|

|

|

Abstract

Inflation that is fully anticipated has few real effects in purely private market economies, but this need not be the case in the presence of taxation. In practice, tax systems are not neutral with respect to inflation – though some countries have attempted make their tax systems inflation-neutral in the past – and this paper provides a comprehensive overview of the most relevant non-neutralities, drawing on existing literature, but also supplying new illustrations and evidence of the effects. The paper shows, for example, how taxing inflationary gains can have a large impact on effective tax rates – even at relatively low rates of inflation. It also shows how partial coverage of protection against inflation – for some types of incomes only – can create additional distortions. A new empirical analysis reveals how the erosion of the value of depreciation allowances through inflation affects investment. Finally, the paper discusses policy options to address such non-neutralities.

Keywords: tax policy; inflation; bracket creep; indexation; fiscal policy; income taxation

JEL: H20, E31

1 Introduction

Inflation rates around the world have risen. Inflation in advanced economies has reached its highest rate in forty years, increasing from 3.1 percent in 2021 to an estimated 7.2 percent in 2022. In emerging market and developing economies, inflation in 2022 is expected to have reached 9.9 percent (IMF,  2022). While there has been considerable discussion of the relative roles of monetary and fiscal policy (quantitative easing, fiscal stimulus to fight the pandemic and afterwards) versus supply shocks (Russia’s invasion of Ukraine, and food and energy price increases) in causing inflation, less attention has been given to the impact of higher inflation on fiscal aggregates and the stance of fiscal policy, but also how does inflation interact with the tax system, what distortions does this give rise to, and how might they be corrected? The present paper considers this latter set of questions. It draws heavily on literature from the 1970s and 1980s,1 when this topic was last studied in detail, probably because inflation started coming down soon after, at least in advanced economies, and the topic was then thought to be less relevant. However, this paper shows that the impact of inflation on tax revenues, marginal tax rates, and effective tax rates is not negligible, even at lower inflation rates. 2022). While there has been considerable discussion of the relative roles of monetary and fiscal policy (quantitative easing, fiscal stimulus to fight the pandemic and afterwards) versus supply shocks (Russia’s invasion of Ukraine, and food and energy price increases) in causing inflation, less attention has been given to the impact of higher inflation on fiscal aggregates and the stance of fiscal policy, but also how does inflation interact with the tax system, what distortions does this give rise to, and how might they be corrected? The present paper considers this latter set of questions. It draws heavily on literature from the 1970s and 1980s,1 when this topic was last studied in detail, probably because inflation started coming down soon after, at least in advanced economies, and the topic was then thought to be less relevant. However, this paper shows that the impact of inflation on tax revenues, marginal tax rates, and effective tax rates is not negligible, even at lower inflation rates.

In simple models of a private market economy with full market clearing, changes in nominal variables such as the money supply and the general price level – at least when anticipated – should not have significant real effects. While increases in the money supply may have short-run real effects due to wage or price rigidities, in the long-run wages and prices adjust, and agents base their decisions on real or relative prices and – abstracting away from hysteresis effects – the real equilibrium is unchanged (Friedman, 1968). With fully flexible prices the arguments for neutrality are stronger. Even in this case, surprise money supply and price level increases have the potential to have real effects, if they cause misperceptions that relative prices have increased thus leading to increased supply (Lucas, 1972). With fully flexible prices, expected changes in inflation should have few real economic implications, save for reduced real holdings of cash (and other unremunerated liquidity) and some additional printing costs (unless money is fully digitalized). However, save for the case of hyperinflation, the magnitudes are likely to be small.

In a mixed economy, however, where a significant share of income is collected through taxes and used for public spending, even inflation that is fully anticipated can have real effects, if the tax system is not neutral with respect to inflation. 2 By neutrality with respect to inflation, we mean that the impact of the tax system on incentives and tax burdens does not change with inflation. It does not necessarily mean that the tax system is more generally neutral in its impact on incentives (such as for investment or labour supply).

This paper describes and analyses various non-neutralities of the tax system with respect to inflation, both drawing on the existing literature and showing new illustrations and evidence of the effects. The paper shows how the taxation of income gains that are purely inflationary can have a tremendous impact on effective tax rates – even at relatively low rates of inflation. The paper also shows how partial adjustment for inflation – for only some types of incomes – can create additional distortions. A new empirical analysis reveals how the erosion of the value of depreciation allowances through inflation reduces investment. The paper also discusses a range of policy options to address these non-neutralities due to inflation, from specific measures that aim to address individual distortions to more comprehensive reforms of the tax system (which might also improve the efficiency of the tax system more generally).

There are further important links between inflation and tax that are not covered here, as they are not related to structural tax issues but instead to the macroeconomic linkages. These include seigniorage, sometimes known as the inflation tax, although “tax” is used metaphorically in that case. Also, tax policy, like any fiscal policy, affects aggregate demand and hence has a macroeconomic impact on inflation. Another issue is that taxes, especially those on consumption, such as a value-added tax (VAT) or sales tax, have an immediate (but one-off) impact on inflation.

In covering the main distortions of the tax system due to inflation, this paper is organized by the underlying cause of the distortion rather than by the type of tax or its economic importance. The focus is on the common causes of distortions, and how these apply to different types of tax. Section 2 covers distortions that arise due to the failure to adjust certain parameters of the tax system in line with inflation (examples include thresholds for paying tax that are fixed in nominal terms, or specific taxes that also are set in nominal terms). Section 3 examines the tax consequences resulting from timing effects, such as the lag with which taxes are collected and refunded, and how these interact with inflation. The paper then covers the more general problem caused by taxing nominal rather than real income, in particular capital gains and capital income. Given the length of this discussion, it is split into two parts: section 4 focuses on the household level while section 5 examines taxation at the corporate level. Section 6 provides a summary and concludes.

2 Non-adjustment of the parameters of the tax system

The simplest way in which inflation can lead to unintended changes in taxes is when the parameters of the tax system are fixed in nominal terms without adjustment for inflation. The simplest example is taxes or fines that are fixed in domestic currency (specific taxes) rather than as a percentage (ad valorem). These include specific excises, lumpsum taxes, license fees, and certain simplified taxes (e.g., taxes per table in a restaurant). They also include nontax items such as fees, fines, or interest assessed for the late filing or payment of taxes. Finally, even ad valorem taxes can be affected if the thresholds for registration or for higher rate brackets are fixed in nominal terms.

2.1 Specific taxes, fees, and penalties

There are good reasons for some taxes to be specific rather than ad valorem. Excises levied to address an externality, such as a carbon tax or taxes on alcohol and tobacco, aim to internalize the real cost of consumption to society, and this real cost will depend on the amount consumed rather than the nominal value of the item consumed.3 Fuel prices, for example, are very volatile, but the harmful effect of burning fuel does not increase with the price of fuel. Prices for wine vary tremendously with quality, but more expensive wine does no more harm than cheap wine.

However, inflation means that the real value of specific taxes, fees, and penalties is eroded over time. Where an excise was set at a value meant to internalize an externality, after inflation-induced erosion of the real value of the tax, it does not cover the externality in real terms anymore, and also leads to lower real revenues. Some countries define specific taxes, notably tariffs, in US dollars, 4 which might offer some protection against local inflation eroding the real value of the excise, provided the exchange rate adjusts over time to offset inflation. In practice this may not be the case, as exchange rate movements can differ quite substantially from purchasing power parity conditions (so will not offset one for one). Moreover, even when the exchange rate does adjust in a way that offsets inflation reasonably closely, over time, excises fixed in dollar terms would still have their real value eroded because of US inflation – which, although lower than in many developing countries, is clearly nonzero, with the official target at 2 percent, and current rates much higher. Adjustment is therefore still needed, though not as frequently as when specified in a currency that is marked by very high inflation and corresponding depreciation.

