different and significant in both regimes.

Figure 1HIFS values (left hand side) and the one-step-ahead and filtered probability of being in the regime of higher stress (right hand side) DISPLAY Figure

Table 2Regime switching estimation results for a 2-regime AR(2) model for HIFS DISPLAY Table

4.2 Inclusion of indicator variables results

Next, the baseline model is challenged by including the variables of cyclical risk accumulation in equation (3) of the model to govern the one-step-ahead probability of entering the risker regime (or staying in it). Thus, for every variable in the previous section, the 2-regime AR(2) model is estimated, including the single variable (in some of its transformations from table 1) with a lag of 4, 5, 6, and 7 quarters. That is, 964 models were estimated in total. As not all variables are comparable in terms of their unit of measurement, we first compare the log likelihoods and AIC information criterion across all variables, lags, and their category according to table 1. Figure 2 depicts the box-plots for the mentioned variations for the log likelihood values, and figure 3 does the same, but for the AIC values10. It can be seen that the value of Log L increases as the lag of the indicator variable shortens across all of the categories of measures. This is in line with the EWS research (ESRB, 2018; Lang et al., 2019; Alessi and Detken, 2019; Candelon, Dumitrescu and Hurlin, 2012), where the indicators should show a consistent increase in their value before the peak of the financial cycle occurs and the risk materializes. A more detailed depiction of the values from figure 2 is given in figure A1 in the appendix. A detailed picture of the Log L values across all individual indicators in the regime-switching specification. The best specification is for the t-4 lag case, as the values are greater than the baseline model in most of the cases, and the variability is the smallest for most of the measure categories.Figure 2Box plot for log likelihood values across all 964 models DISPLAY Figure

Figure 2 also shows that the best-performing models are those regarding the credit, house price, and debt burden variable categories. In contrast, external imbalances are those that have the greatest variation of results. This means that in modelling the HIFS regime-switching behaviour, it would be useful to include credit and debt burden variables with a 4-quarter lag. However, the rest of the categories with the exception of the aforementioned external imbalances, are also found to have good Log L values. AIC values in figure 3 tell a similar story (when the same analysis is done on the interquartile range and the average and median values compared to the original model’s value of -247.6). Here, we can also see that for t-7 and t-6, most of the variables have greater AIC values than the baseline model, contributing to the validity of t-4 and t-5 variants.

Figure 3Box plot for AIC values across all 964 models DISPLAY Figure

Not all variables are best performing for the t-4 case, which is seen in figure 4. It observes the empirical density functions of each risk category for all four lags observed in the study. This helps determine which lag could be best for a variable category, or individual variables when deciding which variant it is best to use in practice. This figure tells the following for the credit series as we move from t-7 to t-4, the density function becomes tighter with higher peaks. However, the best performance is found for t-5 for the balance sheets category, as here, most of the observations are above the value of 132, with a high peak, compared to higher peaks of lower values for t-6 and t-7 cases. Other measures have the best performance for t-4 and t-5 for the house prices category; the external and mispricing categories have the worst performances overall, due to high dispersion, especially regarding the left tails.

Figure 4Empirical density functions of log likelihood values across all 964 models DISPLAY Figure

In general, the promising results of models with the inclusion of indicator variables are in line with other studies that analyse some form of non-linear models, such as Davis and Karim ( 2008) and Vašiček et al. ( 2017). To summarize the results, it is evident that the performance of the models gets better when the lag of the indicator variable gets smaller. There is a trade-off, however, as the information about some variables has a certain lag. The results found here are in line with previous literature. Credit dynamics is found to be the best predictor of financial crises in previous literature (Borio and Lowe, 2002; Borio and Drehmann, 2009; Aldasoro, Borio and Drehmann, 2018), with newer studies including Schularick and Taylor ( 2012), alongside Drehmann and Juselius ( 2014), where the debt service to income ratio is one of the best early warning indicators, as found in this study. The private sector debt burden category is relevant, as found by Detken et al. ( 2014), or Giese et al. ( 2014). Moreover, the mispricing and external imbalances categories were found to have poor performance, as found in Slingenberg and de Haan ( 2011). The reasoning could be found in the poor performance of the stock market index, which has had little dynamics in the last 10-12 years. The lack of dynamics in a variable could result in no variation being caught in the modelling process. The results here are also in line with the research of Miszina and Tkacz ( 2009), who find that indicators such as asset prices are better predictors of future financial stress when nonlinearities are included in the analysis.

However, previous analysis observes the entire distribution performance of each category. In the next step, we observe those individual indicators that are useful in transition probability forecasting (equation (3)). We extract those indicators that have significant parameters in equation (3) and that are positive, indicating that greater values of those indicators affect the future probability of staying within the stressful regime or entering it. Put differently, when estimating the regime-switching model, the matrix in (2) includes the estimation of the parameter that is related to entering the regime of higher stress if the DGP was in the lower stress regime in the previous period. Furthermore, the matrix includes the parameter related to staying in the regime of higher stress if the DGP was previously in the same regime in the previous period. These parameters are depicted in table 3. The left panel in table 3 shows the value of the estimated parameters from equation (3) for the case of entering the higher risk from the lower risk regime for all four types of lags: t-4 to t-7. The right panel in table 3 contains values of the parameters regarding the case of staying in the higher risk regime. As the indicator variables are in different units of measurement, they are not directly comparable. The values are shown so that the dynamics of the parameter value can be observed. The dynamics are stable across all individual variables in the left panel in table 3. In contrast, an increasing trend is found in the right panel of table 3 for some variables (e.g., credit and house price series). Stable dynamics indicate a stable effect of a variable in the model, which is needed for its credibility. Increasing dynamics of the parameter in the right panel in table 3 means that the effects of individual indicators on the probability of staying in higher stress regime increases as the lag gets smaller. Such a result is in line with previous early warning system research 11 that concludes that the best-performing signalling indicators increase their values the most several quarters before the crisis hits. In the context of regime-switching, this could be interpreted as the persistence in those indicators accumulating the total effects for the future transition probability.

These results are in line with Duprey and Klaus ( 2017; 2022), who find that the credit and housing dynamics are the best predictors for entering a more stressful period; with Pietrzak ( 2021) who discovers that variables related to real estate markets (alongside earnings and profitability) are helpful in financial stress forecasting; specifically real estate prices as in Vašiček et al. ( 2017), as well as with some earlier studies such as Adalid and Detken ( 2007); and more recent, such as Christensen and Li ( 2014), and Slingenberg and Haan ( 2011), who also find that house price returns and credit growth are best predictors of financial stress. The house price-to-income ratio significance in this study is in line with Anundsen et al. ( 2016), who also found that the higher the value of this ratio, the more the probability of financial crisis increases. Although the results of this study are aligned with this mentioned research, it should be noted that the comparisons are made on a broader scale, i.e., this research looks at the effects of individual indicators on risk probabilities. In contrast, most of the work mentioned looks at the values of financial stress. As it is difficult to predict future values of financial stress, as the mentioned literature agrees, this research has the advantage of predicting just higher or lower stress regime probability, not actual values of financial stress.

In economic language, the results in table 3 are useful to determine which variables should be closely monitored over the financial cycle, as their dynamics affects the probability of entering or staying in the higher stress regime. The policymaker can observe these variables and their variations more closely, compared to the rest of those available, as monitoring many data at once is resource and time-consuming. Moreover, the results in table 3 show that the policymakers face difficulties when actively tracking the dynamics of most of the risk indicators. This is due to different units of measurement for each of the series, as this indicates non-synchrony of their characteristics regarding the assumption of the length of the financial cycle. This has proven in the literature to be a very difficult task, in Croatia as well (CNB, 2022b). Moreover, the policymaker needs to choose other relevant criteria to find the best indicator from figures 5 and 6. This will depend on the decision maker’s preferences and tracking of other indicator dynamics. One possible solution could be observing interval estimates of such indicators where different smoothing parameters are used. An example of such an application is found in CNB ( 2022b), in which flexibility is introduced by observing such intervals. When more data become available 12, the policymaker could re-estimate all of the models to see which indicators are best for specific purposes, including the one in this study.