2.2 Fixed interest rates

Tax laws sometimes contain fixed interest rates for overdue payments, which tend to lower real revenues in inflationary times.5 Sometimes a lower rate applies for some accidental under- and overpayment, and a higher penalty rate in cases of late filing or underpayment due to tax fraud. In either case, if the percentage rate is fixed in the law, its real value will be eroded by inflation. As a result, in high inflation periods, the real penalty for late payment is lower. In extreme cases it could effectively turn into a premium for late payment, if the interest rate in the tax law is lower than what the taxpayer can obtain in the financial market. The opposite occurs in times of very low inflation, such as the recent period during which many central banks had interest rates at zero or even negative rates. This encourages overpayment of taxation if refunds benefit from application of a fixed interest rate, even if it is set at a very low level.

2.3 Thresholds

Taxes that are expressed as simple percentages adjust automatically with inflation. However, when rates are not flat, such as under a progressive income or inheritance tax, inflation can cause real tax increases when income tax brackets (thresholds) are fixed in nominal terms. Inflation shifts people into higher tax brackets, which typically have higher tax rates, and thus erodes the value of the tax-free personal allowance (and any other allowances or deductions). So real taxes paid increase, as does the marginal rate. This is known as bracket creep, and could be avoided by full inflation indexation of thresholds.

This issue does not arise for a truly proportional income tax system (with a flat rate starting from zero income) 6 or for consumption taxes such as VAT or sales tax. These taxes are naturally neutral with respect to inflation, except for any effect from registration thresholds being set in nominal terms (see below). Inflation will boost revenues from such proportionate taxes in nominal terms, but in real terms the tax remains the same. For goods with price increases that exceed the general inflation rate, the real value of tax revenues rises, but this increase then reflects the change in relative prices, not general inflation.

The reverse effect occurs with social security or national insurance contributions, as in some countries these are not levied beyond a certain income threshold. Higher inflation then leads to lower real payments, as the amount of income that exceeds the upper limit rises with inflation.

The extent of bracket creep depends on the structure of the tax system. Bracket creep does not exist for a completely flat tax and is more severe if there are many brackets or large differences in rates between brackets. Immervoll ( 2005) compared the impact of bracket creep for personal income tax in the Netherlands, Germany, and the United Kingdom. He found that the simulated effect of bracket creep is much lower in the United Kingdom because at that time it had few and wide tax brackets, meaning that fewer people were shifted into higher tax brackets as a result of inflation than in Germany (where there are infinite brackets, given the linearly rising marginal tax rate) or the Netherlands where there are various large jumps in brackets. 7

Table 1Adjustment of income tax thresholds DISPLAY Table

A few countries adjust personal income tax thresholds automatically for inflation, but the majority either do not adjust them regularly, or do so in an ad hoc manner that may or may not be aligned with inflation (table 1). Of 160 countries from which we could obtain data, there are 131 countries (too many to list) that do not adjust thresh-olds regularly (defined as almost every year). Other countries do adjust regularly, but only in nine could we find an explicit legal or administrative reference to a process that adjusts for inflation. In the case of ad hoc adjustments – for example changing thresholds during the budget process – policy considerations (such as a potential need for fiscal consolidation) tend to be weighed against keeping the real tax system unchanged through inflation adjustment of thresholds. Raising thresholds but by less than the inflation rate (or even freezing them but then cutting tax rates) can appear a politically expedient way to raise real taxes by stealth, while appearing to lower them.

With the interaction of higher inflation and fixed nominal thresholds typically leading to increases in real tax revenues and marginal tax rates, some have argued that higher inflation increases income tax evasion. Simple models suggest that tax evasion depends on the probability of detection, the fine or penalty rate if detected, the tax rate, and the level of true income (Arrow’s hypothesis that absolute risk aversion decreases as income increases). If inflation causes the tax rate to increase, then so does the incentive to evade taxes; however, the resulting fall in real income might offset this if it leads to greater risk aversion. Given such ambiguity, it is an empirical question which effect dominates. Crane and Nourzad ( 1986), using US data 1947-81, find that higher inflation leads to higher aggregate tax evasion. In addition, it seems likely that higher inflation reduces the fine or penalty rate (unless these are adjusted rapidly) which again would support the hypothesis that inflation increases tax evasion.

Similar issues can arise with registration thresholds. VAT typically has a registration threshold to limit coverage to businesses where expected revenues exceed the administrative cost. Inflation erodes the real value of this threshold. More businesses then have to register for VAT, creating administrative costs for the tax authorities and compliance costs for businesses. Unlike for personal income tax thresholds, there appears to be no country in the world that regularly adjusts VAT registration thresholds. In some countries, the original threshold might have been set too high, perhaps deliberately for the sake of being able to phase in the VAT. In those cases, inflation would raise additional revenues that exceed the additional administrative costs and would therefore benefit the public finances. However, even in those cases, it would be unlikely that the desired lowering of the real threshold would coincide exactly with the inflation rate.

2.4 Solutions to the erosion of specific taxes and thresholds

Resolving the erosion of fixed parameters of the tax system is easy to solve technically. Indexing the parameters to a reliable inflation measure should fix the problem. The frequency of optimal adjustment depends on the inflation rate. For modest inflation, annual adjustment is sufficient, while high inflation could require more frequent adjustment.

In the case of interest rates and penalty rates, the problem could be solved if these could be defined as a markup over the inter-bank or government bond rate. In principle it could also be a fixed rate that is increased by the prevailing inflation rate, but such precision might not be necessary. Moreover, from a taxpayer’s perspective any decisions on later payments are likely to be based on comparisons of the rate in the tax law to that available in the financial markets, hence a markup over the latter would prevent the creation of incentives for payment delays in inflationary periods.

In the case of specific taxes, fixing them in a more stable foreign currency may help, but this will not ensure that their real value is stabilized. This approach only protects partially against domestic inflation and could lead to unwanted changes in taxes driven by exchange rate changes. The specific taxes would also need to be increased in line with foreign country inflation – especially in times of high global inflation. For a few excises the solution could also be to switch from specific to ad valorem, though as noted, such a move would have consequences that go beyond addressing inflation and may therefore often not be advisable.

While indexation is technically simple, it may face political obstacles but would be more transparent. The annual adjustment of thresholds allows the government to appear to cut taxes, while automatic indexation would make it more obvious that the system is merely being kept stable. Automatic indexation would also improve transparency in policy making. Upward changes to thresholds tend to benefit most those with high incomes. Hence any such adjustment can be portrayed as being regressive – even though in the case of an inflation adjustment it merely maintains the same real progressivity. These interactions between inflation adjustment and changes to progressivity can be avoided, if thresholds adjust automatically with inflation and debates on any additional changes in the threshold can focus on the desired progressivity of the system.

Unlike wage and price indexation, indexing thresholds does not perpetuate inflation, but prevents inflation from leading to arbitrary changes in real taxes. Wage and price indexation makes disinflation harder by making an initial burst of inflation more entrenched, both by leading to second rounds of cost and price increases and also by de-anchoring inflation expectations. Indexing thresholds has no such effect, although if not indexed then inflation does lead to a real increase in tax revenues which would help in disinflation. Indexation leaves real tax revenues unchanged, and thus is neither inflationary nor disinflationary. It is true that indexing thresholds reduces the tax distortions associated with higher inflation, and by making inflation less costly could reduce the incentives for policymakers to lower inflation, but this would seem a contrived argument for not addressing the distortions that inflation gives rise to.