Table 3Significant coefficients, probability of transitioning from lower to higher risk regime (upper panel) and significant coefficients, probability of staying in the higher risk regime (lower panel) DISPLAY Table

4.3 Discussion

Anundsen et al. (2016) state that specific information is present in each single country’s history of financial crises. Thus, it should be said that in the period before GFC, Croatia experienced an increase in internal and external vulnerabilities due to excessive credit activity and foreign borrowing. This is captured in the results, in the statistical significance of this risk category. Moreover, FDI (foreign direct investment) inflows at the beginning of the 2000s due to the privatization of telecoms and oil companies, and government foreign borrowing increased rapidly. Then, the GFC hit, and re-financing problems spilled over from mortgage markets to interbank money markets worldwide, including Croatia. This was when the HIFS indicator spiked in the analysed period (figure 1). Some of the macroprudential measures taken in the pre-GFC period had the goals of reducing credit growth and capital inflows, supporting the banking system’s liquidity and increasing its capitalization. By looking at all of the measures being put into place before the GFC (see Kraft and Galac, 2011 for details), it is seen that a lot of fine-tuning was done in the years that preceded the crisis. Kraft and Galac (2011) and Galac (2010) agree that some measures did manage to slow down the credit growth in that period, alongside the marginal reserve requirement. All this information indicates that the CNB utilized effective measures. However, many problems of that era, many of which were out of Croatia’s scope, contributed to the consequent crisis. If the knowledge from the estimated results here had been known back then, maybe the macroprudential policy would have been even tighter. This conclusion stems from the facts of what the policymakers were doing back then, just by observing the happenings in the financial system. As they were very active and prudent, having the output from models such as the one in this study would perhaps lead to more significant tightening. However, the measures taken back then for surely have contributed to lowering the probability of entering the more stressful regime.

The period from 2010 to 2015 was characterized by several stressful events for the Croatian markets: the government debt crisis in the Eurozone, the rise of CDS premiums on parent bank bonds of the largest banks in Croatia, the fall of the credit rating of Croatia in 2013 and increased costs of foreign borrowing. In this period, the macroprudential policy was loosening for the most part, as CNB was lowering the minimum required amount of foreign currency claims and was lowering reserve requirement rates so that the released funds would be utilized for economic recovery. Bambulović and Valdec ( 2020) found that domestic and foreign banks increased lending activity after the loosening measures. However, as Dumičić ( 2015a) pointed out, the recovery was prolonged due to a lack of structural reforms and a deterioration of fiscal indicators. This period indicates that although CNB had good timing of measures, the good conduct of macroprudential policy is not enough to bring the economy on the right path if other conditions are not fulfilled. The last sub-period, from 2016 until the end of the sample, was the most tranquil period until the COVID-19 shock hit. Here, the economic activity was in recovery, and lending to the private sector started to increase. In addition, CNB introduced tightening measures due to the new Basel accords and legislation. Finally, the COVID-19 shock was exogenous and could not have been forecasted with the cyclical risk indicators. This shows that there is a need for the policymaker to track structural and cyclical risks and mitigate them in a timely fashion so that the shocks in the financial stress series come from mostly exogenous shocks.

Consequences for policymakers are as follows. The results show that some indicators of cyclical risk accumulation provide information about future financial stress dynamics. The policymaker could use this information to narrow the most important indicators that need to be tracked over time and, consequently, tailor policies that would mitigate those risks. Although CNB had timely measures that focused on the majority of the risk indicators over the entire observed period, better coordination among macroprudential, monetary and fiscal policies is needed to achieve healthier economic growth. As some asymmetry in results is found, this indicates that the tightening and loosening policy should not be considered similarly.

The results indicate that policymakers will have to be flexible in policy tailoring, due to the difficulties of predicting financial stress. However, the results here do tell a similar story, in line with previous empirical research: credit and housing variables are extremely important in future financial risk materialization prediction and thus, useful for countercyclical capital buffer (CCyB) calibration (Bonfim and Monteiro, 2013) 13.The best indicators in this research are in line with the credit dynamics, such as the credit-to-GDP gap and growth rates of credit (Borio, 2012; Borio and Drehmann, 2009; Babecký et al., 2014); and property price dynamics, such as the growth rates and gaps regarding house prices, rents, construction work index (Borio, 2012; Jordá, Schularick and Taylor, 2015; Behn et al., 2013). Furthermore, external debt imbalances have been examined in the literature for a long time due to the analysis of currency crises. Variables regarding this group of potential indicators include different transformations of a country’s gross and net external debt, terms of trade, current account, and net export (Giese et al., 2014; Laeven and Valencia, 2008; Tölö, Laakkonen and Kalatie, 2018). In addition, the balance sheets of credit institutions were often analysed as well, as they give insights into potential weaknesses of the structure of the balance sheets. Here, the leverage ratio and other relevant ratios regarding deposits, assets, and credits of banks were analyzed (see Laina, Nyholm and Sarlin, 2015; Alessandri et al., 2015; Drehmann and Juselius, 2014; Rychtarik, 2014). Furthermore, the private sector debt burden has been recognized as another important group of measures, which includes debt service ratios (see Lombardi, Mohatny and Shim, 2017; Detken et al., 2014; Drehmann and Juselius, 2012; 2014). Finally, another group of variables that is important in evaluating their potential in signalling future crises is the mispricing of risks. It includes measures that relate to the credit institutions’ skewed views (interest rate margins), but private investors as well (in terms of stock market index-derived measures). Here, research finds that optimism and pessimism changes of economic agents over the financial cycle also affect the build-up of cyclical imbalances (see Pfeifer and Hodula, 2018; Drehmann et al., 2010).