To the extent that tax evasion increases with inflation (as explained above), this would call for devoting greater resources and efforts to tax compliance in times of high inflation.

3 Timing issues

3.1 Lags in collections and refunds

Even when taxes increase one for one with inflation, collecting revenues takes time, and this can erode tax revenues in real terms when there is inflation (Olivera, 1967; Tanzi, 1977). As argued in the previous section, the presence of fixed nominal income tax thresholds means that inflation leads to higher real revenues. This is the conventional result for economies with progressive income tax systems and prompt tax collection. However, income taxes collected in any given period typically depend on personal or corporate income earned some time earlier. In the presence of inflation, this collection delay results in lower real tax revenues. The effect is likely to be particularly significant for countries where the tax system is not elastic (i.e., which lack progressive income tax systems), where collection delays are significant (income tax or property tax, as opposed to VAT, sales taxes, and excises), and where inflation is high (so the real erosion is greater) (Tanzi, 1977).

VAT is typically paid on a quarterly or even monthly basis, with companies remitting net VAT – the difference between VAT collected on outputs and VAT paid on inputs – to the tax authority. The tax credits companies receive for the VAT they paid on intermediate inputs thus tend to retain their real value during normal commercial undertakings, even in the presence of inflation. However, for large-scale projects with extended construction periods, such as encountered in the natural resource or tourism sector, the lag between payment of input VAT and receipt of a corresponding input tax credit can take several years. Besides the cash-flow problems that a delayed refund creates, inflation also erodes the real value of the tax credit and thus increases the effective tax rate on (instantaneous) value added.

Fixed penalties or penalty interest rates are not only directly eroded by inflation (as noted in the previous section) but their deterrent effects also lessen as inflation increases the real value of postponing tax payments. The real cost of a penalty can be maintained by indexing the payment to inflation. Its deterrent effect is nevertheless reduced in a high inflation environment, because the real saving from making a later payment rises. Payments delays themselves can lengthen endogenously, as the benefits of delay increase with inflation. To prevent this, one would need to index the tax payment itself for inflation, or subject it to a variable penalty interest rate

Investment is usually depreciated over time in most tax systems. As it is typically based on a percentage of historical costs, the value of depreciation deducted from profits in later years is eroded by inflation. The phenomenon will be discussed in greater detail in the section on taxing nominal profits. Similarly, loss-making firms can typically use losses against future profits (with restrictions that vary across countries), but the value of such losses carried forward is eroded over time in the presence of inflation.

3.2 Policies to address timing issues

While a fully comprehensive solution to timing effects would involve the introduction of a fully inflation-neutral tax system (as will be discussed later), the simplest way to solve the problem of timing issues is to speed up tax payments. Options to prevent the amount of tax levied from declining in real terms in the presence of inflation include:- Introducing withholding taxes so that income is taxed as it is earned, including through pay-as-you-earn schemes for wage taxes. If the precise tax liability cannot be determined, as would be the case in a comprehensive income tax system with progressive rates, a nonfinal withholding tax can still bring forward cash payments and improve incentives for the rapid filing of returns.

- Greater reliance on advance corporate income tax (CIT), which should be based on expected profits. If that tax base is estimated from historic profits, it should be adjusted for inflation.

- More frequent asset revaluations. Where the cost of updating is high, for example for property tax, some formulaic mechanism can be used in years in which properties are not due a full review, and this should reflect inflation.

- Once a tax has been determined, steps also need to be taken to discourage delays in its payment, as its value will fall in real terms with inflation. This includes inflation-adjusting payments (so that they rise if not paid on time) and having proper penalty rates (that do not fall in real terms just because of inflation).

- Other steps could include improving tax administration (for example by encouraging electronic payments, and more rapid payments), or placing greater reliance on taxes where collection delays are shorter.

- Indexing depreciation allowances with inflation would prevent the erosion of their real value because of inflation, and thus reduce the resulting disincentive to invest. A more direct approach might be to allow full expensing upfront of investment, which could have additional advantages beyond addressing the inflation distortion, as will be discussed in more detail in the following section.

4 Taxation of nominal household income

4.1 Savings income

Most personal income tax systems cover also capital income, though not necessarily at the same rate as labour income. Capital income is typically taxed, irrespective of whether it represents a normal return or an economic rent, and without adjusting for inflation. Another aspect – to which we will return later – is that capital income flows, such as interest and dividends are typically taxed immediately, while capital gains are often taxed only on realization.

Taxing the normal rate of return on savings is well known to distort household savings decisions. The extent of this distortion and the resulting optimal tax rate on normal returns is debated in the literature, with earlier contributions tending to find a rate of zero optimal (Atkinson and Stiglitz, 1976; Chamley, 1986; Judd, 1985), while some more recent papers that relax assumptions of infinite horizons or that give more weight to equity considerations provide arguments for taxing such returns (e.g., Straub and Werning, 2020). The purpose of this paper is not to take a stance in this debate, but to analyse how inflation changes the effective taxation of normal returns and therefore the incentives to save.

To illustrate the effect of taxing savings income, consider a simple economy with zero inflation, a risk-free (or normal) real interest rate of r, and a capital income tax rate of t. In such an economy the real return to saving is reduced by taxation to r(1 – t). This reduction in the rate of return makes future consumption more expensive than it would be without taxation, and therefore likely reduces savings.

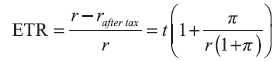

Inflation magnifies this distortion, since all nominal interest income is taxed, reflecting both real interest (which might include the normal rate of return) and inflation. With inflation, π, we assume that the Fisher equation holds,8 so that the nominal return, i, on an asset is given by

| i = (1 + r)(1 + π) – 1 | (1) |

| (2) |

| (3) |

The ETR is increasing in inflation and declines with the rate of return. At the limit, with ever higher inflation, the ETR tends toward t/r. For ever higher returns, the ETR tends toward the statutory tax rate.

To illustrate the order of magnitude of the impact of inflation on ETRs, figure 1 shows a few examples assuming a tax rate of 25 percent and allowing 3 levels of real returns. In the absence of inflation, the ETR matches the statutory tax rate. Inflation, however, raises the ETR, and this effect is particularly strong at low rates of return. For example, with a real rate of return of 2 percent, the ETR reaches 100 percent when inflation hits 6 percent. At current levels of inflation that are close to double digits in many advanced economies, the ETR far exceeds 100 percent (or more generally, quadruple the statutory tax rate). However, even with inflation at 2 percent – which is the target of various advanced economy central banks – the ETR is still doubled for investors expecting to earn a 2 percent real rate of return. For investments with lower real returns (not shown), the ETR would be even higher, tending toward infinity as returns approach zero. And even with negative real returns tax must be paid, as long as the rate of inflation exceeds the real rate of return.

For investments earning higher real rates of return, the effect of inflation on ETRs is more muted. This adds an equity dimension, given that well-off investors are likely to enjoy higher rates of return on average, as they have greater ability to tolerate risk and access to better financial advice.

Figure 1Effective tax rates on real savings returns (in %) DISPLAY Figure

Even proponents of taxing capital are unlikely to support effective tax rates exceeding 100 percent (especially not in case of low returns), and the optimal tax rate – whatever it may be – is unlikely to vary with inflation. These very simple illustrations have shown that in practice such high effective tax rates can occur at combinations of inflation and interest rates that are not unusual. Indeed, effects are even non-negligible when inflation is close to most central banks’ target values.

4.2 Taxation of capital gains

Similar arguments apply to the taxation of capital gains.9 Since the comprehensive income tax base is based on nominal income, higher inflation increases nominal capital gains and thus capital gains tax payments. Just as for interest and dividend income, the real tax rate on capital gains increases as inflation rises, as the nominal component of the gain increases relative to the real gain, and both of these are taxed (Diamond, 1975).

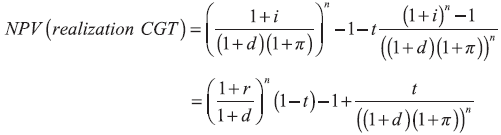

However, an additional complication comes from the fact that capital gains are usually taxed at lower rates than other income. Some jurisdictions exempt them (e.g., Belgium, Hong Kong SAR), some tax them at reduced rates (e.g., Germany, Canada, United States), and others apply standard rates (e.g., Denmark, Czechia).10 Even in the case of standard rates, effective rates on capital gains tend to be lower, because taxation is deferred until realization (with very few exceptions that serve as anti-avoidance measures, such as accrual taxation of zero-coupon bonds in some countries). This realization principle provides a tax advantage for capital gains compared to dividends or interest income which are taxed each period. When looking at a one-period investment, this does not create any difference, but when an investment is held for multiple periods, the effective taxation of capital gains is lower, because such investment compounds at a (higher) untaxed rate of return. Specifically, if an investment yielding capital gains is held for n years, its after-tax value V reaches:

| Vcapital gain = (1 + i)n – t ((1 + i)n – 1) = (1 – t) (1 + i)n + t | (4) |

| (1 – t) (1 + i)n + t ˃ (1 + i(1 – t))n for all n ˃ 1 | (5) |

To analyse the impact of inflation on the tax preference for capital income, we need to consider a multi-period investment. For that we consider the net present value (NPV) of an n year investment, discounted at a real rate of d. The ETR is then the NPV of tax (capital income flow or realized capital gain) divided by the NPV in the absence of tax, 12 with the NPVs given by:

| (6) |

| (7) |

| (8) |

Figure 2 illustrates the impact of inflation on the relative taxation of capital gains and distributed capital income. It assumes a tax rate of 25 percent as before, a real rate of return of 3 percent, and a real discount rate of 0 percent. The figure assumes a 10-year investment horizon. - The figure shows clearly how the tax preference for capital gains rises with inflation. At zero inflation, the ETRs look similar – though the one for the distributing asset is still higher at 28 versus 25 percent, given the accumulation at untaxed interest rate as discussed. For higher rates of inflation, the difference rises dramatically in favour of the investment that yields its return in the form of capital gains. This also implies that the lock-in effect is stronger, the higher the inflation rate.

- The figure also shows, for comparison, a one-year investment (where as noted, there is no difference between taxing accrued capital income or realized capital gains). In general, the longer-term investment has higher ETRs, because of the reduction in the rate of return. When the inflation rate is so high as to lift the ETR above 100 percent, the long-term investment has a lower ETR. Under these circumstances, the investment is loss-making after tax, so having a low return in the first year reduces the amount available for re-investment in such a value-reducing asset.

An additional aspect is that income from saving is often taxed at different rates, with some savings income tax exempt. Exempt capital income typically includes certain savings vehicles, such as pension funds, tax-free savings accounts, and the consumption return from owner-occupied housing. Capital gains, as noted, already benefit from being taxed on realization, but nevertheless in many countries also have preferential rates. Inflation interacts with these tax preferences: - When comparing two assets with the same positive rate of return, inflation unambiguously increases any pre-existing tax preference from lower rates or from taxation at realization.

- When comparing assets with different rates of return, there is ambiguity if the high return asset is also the more highly taxed one. Inflation increases taxation in effective terms, but the impact is smaller on high-return assets.

Figure 2The impact of inflation on the trade-off between capital gains and distributions (in %) DISPLAY Figure

4.3 Human capital

Once it has been shown that taxing nominal capital income leads to distortions, that the under taxation of capital gains leads to a tax preference for taking income in the form of capital gains, and that this tax preference rises with inflation, the natural question arises of whether investment in human capital is similarly affected. Would higher inflation encourage investment in human capital? After all, labour income is also taxed based on nominal rather than real values, and improvements in human capital are untaxed, just like unrealized capital gains in many countries. Closer analysis (Diamond, 1975), however, reveals that these analogies are incorrect and that investment in human capital is affected differently by inflation than investment in financial or real capital. Costs are twofold: forgone earnings while engaging in education and outright payments for education services or goods. In the case of forgone earnings, it is clear to see that inflation has no impact: what is given up now is real earnings, and what is gained is higher real earnings in the future. If inflation boosts earnings in the future by some additional amount, this does not imply any additional taxation. Provided the tax system is designed so as to avoid bracket creep, as discussed above, inflation should not add any additional discouragement of education beyond the one from a progressive labour income tax schedule. In the case of outright payments, these are not deductible in most countries, and certainly not depreciable over time, so that again there is no tax consequence. Moreover, the gain in human capital can only be reaped by earning income through work, it cannot be realized by selling an asset. Labour income is thus appropriately treated differently and, provided there is no bracket creep, it does not require an inflation adjustment even if one is granted to capital income.

4.4 Solutions to taxation of inflationary household income

Finding solutions to the taxation of inflationary gains of households is more complex than fixing the erosion of fixed parameters of the tax system. Fixed parameters can simply be adjusted for inflation but moving away from taxing inflationary gains would imply a more fundamental change in the definition of tax bases. One approach, suggested by Diamond (1975), is to provide a deduction of the inflation rate assessed on the value of assets. His proposal applies irrespective of whether these assets yield capital gains or other capital income, thereby avoiding a preference for capital gains. Partial solutions, such as inflation-adjusting only select income flows, for example capital gains, can exacerbate rather than reduce non-neutralities. Adjusting capital gains for inflation – which is the most common case13 – removes the inflation bias for this type of income. However, if other incomes are not similarly adjusted, it creates a distortion toward a preference for capital gains. In the particular example of capital gains, this exacerbates the existing distortion that arises from taxation at realization. Simplified approaches to addressing the impact of inflation on capital gains, such as lower capital gains tax rates for long-term gains as offered, for example in the United States, similarly exacerbate the existing tax preference for this type of income.

5 Taxation of nominal profits

Like household savings, corporate profits are taxed at their nominal value, but determining corporate profits is certainly more complex than figuring out financial income where there are no (or no significant) costs to offset. Profits, however, are the difference between sales and costs, including deductible financing costs. If sales and related costs always occurred simultaneously (or sufficiently close in time), there would be no issue for the tax system. Inflation would drive up both revenues and costs, and the resulting nominal profit would be higher, but given that CIT is usually charged at a flat rate, this would not have any tax consequence.14

More realistically, even in a very simple business, revenues and costs are spread out over time. When costs are incurred earlier (at lower prices) than corresponding sales, nominal profits are boosted by inflation. This effect rises with the lag between input costs and sales to final customers. Indeed, it is conceivable that a business could sell a good at a real loss, while making a nominal profit, in which case the loss would be compounded by the tax assessed on such nominal profit. Because every business has a different distribution of costs and revenues over time, the real profit cannot be obtained by simply adjusting nominal profits by some inflation-adjustment factor. Most clearly, if a business makes a real loss by selling at prices that exceed nominally but not in real terms input costs, such nominal profit could not be correctly turned into a loss by applying such adjustment. The time lag between incurring costs and receiving profits is particularly long for investment, because the costs are depreciated over time rather than immediately expensed, and thus it merits a more detailed discussion.