5 Conclusion

Forecasting future financial stress is extremely relevant and topical. However, macroprudential policy is still relatively new compared to other economic policies, with respect to data availability and to the possibility of investigating transmission mechanisms of instruments and general interactions with different policies. Thus, any step forward in these areas contributes to a better understanding of the matter, so policymakers can tailor better instruments to achieve important objectives. This paper contributes to the literature by finding indicators that help forecast financial stress, in terms of switching from one regime to another, alongside utilizing techniques to reduce their number.

Instead of defining important dates of crises or specific events happening in the financial system, we allow the model to optimize the selection of which data should belong to each of the regimes. This lets the policymaker allow the data-generating process “to speak” freely without imposing assumptions or restrictions on the modelling process. Next, we focus on the properties of estimated regime-switching models across chosen lag lengths of indicator variables, and across risk group categories. This gives concise information about the quality of selected variables overall in terms of their forecasting capabilities. Nevertheless, the financial stress variable is very hard to predict, as it can react to different political, economic, and other shocks in the economy. That is why the approach made here was not to forecast the value of the stress variable itself but to try to incorporate additional information into the probability of (re)entering the higher stress regime. The results are in line with related literature, as the credit and housing price variables stood out the most here, as they did in previous research on related topics. But here, this confirmation is obtained from another approach to the problem. Although more than 900 models have been estimated and compared, with more than 240 variables considered in the analysis, one could say that the results are not so promising due to not more than 20 variables having been found to have meaningful results. This does not have to reflect poor data availability or other similar reasoning. On the contrary, it could reiterate the problems of macroprudential policymaking and research as a still insufficiently analysed area of research and application.

However, we are aware of the shortfalls of such approaches due to lack of data, shorter periods, bias of results, etc. The Croatian time series is short compared to other countries which only enabled in-sample analysis. Single-country analysis suffers from having only a few crisis periods in the sample, which is not something new (see Claessens, 2009). However, a starting point is needed, and macroprudential instruments need to be calibrated on the specific characteristics of a country. Moreover, a single-country analysis can be enhanced by combining both approaches (EWS indicators and the regime-switching of stress) has the potential to obtain overall good forecasting results. As Kauko ( 2014) observes, most of research on EWS utilizes binary variables as the dependent ones in the analysis. As crises rarely occur, meaning that not many observations are included in the regime of crisis occurrence, the combination of financial stress data as the dependent variable can be helpful. Vermeulen et al. ( 2015) agree on this topic. Finally, the EWS approach utilized often in research depends on the policymaker’s preferences regarding false alarms and missing signals. On the other hand, regime-switching does not include such subjectivity. The heterogeneity in different countries may not capture specific variables or their transformations as relevant in the modelling process.

Macroprudential policymakers could use results from this study to track specific indicators in greater detail and try to estimate the stance concerning the instruments used over the observed period and the goals set during the boom-and-bust phases of the financial cycle. The Croatian case showed that the policymakers had a good focus on specific problems that were occurring during the entire observed sample. Most tightening and loosening measures were tailored according to some of the indicators found to be the best-performing ones in this study.

Future work should seek how to do a similar analysis such as this one on a larger scale, considering that all different variable categories, variable transformations, and lag selection make this a big data problem. This could be relevant for international institutions or those who need to monitor more countries simultaneously. Other institutions focusing on one country could apply this approach regularly, since the problem is focused on the country the researcher or policymaker is familiar with the most.