5.1 Depreciation

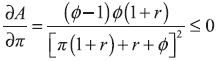

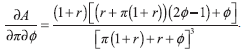

Inflation erodes the NPV of depreciation allowances. Investment I is not treated as an immediately and fully deductible expense in most countries, but instead depreciated over time (and the amount depreciated can be deducted from taxable income each period). Depreciation allowances are based on the historic cost of assets. With an increasing price level, the present value of the depreciation allowance falls increasingly short of the real cost of the asset. To see this effect more formally, denote by A the net present value of depreciation allowances as a share of the investment. When a share ϕ ˃ 0 of the cost of the investment can be deducted each year – that is if depreciation follows the declining balance method – the net present value of the allowances is given by:

| (9) |

Perhaps surprisingly, the effect does not increase monotonically with the durability of assets. This is most readily seen by differentiating expression (9) with respect to π:  | (10) |

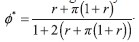

The marginal impact of higher inflation on the NPV of depreciation allowances is thus negative (save for full expensing or zero expensing) and depends on the current level of inflation and the depreciation rate. To illustrate, figure 3.b depicts the marginal reduction in A (on the vertical axis) for assets subject to depreciation rates ranging from 0 to 100 percent (on the horizontal axis). The graph further differentiates between three baseline levels of the inflation rate (0, 10, and 20 percent). The vertical lines depict values ϕ* for which a marginal increase in inflation exerts the largest reduction in A. 17 For instance, when inflation increases marginally from a constant price level (solid line), the NPV of future depreciation allowances declines by up to 5 percentage points and this maximum decline is felt for assets characterized by ϕ* = 0.05. The NPV of depreciation allowances for other assets – both of shorter or longer useful life – declines less. The effect of inflation on A quickly subsides as inflation increases. For instance, when inflation increases marginally from a baseline level of 10 percent, the resulting marginal change in A is just 1.5 percentage points and the maximal decline is experienced for assets with ϕ* = 0.12.

Figure 3The impact of inflation on the NPV of depreciation allowances DISPLAY Figure

As depreciation allowances vary across countries and asset types, inflation could impact asset stocks asymmetrically. Figure 4.a illustrates the distribution of (implied) declining balance depreciation schemes for 68 countries and three different asset types: buildings, tangible assets, and intangible assets, between 2017 and 2020. 18 The mean declining balance rates for these asset types are 10 percent (for buildings), 25 percent (for tangible assets), and 38 percent (for intangible assets). Notably, across countries, there is no statistically significant correlation between the generosity of depreciation allowances and inflation (figure 4.b).

Figure 4Distribution of depreciation rates DISPLAY Figure

| (11) |

| (12) |

If the production function is Cobb-Douglas, a log-linear approximation of this first order condition implies that the (tax-driven) semi-elasticity of investments with respect to inflation is given by 19 | (13) |

For instance, with a corporate tax rate of 22 percent, a depreciation rate of 25 percent and an inflation of 2 percent, the semi-elasticity of capital is 0.42, implying that the optimal investment level would decrease by 0.42 percent in response to a one-percentage point increase in inflation. In the presence of adjustment costs, this response would not happen instantaneously but over several years. Before analysing empirically the impact of changes in A on investment, we need to consider the counteracting impact from greater interest deductibility if the investment is financed partly or fully by debt.

5.2 Debt bias

Another aspect in determining corporate profits is the deductibility of interest. There are various ways to achieve a tax system that does not distort investment decisions: first, by allowing full expensing and denying all interest deductions; second, by setting depreciation allowances at the value of true economic depreciation and then allowing interest deductibility; or third, by offering an allowance for corporate equity (ACE) discussed further below. In the presence of inflation (King, 1977), the first option remains neutral, as inflation cannot erode an immediate deduction, and the value of disregarded interest is irrelevant (King, 1977). For the second option to be neutral, however, interest deductibility should be restricted to the real interest rate, while depreciation should be based on replacement, not historical cost. As will be clear from the analysis below, the deduction of nominal interest will not fully offset the erosion of depreciation allowances, and vice versa.

As is well known (see for example De Mooij, 2011), the deductibility of interest creates a debt bias in corporate financing choices, given the non-deductibility of a similar return to equity. Standard corporate finance models, such as Modigliani and Miller ( 1963) also suggest that – once tax aspects are taken into account – firm value rises with the share of debt finance. The question of interest for this paper is whether such debt preference is affected by inflation.

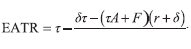

To analyze this, consider the financial effect F of issuing one-period debt of Bt, which pays interest that is tax-deductible: | (14) |

As can be seen in (14), the tax-relevant flows are easily separated out from debt issuance and repayment.

| (16) |

| (17) |

From (17) it can be seen that the cost of capital declines with the debt share. The firm thus issues as much debt as possible, and if loans are limited to the amount of collateral, it will choose a debt share of 100 percent. Before considering how agency costs may lead to an interior solution, we can illustrate the impact with effective tax rates.

Using the framework developed by Devereux and Griffith ( 2003), as adjusted in Klemm ( 2012), and abstracting from investor-level taxes, 20 we can calculate 21 the effective marginal tax rate (EMTR) and the effective average tax rate (EATR). The EMTR is a measure of how investment is distorted at the margin, that is for an investment that just breaks even. The EATR considers a discrete inframarginal investment with some assumed profit rate and then relates the net present value of taxes paid in such projects to the NPV of profits. Both measures are shown in figure 5 for equity and debt finance (i.e., the share of debt is 0 or 100 percent).

Figure 5Effective tax rates as a function of inflation DISPLAY Figure

As illustrated by the figure, 22 rising inflation raises effective tax rates for equityfinanced investments – unsurprisingly given the above analysis of the impact on depreciation allowances and the absence of any countervailing effect. Inflation, however, lowers effective tax rates for debt-financed investment, with the impact from interest deductibility dominating the loss in the value of depreciation allowances. The incentive to finance investments with debt thus clearly intensifies as a result of inflation.

where the cost function c(s) is quadratic, so that where the cost function c(s) is quadratic, so that  with γ parameterizing marginal costs. As γ tends to zero, marginal costs of a given debt share tend to infinity. We add the additional cost component to (11) and differentiate with respect to K and s to obtain optimal investment and financing decisions. Rearranging the first order conditions, we obtain: with γ parameterizing marginal costs. As γ tends to zero, marginal costs of a given debt share tend to infinity. We add the additional cost component to (11) and differentiate with respect to K and s to obtain optimal investment and financing decisions. Rearranging the first order conditions, we obtain: | (18) |

| (19) |

| (20) |

On the one hand, inflation reduces the NPV of depreciation allowances  which increases the cost of capital and thus depresses the optimal investment level. On the other hand, inflation impacts the cost of capital through a debt financing channel. There is a direct and an indirect effect. The direct effect, captured by the second term on the right-hand side in equation (20), is that inflation increases the tax privilege of existing debt, because higher inflation increases nominal, tax deductible interest payments, while leaving real cost unchanged. The indirect effect is that firms that are unconstrained in their financing decision will respond to the reduced cost of debt-financed investments by increasing their share of debt,  which further depresses the cost of capital and increases the optimal investment. This effect is captured by the third term of equation (20).

when s = sc. The optimal debt level is, of course, itself a function of the model’s parameters. Rearranging the condition implies the critical debt level is defined by when s = sc. The optimal debt level is, of course, itself a function of the model’s parameters. Rearranging the condition implies the critical debt level is defined by | (21) |

Figure 6 illustrates critical debt shares sc as a function of depreciation rates, holding constant the real interest rate at 5 percent, the tax rate at 25 percent, and assuming that tax depreciation coincides with economic depreciation. For instance, when the price level is initially constant, a marginal increase in inflation will have no effect on the optimal investment level of companies that lie on the solid line. One such company, depicted by the point on the solid line, is characterized by sc = 0.67 and ϕ = δ = 0.18. Companies that employ the same asset (and thus face the same depreciation rules) but incur higher agency costs are less leveraged and will reduce their optimal investment level in response to the uptick in inflation. In contrast, more highly leveraged firms, lying above the solid line, will increase their investment level. Trivially, for firms that employ assets which are fully deductible in one year or not deductible at all, the debt-financing channel always dominates: these firms will increase their investment volume (which is represented by critical debt shares of zero in the graph). The dashed lines below characterize firms whose optimal investment decision is marginally unaffected at baseline inflation levels of 10 and 20 percent, respectively. Comparing these lines shows that the share of firms that raise their investment volume at the margin increases as inflation rises further (because a larger mass of firms lies above the dashed lines).

Figure 6Critical debt shares as a function of depreciation rates DISPLAY Figure

Accordingly, a marginal increase in inflation tends to reduce the optimal investment volume of firms that (i) face high agency costs, such as micro and small enterprises, (ii) operate in low-inflation environments, and (iii) employ assets with relatively long useful lives (such as buildings).

5.3 Empirical analysis of the inflationary tax effect on investment

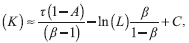

Information on country-level capital stocks can shed light on the importance of inflation for capital accumulation in practice. The conceptual considerations above suggest that inflation should reduce optimal capital stocks because of depreciation but increase the optimal capital stock for debt financed investments. To test which of these effects dominates, we estimate regressions of the form: | Δ% Assetit = β1πit + β2τit + β3πitτit + γ'xit+εit. | (22) |

Table 2 presents results, with columns differentiating between different types of assets. For ease of interpretation, the CIT rate and the inflation rate are centred at their mean and median, respectively. The results suggest that investments decrease by between 0.06 percent (intellectual property) and 0.24 percent (machinery) in response to a one percentage point increase in the CIT rate when inflation is at its median (4 percent in our sample). Those estimates are smaller than that obtained by Ohrn ( 2018), who examines the semi-elasticity of US plant machinery and equipment with respect to effective tax rates and reports an estimate of 4.7 percent. The difference is likely partly related to measurement problems associated with macro data, but it is also due to Ohrn’s use of effective tax rates, which already include the impact of inflation, while our specification considers separately the impact of statutory tax rates and their interaction with inflation. The first-order impact of inflation on investment is statistically insignificant when the CIT rate is at its average (25 percent in our sample). The interaction between inflation and the CIT rate measures the impact of inflation that is propagated through the tax system. For three types of investments (construction, intellectual property, and machinery), we find a statistically significant negative coefficient, suggesting that the eroding value of depreciation allowances outweighs any additional tax benefits from debt finance. The measured effect is strongest for investments in machinery: when the inflation rate is 2 percent, the estimated semi-elasticity of machinery with respect to the CIT rate is 0.17 percent (= -0.241 + 2 x 0.035); but it is 0.45 percent when inflation is at 10 percent (= -0.241-6 x 0.035). The estimated coefficients on the control variables are in line with expectations: investments increase during an upswing in the business cycle (as seen from the negative coefficient on unemployment and the positive coefficient on real GDP growth) while more developed and thus more capital-intensive countries (measured by the log of GDP per capita) experience slower investment growth.

Table 2The impact of inflation on investment DISPLAY Table

5.4 Interaction between corporate and household income

From the discussion of the impact of inflation on interest deductibility for businesses and the taxation of interest returns on savings of households, it is clear the former reduces, and the latter raises, effective taxes, prompting the question of whether the effect washes out economy-wide. This is unlikely to be the case, except under very specific conditions. First, the corporate and the personal income tax rates are not the same in most countries, with the former typically flat and the latter often progressive. It is unlikely for the tax rates for the marginal borrower and the marginal lender to be the same, save for a complete coincidence. Second, even if statutory tax rates matched across borrowers and lenders, the actual marginal lender might not face this same rate, for example, because it is either a tax-exempt pension fund, or a foreign investor (subject to some withholding tax and possibly additional tax in their home country). Third, even if all tax rates are aligned, the demand and supply of savings are unlikely to be equally elastic, hence the real rate of interest could change. Nevertheless, while the impact on households and business are unlikely to wash out perfectly, the offsetting effects on returns to and costs of capital will mitigate the impact of inflation in most cases.

Feldstein and Summers ( 1979) attempt to estimate the net impact on effective tax rates, including both CIT and investor-level taxes. Their calculations suggest that overall inflation increased effective tax rates (defined here as taxes divided by profits) by 50 percent in 1977. Of course, this calculation was done for a different economy and tax system, with one key difference being that there is now a much larger share of foreign investors in the U.S. economy. In any case, even at the time, the calculation was criticized on methodological grounds by Gravelle ( 1980) who argued that it relied on hard-to-make assumptions about what the tax system would have been like in the absence of high inflation, as well as some points regarding how to estimate the value of the replacement cost of capital. Another important angle is that stock prices can be affected by inflation through their interaction with personal and corporate taxes. Taking all mechanisms into account, overall theoretical predictions can be ambiguous with offsetting effects, but under some assumptions the combined interactions would decrease real stock prices, which would have a dampening effect on investment (see Feldstein, 1980; Edwards and Keen, 1985).

Another interaction occurs for small owner-managed businesses, where owners have some liberty to choose the share of income that they wish to declare as profits, which share they declare as salary (within legal constraints that differ across countries). The impact of inflation on that choice will clearly be country specific, but in many cases, one could expect an increase in declared profits over salaries, as the former is typically taxed at a flat rate, while the latter is subject to bracket creep.

5.5 Solutions to the taxation of inflationary profits

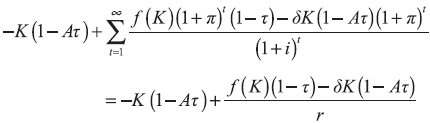

Finding comprehensive solutions to the taxation of inflationary gains at the corporate level is even more complex than for household savings. For corporate income, it would require tracking timings of each flow to be able to figure out the corresponding value of currency

One approach to do this is make tax calculations using fiscal units rather than nominal currency. This is an inflation-adjusted unit of account into which each nominal flow is converted. Depending on the severity of inflation, the conversion rate could be set yearly, quarterly, monthly, or daily. Such an approach would address the problem, but would also be costly to administer, and likely open up many opportunities for tax fraud, as manipulating dates of receipts and costs would have tax consequences. For most countries, the costs of such a system would likely exceed the benefits, especially if inflation is not extremely high or not expected to remain structurally high in the long run.

Nevertheless, some countries have experimented with variants of such systems. For example: - Israel adopted a law in 1982 that dealt comprehensively with inflation, as described and analysed in Sadka (1991). Its main feature was an allowance for inflation that was applied to equity. This removes the additional benefit of debt finance from inflation (but unlike the ACE, discussed below, it does not address the general debt bias). As this achieves a comprehensive deduction of inflationary effects from both debt (through interest deductibility) and equity (through the allowance), it compensates for inflationary gains. Indeed, for capital gains, this allowance overcompensates, so that accrued inflationary capital gains were then made taxable to achieve symmetry (capital gains beyond inflation remained taxable under a realization principle, which is inefficient, but this is unrelated to inflation). Finally, to address the erosion of depreciation allowances, depreciation was calculated at end-ofyear prices. Sadka (1991) also points to various difficulties and loopholes, including that determining the value of equity is tricky when it changes multiple times per year in a high-inflation environment such as Israel in the early 1980s and that industrial equipment and machinery were made exempt from inflation accrual (with the aim of supporting investment in such assets). He also points out that the effectiveness of the law was never put to the test, as inflation had fallen by the time the law had been properly phased in.