Appendix

Table A1SIC information criterion on different specifications of ARMA(p,q) model for variable HIFS DISPLAY Table Figure A2Log likelihood statistics for regime switching models with variable indicators included in the equation (3) DISPLAY Figure #figure10456# #figure10457#

Notes

* The views expressed are those of the author and do not necessarily reflect the official views of the institution the author works at. The author is grateful to two anonymous referees who have contributed to the quality of the final version of the paper. The paper was written when the author was at Croatian National Bank, Department for Financial Stability.

1 This is due to the intuitive interpretation of dynamics and characteristics of economic and financial variables via expansions and contractions in real economy or bull and bear markets in financial markets (see Ang and Timmermann, 2012). Structural and abrupt changes in the economy and/or financial markets due to political issues, legislative changes, new methodological approaches, etc. can be captured via the regime-switching approach (Baele, 2003 is an example of the economic and monetary integration of Western Europe affecting the European financial markets).

2 Croatia has a specific, i.e., unique experience regarding macroprudential policymaking and monitoring cyclical risk accumulation. It stands out due to it belonging to a group of countries that had the most intensive use of instruments before the global financial crisis (Vujčić and Dumičić, 2016). This means that macroprudential policy was active during the boom and bust phases of the financial cycle. Analysis regarding Croatian data could provide insights into the effects of macroprudential policy during all phases of the cycle, the effects on the financial stress, and other analyses of interactions of this policy with the rest of the economy. As Vujčić and Dumičić (2016) state, Croatian experience shows that policymakers shouldn’t focus only on textbook approaches to macroprudential policy conduct but, to keep their minds open, also on analysis such as the one in this study. However, a not-typical one could be one of the starting points. Moreover, Bambulović and Valdec (2020) state that Croatia is an interesting country for a study of the effects of macroprudential policies on credit growth, as the Croatian National Bank employed many measures in the pre-GFC period. More specifically, greater macroprudential activity started in 2003, as it was seen that monetary policy would not be efficient alone (see Kraft and Galac, 2011).

3 That is why forecasting future financial stress would be helpful in order to adjust the instruments and measures so that the financial system is more robust and stable over time, alongside reducing the costs of financial crises. Moreover, financial stress indicators are used in the quick release of the countercyclical capital buffers (CCyB), as at the beginning of the COVID-19 crisis in some countries (see Arbatli-Saxegaard and Muneer, 2020).

4 A stress event is defined if the stress indicator exceeds its mean value enlarged by its standard deviation multiplied by a constant k. This could be arbitrary, as opposed to the regime-switching that is based on the optimization of the likelihood function in which optimal switching behaviour is governed by the data. This is what the authors concluded at the end of the study: future research should focus on switching models.

5 A drawback of the study is found in determining the stress periods when the financial condition indicator exceeds the 90th percentile of the country's indicator distribution. The regime-switching approach does not ask for such interventions from the researcher's side.

6 Calculation of HIFS is based on volatilities and similar measures and correlations derived from daily data on bond yields, stock market returns, money market interest rates, exchange rates, and interbank market rates and fragility. It does not include any of the individual indicators (or their transformations) used in MRS modelling.

7 Margins were calculated as the difference between the interest rates on credits to HH or NFC and the Euribor interest rate, as the national referent interest rate ceased to exist in 2020. Comparable studies (e.g. Kupkovič and Šuster, 2020) also use Euribor as the referent interest rate.

8 Defined in Pfeifer and Hodula (2018).

9 The results in figure 1 are comparable to those in Dumičić (2015a) in sub-periods of greater and lower stress. Furthermore, based on the discussion in section 4.3., in a comparison of the results to the discussion in the mentioned paper, findings on indicators in table 3 of this research confirm the importance of these indicators for macroprudential policy-making, alongside the measures that the CNB conducted in the observed sample. For more details, please see section 4.3.

10 As the baseline model has LogL value of 131.873 (see table 2), inclusion of indicator variables in the model is considered successful if the new model has a higher value than the baseline model to ensure comparability across all specifications, all models are contrasted on the same length of T.

11 See literature review section, and introduction.

12 And more data on the characteristics of individual indicators during different phases of the financial cycle, so that the duration of the cycle could be estimated better.