- Brazil used various approaches to determine real business incomes, including a system of monetary correction from 1976, and a more comprehensive “integral correction” from 1987. For a description of these systems and the evolution see Doupnik, Martins and Barbieri (1995). While the integral correction was used for accounting purposes, for tax purposes the less complete monetary correction was relevant, which did adjust many, but not all, flows, and notably still taxed inflationary inventory gains.

Alternative tax reform proposals that would change the tax base from total profits to economic rents would also resolve the issue of inflation affecting interest deductions or depreciation allowances. Such reforms have been proposed to make the CIT more efficient: that is, to make it neutral with respect to investment so that any investment that is viable in the absence of taxation would remain so under taxation. A beneficial side-effect is that such taxes can also achieve neutrality with respect to inflation. Two examples of such reforms are cash-flow taxation and the ACE. - There are various ways of implementing a cash flow tax. The one where the neutrality to inflation can be seen most easily is the “R-based” cash flow tax (see Meade, 1978). Under such a tax, investment is immediately expensed, which, as discussed above, reduces the impact of inflation on depreciation allowances to zero. Moreover, such a tax disregards financial flows, so that there is no interest deductibility, removing any impact of inflation through changes in the interest rate.

- The ACE applies deductible notional interest to equity, thereby achieving similar treatment of equity and debt.23 It is neutral with respect to depreciation allowances, and hence also to any inflationary impact on them. This neutrality is achieved because any use of a deduction for depreciation reduces the value of equity, leaving the NPV of taxes unchanged.

6 Conclusions

This paper considered the impact of inflation on the tax system, and specifically the tax distortions created by higher inflation. We grouped the effects into three main categories.

First, non-neutralities caused by the parameters of the tax system being defined in nominal rather than in real terms. These effects include: - Specific taxes or fees (revenues decline in real terms with inflation).

- Fixed nominal interest rate charges on overdue payments (which means lower real rates as inflation rises, thus making payment delays less costly. This itself could also encourage payment delays, for example for negative real interest rates, and thus gradually weakens tax compliance).

- Fixed nominal thresholds for paying taxes or “bracket creep” (typically results in higher real taxes, assuming a progressive income tax).

Second, non-neutralities caused by timing issues: - Collection lags (revenues decline with inflation since they are worth less in real terms by the time they are collected). This can also encourage payment delays (without necessarily becoming overdue).

- Lags in paying refunds, which have the opposite effects to collections.

Third, distortions caused by the fact that the tax base for income and for income tax deductions is defined in nominal terms, so that nominal rather than real income is taxed: - Taxation of the nominal return on savings (rather than just the real return) means that higher inflation leads to higher tax payments and thus a further reduction in the real after-tax rate of return.

- Taxation of nominal rather than real capital gains means that higher inflation leads to higher capital taxation and increases lock-in effects (since this higher taxation only occurs on realization).

- Loss in the real value of depreciation allowances that are fixed in nominal terms (higher real revenues but at the cost of discouraging investment).

- Conversely higher inflation increases nominal debt interest payments, allowing greater deductibility from taxable income (and thus increasing the bias towards debt over equity).

That said, the cutoff between these three groups is at times arbitrary. For example, the impact of depreciation allowances is both because depreciation is only allowed over time (timing effects), but also because the allowances are typically specified in nominal terms (taxation of nominal gains). Likewise for the taxation of nominal capital gains: non-neutrality is caused by the delay in taxing capital gains (only on realization) and by the failure to index capital gains for inflation

Many of the potential distortions having been covered, the question arises of gauging their relative importance. This will depend on each country’s specific circumstances, notably the nature of the tax system that they have in place, and also how high the inflation rate is. Consider first an economy that has a strong reliance on personal income and general consumption taxes, with a monetary policy that generally ensures low inflation (i.e., a typical advanced economy). In such a case, bracket creep is likely to be the most pronounced problem, because even low inflation will cumulate over time. If, as is typical, capital gains are relatively undertaxed, then the tax preference toward these is increased by inflation. Consumption taxes are unlikely to create issues. Conversely, in an economy with less reliance on income taxes, and where an important share of consumption taxes is collected through specific excises, but where inflation is still low (e.g., a developing country with strong macroeconomic policies), erosion of the real value of excises would be a more pressing issue. Finally, in economies with very high inflation rates, timing issues might dominate all other effects, as the delay in tax payments rapidly erodes their real value (and very high inflation rates might create incentives to lengthen this delay). Of course, any of these effects might already be addressed by reform to the design of the tax system (e.g., indexation of thresholds), in which case their relevance would be diminished.

Another concluding question is the overall impact of inflation on tax revenue of these various effects that at times act against each other. Gains from revenue due to bracket creep (larger in countries with progressive income tax systems, which are typically higher income countries) need to be offset against the revenue loss from collection delays (more important for countries with weaker tax administration or higher inflation rates). Likewise in terms of incentives for savings and investment: higher inflation reduces the after-tax rate of return on saving but could lower the cost of debt finance of investment. That said, the impact of the various distortions identified in this paper can be quite large, even at relatively modest inflation rates.

Solutions vary both in nature and in scope. For many of the problems we identified, narrow solutions exist that are fairly easy (technically at least) to implement, though they might face political obstacles. For example, adjusting the basic parameters of the tax system (automatically) in line with inflation. More comprehensive solutions addressing all timing issues and relating to the taxation of nominal gains would be complex. Some simpler solutions, such as increased use of withholding taxes, increasing advance CIT payments, more frequent asset revaluations (say of house values for property tax) would not eliminate timing issues, but help reduce their impact. Some broader tax reforms, such as corporate cash-flow taxes or ACE systems would involve a more fundamental change, but have the advantage of increasing efficiency, as they tax only economic rents and thereby avoid distorting investment decisions.

For simplicity and to preserve neutrality, when adjusting the parameters of the tax system (thresholds, interest rates on overdue tax payments, specific taxes, the measurement of capital income), the same inflation rate should generally be used throughout. Consider specific taxes: if the fuel price increases, the fuel duty would increase but only in line with increases in the general price level. Likewise for wages: the threshold would not increase with wage increases, but only with some general measure of price increases. 24 Since the GDP deflator is only available with a lag, and is subject to revision, this would suggest indexing or adjusting parameters based on CPI inflation. For corporate incomes, the issue might be confusing: with different deflators being available for capital goods, producer, and consumer prices, one might wonder whether separate deflators should be used. If the aim is neutrality with respect to overall inflation, this should be avoided. A firm that buys inputs (including capital), whose prices change at different rates from general inflation, makes real valuation gains or losses, and there is no need to remove those relative gains or losses from the tax base.

The arguments could also be extended to the case of deflation which, until recently, was a pre-occupation of policymakers, and where the effects would operate in the opposite direction. Thus, specific taxes, fees, interest rates, thresholds would need to be reduced in line with the deflation. Collection lags and payments delays would lessen endogenously, and there could even be incentives for pre-payment if positive balances earn interest, while depreciation allowances would become too generous. Nominal capital gains and hence capital income taxes would fall as the real gains due to deflation would escape tax. Conversely the value of the interest rate deduction would fall since nominal interest rates would be lower, and the real value of the existing debt increase as the price level falls.

With the great difficulties in comprehensively addressing all distortions arising from inflation, one practical approach would be to focus on those where the costs to efficiency are likely high and the solution relatively simple, while simultaneously making efforts to bring inflation back down. However, such a selective approach would need to be careful in avoiding problems of the second best. Plus, the distributional impact should be considered too, which might require compensating measures. And quickly reducing inflation may be easier said than done: if the path to lower inflation takes longer, this will strengthen the need for gradually designing a more inflation-proof tax system, along the lines considered in this paper. Not to mention measures on the spending side (including government wages), which we have not considered in this paper, but where the combination of inflation and fixed nominal spending totals may lead to cuts in real government spending, and which would also seem a candidate for “inflation-proofing”.