13 That is why additional analysis was done by constructing a composite indicator of cyclical risks based on the results from this study and it has a potential for being used in practice. Details are available upon results.

* The views expressed are those of the author and do not necessarily reflect the official views of the institution the author works at. The author is grateful to two anonymous referees who have contributed to the quality of the final version of the paper. The paper was written when the author was at Croatian National Bank, Department for Financial Stability.

1 This is due to the intuitive interpretation of dynamics and characteristics of economic and financial variables via expansions and contractions in real economy or bull and bear markets in financial markets (see Ang and Timmermann, 2012). Structural and abrupt changes in the economy and/or financial markets due to political issues, legislative changes, new methodological approaches, etc. can be captured via the regime-switching approach (Baele, 2003 is an example of the economic and monetary integration of Western Europe affecting the European financial markets).

2 Croatia has a specific, i.e., unique experience regarding macroprudential policymaking and monitoring cyclical risk accumulation. It stands out due to it belonging to a group of countries that had the most intensive use of instruments before the global financial crisis (Vujčić and Dumičić, 2016). This means that macroprudential policy was active during the boom and bust phases of the financial cycle. Analysis regarding Croatian data could provide insights into the effects of macroprudential policy during all phases of the cycle, the effects on the financial stress, and other analyses of interactions of this policy with the rest of the economy. As Vujčić and Dumičić ( 2016) state, Croatian experience shows that policymakers shouldn’t focus only on textbook approaches to macroprudential policy conduct but, to keep their minds open, also on analysis such as the one in this study. However, a not-typical one could be one of the starting points. Moreover, Bambulović and Valdec ( 2020) state that Croatia is an interesting country for a study of the effects of macroprudential policies on credit growth, as the Croatian National Bank employed many measures in the pre-GFC period. More specifically, greater macroprudential activity started in 2003, as it was seen that monetary policy would not be efficient alone (see Kraft and Galac, 2011).

3 That is why forecasting future financial stress would be helpful in order to adjust the instruments and measures so that the financial system is more robust and stable over time, alongside reducing the costs of financial crises. Moreover, financial stress indicators are used in the quick release of the countercyclical capital buffers (CCyB), as at the beginning of the COVID-19 crisis in some countries (see Arbatli-Saxegaard and Muneer, 2020).

4 A stress event is defined if the stress indicator exceeds its mean value enlarged by its standard deviation multiplied by a constant k. This could be arbitrary, as opposed to the regime-switching that is based on the optimization of the likelihood function in which optimal switching behaviour is governed by the data. This is what the authors concluded at the end of the study: future research should focus on switching models.

5 A drawback of the study is found in determining the stress periods when the financial condition indicator exceeds the 90 th percentile of the country's indicator distribution. The regime-switching approach does not ask for such interventions from the researcher's side.

6 Calculation of HIFS is based on volatilities and similar measures and correlations derived from daily data on bond yields, stock market returns, money market interest rates, exchange rates, and interbank market rates and fragility. It does not include any of the individual indicators (or their transformations) used in MRS modelling.

7 Margins were calculated as the difference between the interest rates on credits to HH or NFC and the Euribor interest rate, as the national referent interest rate ceased to exist in 2020. Comparable studies (e.g. Kupkovič and Šuster, 2020) also use Euribor as the referent interest rate.

8 Defined in Pfeifer and Hodula ( 2018).

9 The results in figure 1 are comparable to those in Dumičić ( 2015a) in sub-periods of greater and lower stress. Furthermore, based on the discussion in section 4.3., in a comparison of the results to the discussion in the mentioned paper, findings on indicators in table 3 of this research confirm the importance of these indicators for macroprudential policy-making, alongside the measures that the CNB conducted in the observed sample. For more details, please see section 4.3.

10 As the baseline model has LogL value of 131.873 (see table 2), inclusion of indicator variables in the model is considered successful if the new model has a higher value than the baseline model to ensure comparability across all specifications, all models are contrasted on the same length of T.

11 See literature review section, and introduction.

12 And more data on the characteristics of individual indicators during different phases of the financial cycle, so that the duration of the cycle could be estimated better.

13 That is why additional analysis was done by constructing a composite indicator of cyclical risks based on the results from this study and it has a potential for being used in practice. Details are available upon results.

Disclosure statement

The author declares that there is no conflict of interest.

References

Adalid, R. and Detken, C., 2007. Liquidity shocks and asset price boom/bust cycles. ECB Working Paper, No. 732 [ CrossRef]

Adrian, T., Boyarchenko, N. and Giannone, D., 2019. Vulnerable growth. American Economic Review, 109(4), pp. 1263-1289 [ CrossRef]

Alessandri, P. [et al.], 2015. A note on the implementation of a Countercyclical Capital Buffer in Italy. Bank of Italy Occasional Paper, No. 278 [ CrossRef]

Alessi, L. and Detken, C., 2019. Identifying excessive credit growth and leverage. Journal of Financial Stability, 35, pp. 215-225 [ CrossRef]

Ang, A. and Bekaert, G., 2002a. Short Rate Nonlinearities and Regime Switches. Journal of Economic Dynamics and Control, 26, pp. 1243-1274 [ CrossRef]

Ang, A. and Bekaert, G., 2002b. International Asset allocation With Regime Shifts. Review of Financial Studies, 15, pp. 1137-1187 [ CrossRef]

Ang, A. and Timmermann, A., 2012. Regime changes and financial markets. Annual Review of Financial Economics, 4, pp. 313-337 [ CrossRef]

Anundsen, A. K. [et al.], 2016. Bubbles and crises: The role of house prices and credit. Journal of Applied Econometrics, 31, pp. 1291-1311 [ CrossRef]

Arbatli-Saxegaard, E. C. and Muneer, M. A., 2020. The countercyclical capital buffer: A cross-country overview of policy frameworks. Staff memo, No. 6.

Babecký, J. [et al.], 2014. Banking, Debt, and Currency Crises in Developed Countries: Stylized Facts and Early Warning Indicators. Journal of Financial Stability, 15, pp. 1-17 [ CrossRef]

Bambulović, M. and Valdec, M., 2020. Testing the characteristics of macroprudential policies’ differential impact on foreign and domestic banks’ lending in Croatia. Public Sector Economics, 44(2), 221-249 [ CrossRef]

Behn, M. [et al.], 2013. Setting Countercyclical Capital Buffers Based on Early Warning Models: Would It Work? ECB Working Paper, No. 1604.

Bloom, N., 2009. The Impact of Uncertainty Shocks. Econometrica, 77(3), pp. 623-685 [ CrossRef]

Borio, C. and Lowe, P., 2002. Asset prices, financial and monetary stability: exploring the nexus. BIS Working Papers, No 114 [ CrossRef]

Candelon, B., Dumitrescu, E-I. and Hurlin, C., 2012. How to Evaluate an Early-Warning System: Toward a Unified Statistical Framework for Assessing Financial Crises Forecasting Methods. IMF Economic Review, 60, pp. 75-113 [ CrossRef]

Cardarelli, R., Elekdag, S. and Lall, S., 2011. Financial stress and economic contractions. Journal of Financial Stability, 7(2), pp. 78-97 [ CrossRef]

Chavleishvili, S. and Manganelli, S., 2019. Forecasting and stress testing with quantile vector autoregression. ECB Working Paper, No. 2330 [ CrossRef]

Christensen, I. and Li, F., 2014. Predicting financial stress events: a signal extraction approach. Journal of Financial Stability, 14, pp. 54-65 [ CrossRef]

Davis, E. P. and Karim, D., 2008. Comparing early warning systems for banking crises. Journal of Financial Stability, 4(2), pp. 89-120 [ CrossRef]

Detken, C. [et al.], 2014. Operationalising the countercyclical capital buffer: indicator selection, threshold identification and calibration options. ESRB Occasional Paper, No. 2014/5 [ CrossRef]

Dimova, D., Kongsamut, P. and Vandenbussche, J., 2016. Macroprudential Policies in Southeastern Europe. Working Paper, No. 16/29 [ CrossRef]

Doz, C., L. Ferrara and P. Pionnier, 2020. Business cycle dynamics after the Great Recession: An extended Markov-Switching Dynamic Factor Model. OECD Statistics Working Papers, No. 2020/01 [ CrossRef]

Drehmann, M. [et al.], 2010. Countercyclical capital buffers: exploring options. BIS Working Papers, No. 317 [ CrossRef]