Notes

* The views expressed in this paper are those of the authors and do not necessarily represent the views of the IMF, its Executive Board, or IMF management. The authors would like to thank Yongquan Cao, Ruud de Mooij, Andrea Lemgruber, Simon Naitram, two anonymous referees, as well as IMF and NIPFP seminar participants for valuable comments and Aieshwarya Davis for research assistance.

1 Key contributions include Diamond (1975), King (1977, chapter 8), Aaron 1976).

2 The same can also hold for the spending side if real public spending is not neutral with respect to inflation (for example, if spending items such as government wages or public pensions do not rise one for one with prices).

3 Keen (1998) provides a broader discussion of specific versus ad valorem excises. Even absent externalities, there can be interesting tradeoffs, at least when competition is imperfect, or goods vary in quality. For identical goods, under perfect competition, there is no difference in specific or ad valorem taxes. Under a monopoly, however, ad valorem taxes can be shown to lead to both higher consumer welfare and profits. Results are ambiguous under oligopolistic competition. Considering goods of variable quality, specific taxes create stronger incentives to improve goods’ quality.

4 We have not found current examples of foreign-currency excises. Foreign-currency tariffs are also exceedingly rare, but there are some examples (e.g., East African Community).

5 Some countries (e.g., United States, Austria) link the rate to a flexible benchmark, such as the central bank’s policy rate, plus a fixed surcharge, which provides some protection against inflation, as interest rates will generally be higher in inflationary times. Other countries adjust such rates rarely (e.g., Germany requires revisions only once every three years and only since 2021), making it more likely that the rate does not reflect changes in the inflationary environment.

6 We found flat rate systems without general personal allowances, credits, or threshold in only 7 jurisdictions: Armenia, Bulgaria, Georgia, Hungary, Montenegro, Ukraine, and Uzbekistan.

7 This may not hold anymore, as the UK system has more brackets now than at the time of the study, including because of a provision to phase out the personal allowance for incomes above around £100,000.

8 In practice this assumption may not hold, and even in general equilibrium models it often does not hold in the presence of taxation (see Feldstein, 1976). Nevertheless, this is a useful starting point, if one wants to show that even in an otherwise fully adjusting economy, the tax system creates distortions.

9 Another aspect is that unexpected inflation will have potentially very large effects on capital gains. Fixed income assets and liabilities would immediately lose value. Related gains would typically remain untaxed unless realized.

10 See pwc Capital Gains Tax Rates.

11 Auerbach (1991) suggested a capital gains tax with no such effect, where taxation is based on the number of years an asset is held and a statutory rate of return, not on the true capital gain. Such a tax has not been tried in practice.

12 Note that the NPV in the absence of tax is completely independent of the inflation rate, because inflation cancels out of the fraction. This is expected, given the argument that expected inflation should not affect real decisions such as investment.

13 A review of tax laws revealed that Botswana, Chile, Colombia, Cyprus, the Dominican Republic, Israel, Mexico, Luxembourg, and Portugal provided relief for inflationary capital gains, while the United Kingdom and Ireland did so in the past.

14 Some countries have lower rates for small businesses or low profits, and the thresholds for those should of course be adjusted as discussed in the previous section.

15 This also holds for depreciation methods other than declining balance, as long as the total nominal amount to be deducted equals the cost of the asset. If, for example, straight line depreciation is used, the formula for the present value changes to:

16 The choice of a rate of 5 percent is supported by Reis (2021) who reports that the 10-year ahead expectation of US stock returns was around 5 percent in 2019 (and higher before). Real returns will of course vary across sectors and countries, partly depending on underlying risk.

17 Differentiating (2) with respect to ϕ we obtain:  The critical values are given by setting this equation equal to zero and solving for the depreciation rate, which gives The critical values are given by setting this equation equal to zero and solving for the depreciation rate, which gives

18 Data are taken from the OECD’s effective tax rate database, which provides information on A for a hypothetical low interest (5 percent) and low inflation (2 percent) environment. The implied declining balance tax rates are calculated from A using

19 This follows from rewriting the first-order condition as  where β is the capital share in total costs of production and C summarizes irrelevant constants. Combining this expression with the assumption that total real demand remains unchanged d = β ln(K) + (1 – β) ln(L) and differentiating K with respect to inflation gives equation (13). where β is the capital share in total costs of production and C summarizes irrelevant constants. Combining this expression with the assumption that total real demand remains unchanged d = β ln(K) + (1 – β) ln(L) and differentiating K with respect to inflation gives equation (13).

20 That is taxes on dividends, capital gains, and interest. In terms of the Devereux-Griffith model this implies that the discount rate r is equal to the nominal interest rate i, and the factor that values dividends g equals 1. This assumption can be justified because the investor might be a tax-exempt pension fund, tax-favoured foreign investor, or simply because we wish to focus on the corporate side of taxation.

21 The calculation is closely related to the framework discussed here. One difference is that in the Devereux-Griffith model, first-year depreciation is instantaneous, so that firms only need to fund 1 – τϕ of an investment. The resulting tax rates are thus defined as  and and  Another point is that in the Devereux-Griffith model, investment is a one period perturbation of the capital stock with subsequent sale, while in the Klemm version it is a permanent investment that is allowed to depreciate; however, under a range of reasonable assumptions all approaches lead to the same first order conditions. A minor point is that Devereux and Griffith (2003) define A as the NPV of the tax saving from depreciation allowances, but for consistency with our definition above, our A is simply the NPV of depreciation allowances, and hence we multiply it by the tax rate τ to obtain the tax saving. Another point is that in the Devereux-Griffith model, investment is a one period perturbation of the capital stock with subsequent sale, while in the Klemm version it is a permanent investment that is allowed to depreciate; however, under a range of reasonable assumptions all approaches lead to the same first order conditions. A minor point is that Devereux and Griffith (2003) define A as the NPV of the tax saving from depreciation allowances, but for consistency with our definition above, our A is simply the NPV of depreciation allowances, and hence we multiply it by the tax rate τ to obtain the tax saving.

22 The negative debt-finance EMTR with extremely high absolute value is caused by dividing by a denominator (the cost of capital) that is very close to zero. The resulting figure is thus somewhat unintuitive, which is, however, a common phenomenon with this measure. The negative rate means that a marginal investment turns out to have a tax loss (because the interest and depreciation deductions are greater than the profit). Such a tax loss can be used to reduce taxes from other activities or in the future. In the absence of other profits, the tax rate is bound by zero, because revenue authorities do not pay out tax refunds on tax losses.

23 The ACE does not achieve full symmetry, because the interest rate on debt will be firm specific and could be different (and often higher) than the notional rate on equity. A solution that achieves full symmetry is the allowance for corporate capital, which denies the standard interest deduction, and instead applies the same notional interest rate to equity and debt (Kleinbard, 2005).

24 One could argue for adjusting thresholds in line with average wage increases, thereby keeping the tax rate the same for the average earner and in relation to the average earner. However, this would mean a reduction in real taxes as real incomes rise – certainly a policy option, but one that goes beyond inflation neutrality.

* The views expressed in this paper are those of the authors and do not necessarily represent the views of the IMF, its Executive Board, or IMF management. The authors would like to thank Yongquan Cao, Ruud de Mooij, Andrea Lemgruber, Simon Naitram, two anonymous referees, as well as IMF and NIPFP seminar participants for valuable comments and Aieshwarya Davis for research assistance.

1 Key contributions include Diamond ( 1975), King ( 1977, chapter 8), Aaron 1976).