Drehmann, M. and Juselius, M., 2014. Evaluating early warning indicators of banking crises: Satisfying policy requirements. International Journal of Forecasting, 30(3), pp. 759-780 [ CrossRef]

Dumičić, M., 2015a. Financial stress indicators for small, open, highly euroized countries: the case of Croatia. Financial Theory and Practice, 39(2), pp. 171-203 [ CrossRef]

Dumičić, M., 2015b. Financial Stability Indicators – The Case of Croatia. Journal of Central Banking Theory and Practice, (1), pp. 113-140 [ CrossRef]

Duprey, T. and Klaus, B., 2017. How to predict financial stress? An assessment of Markov switching models. ECB Working Paper, No. 205 [ CrossRef]

Duprey, T. and Klaus, B., 2022. Early warning or too late? A (pseudo-) real-time identification of leading indicators of financial stress. Journal of Banking and Finance, 138, 106196 [ CrossRef]

Duraković, E., 2021. Croatian Systemic Stress Index. CNB Working Paper, No. I-61.

ESRB 2018. The ESRB handbook on operationalising macroprudential policy in the banking sector. European Systemic Risk Board.

Franses, P. H. and van Dijk, D., 2000. Nonlinear time series models in empirical finance. Cambridge: Cambridge University Press [ CrossRef]

Galán, J. E., 2019. Measuring Credit-to-GDP Gaps. The Hodrick-Prescott Filter Revisited. Documentos de Trabajo, No. 1906 [ CrossRef]

Galati, G. [et al.], 2016. Measuring financial cycles in a model-based analysis: Empirical evidence for the United States and the Euro Area. Economics Letters, 145, pp. 83-87 [ CrossRef]

Giese, J. [et al.], 2014. The credit-to GDP gap and complementary indicator for macroprudential policy: evidence from the UK. International journal of finance and economics, 19(1), pp. 25-47 [ CrossRef]

Giglio, S., Bryan, K. and Pruitt, S., 2016. Systemic Risk and the Macroeconomy: An Empirical Evaluation. Journal of Financial Economics, 119(3), pp. 457-471 [ CrossRef]

Gneitinga, T. and Ranjanb, R., 2011. Comparing Density Forecasts Using Threshold- and Quantile-Weighted Scoring Rules. Journal of Business and Economic Statistics, 29(3), pp. 411-422 [ CrossRef]

Gray, S. F., 1996. Modeling the Conditional Distribution of Interest Rates as a Regime-Switching Process. Journal of Financial Economics, 42, pp. 27-62 [ CrossRef]

Hodrick, R. and Prescott, E., 1997. Postwar U.S. Business Cycles. An Empirical Investigation. Journal of Money, Credit, and Banking, 29, pp. 1-16 [ CrossRef]

Hubrich, K. and Tetlow, R., 2015. Financial stress and economic dynamics: The transmission of crises. Journal of Monetary Economics, 70(C), pp. 100-115 [ CrossRef]

Jordá, O., Schularick, O. and Taylor, A. M., 2015. Leveraged Bubbles. Journal of Monetary Economics, 76(Supplement), pp. S1-S20 [ CrossRef]

Kaminsky, G. L. and Reinhart, C. M., 1999. The Twin Crises: The Causes of Banking and Balance-of-Payments Problems. American Economic Review, 89(3), pp. 473-500 [ CrossRef]

Kauko, K., 2014. How to foresee banking crises? A survey of the empirical literature. Economic Systems, 38(3), pp. pp. 289-308 [ CrossRef]

Kim, C-J., 1994. Dynamic Linear Models with Markow-Switching. Journal of Econometrics, 60, pp. 1-22 [ CrossRef]

Klomp, J., 2010. Causes of banking crises revisited. The North American Journal of Economics and Finance, 21(12), pp. 72-87 [ CrossRef]

Kraft, E. and Galac, T., 2011. Macroprudential Regulation of Credit Booms and Busts, The Case of Croatia. Policy Research Working Paper, No. 5772 [ CrossRef]

Laeven, L. and Valencia, F., 2008. Systemic Banking Crises: A New Database. IMF Working Paper, No. WP/08/224 [ CrossRef]

Laina, P., Nyholm, J. and Sarlin, P., 2015. Leading Indicators of Systemic Banking Crises: Finland in a Panel of EU Countries. Review of Financial Economics, 24, pp. 18-35 [ CrossRef]