7477

Views

364

Downloads |

The euro and inflation in Croatia: much ado about nothing?

Petar Sorić*

Article | Year: 2024 | Pages: 1 - 37 | Volume: 48 | Issue: 1 Received: June 1, 2023 | Accepted: October 25, 2023 | Published online: March 1, 2024

|

FULL ARTICLE

FIGURES & DATA

REFERENCES

CROSSMARK POLICY

METRICS

LICENCING

PDF

Note: Vertical dotted line corresponds to September 2022 (start of obligatory dual display of

prices). Vertical full line corresponds to January 2023 (euro changeover). Inflation expectations

are quantified as the response balance to question 6 from the EU Consumer Survey (see section

3 for details). Source: Eurostat and European Commission.

|

January

|

February

|

March

|

April

|

May

|

June

|

July

|

|

hicp

|

1.704

|

0.974

|

1.589

|

0.508

|

1.199

|

2.062

|

2.038

|

|

(0.038)

|

(0.291)

|

(0.155)

|

(0.601)

|

(0.235)

|

(0.038)

|

(0.014)

|

|

food

|

0.065

|

0.203

|

0.823

|

2.748

|

3.927

|

4.889

|

3.615

|

|

(0.986)

|

(0.934)

|

(0.648)

|

(0.127)

|

(0.019)

|

(0.005)

|

(0.028)

|

|

nonalc

|

0.202

|

-1.845

|

-1.570

|

-0.002

|

1.971

|

3.038

|

2.653

|

|

(0.864)

|

(0.315)

|

(0.390)

|

(0.977)

|

(0.296)

|

(0.089)

|

(0.113)

|

|

alc

|

1.077

|

-0.522

|

-2.041

|

-1.794

|

-1.449

|

-1.294

|

-1.374

|

|

(0.577)

|

(0.826)

|

(0.282)

|

(0.343)

|

(0.498)

|

(0.545)

|

(0.516)

|

|

clothing

|

8.225

|

5.901

|

3.294

|

3.419

|

2.121

|

4.385

|

7.374

|

|

(0.005)

|

(0.014)

|

(0.202)

|

(0.174)

|

(0.441)

|

(0.094)

|

(0.005)

|

|

housing

|

4.362

|

3.626

|

0.800

|

-1.105

|

-1.182

|

-0.703

|

-0.086

|

|

(0.244)

|

(0.371)

|

(0.930)

|

(0.718)

|

(0.681)

|

(0.812)

|

(0.953)

|

|

furnish

|

1.463

|

1.014

|

0.181

|

-1.211

|

0.699

|

1.165

|

2.154

|

|

(0.061)

|

(0.197)

|

(0.817)

|

(0.117)

|

(0.380)

|

(0.131)

|

(0.019)

|

|

health

|

2.386

|

1.795

|

1.539

|

1.782

|

2.831

|

4.098

|

4.364

|

|

(0.188)

|

(0.324)

|

(0.385)

|

(0.366)

|

(0.169)

|

(0.023)

|

(0.019)

|

|

transport

|

-0.835

|

-0.373

|

-0.761

|

-1.722

|

-1.421

|

0.198

|

1.109

|

|

(0.577)

|

(0.751)

|

(0.592)

|

(0.300)

|

(0.352)

|

(0.901)

|

(0.479)

|

|

commun

|

-1.623

|

-1.662

|

-1.034

|

-0.097

|

0.167

|

-0.979

|

1.647

|

|

0.277)

|

(0.277)

|

(0.521)

|

(0.962)

|

(0.911)

|

(0.540)

|

(0.291)

|

|

recr

|

-0.802

|

-2.032

|

-3.410

|

-3.965

|

-4.310

|

-3.545

|

-0.533

|

|

(0.549)

|

(0.188)

|

(0.056)

|

(0.033)

|

(0.023)

|

(0.075)

|

(0.789)

|

|

educ

|

1.970

|

1.718

|

2.299

|

2.465

|

2.084

|

2.683

|

3.560

|

|

(0.235)

|

(0.277)

|

(0.192)

|

(0.178)

|

(0.239)

|

(0.174)

|

(0.061)

|

|

rest

|

4.340

|

3.701

|

4.391

|

5.276

|

6.890

|

9.087

|

7.024

|

|

(0.028)

|

(0.052)

|

(0.038)

|

(0.038)

|

(0.014)

|

(0.005)

|

(0.009)

|

|

misc

|

1.501

|

-0.049)

|

0.269

|

0.298

|

1.219

|

0.915

|

0.930

|

|

(0.103)

|

(0.930)

|

(0.756)

|

(0.732)

|

(0.188)

|

(0.371)

|

(0.366)

|

Note: Table entries are gaps between actual and synthetic values of corresponding variables. Positive gaps imply that actual values are greater than the synthetic ones. P-values are given in parentheses. Bold entries are significant at the 5% level. Source: Author’s calculation.

|

January

|

February

|

March

|

April

|

May

|

June

|

July

|

|

hicp

|

0.862

|

0.220

|

-0.439

|

-1.225

|

-0.348

|

0.700

|

0.905

|

|

(0.315)

|

(0.817)

|

(0.704)

|

(0.225)

|

(0.761)

|

(0.460)

|

(0.282)

|

|

food

|

-1.402

|

-0.719

|

0.210

|

2.590

|

4.231

|

4.850

|

3.442

|

|

(0.451)

|

(0.718)

|

(0.930)

|

(0.117)

|

(0.019)

|

(0.005)

|

(0.056)

|

|

nonalc

|

-0.612

|

-2.586

|

-2.417

|

-0.793

|

0.886

|

2.662

|

2.688

|

|

(0.657)

|

(0.136)

|

(0.164)

|

(0.568)

|

(0.549)

|

(0.113)

|

(0.108)

|

|

alc

|

0.795

|

-0.825

|

-2.113

|

-2.496

|

-1.738

|

-1.836

|

-1.922

|

|

(0.695)

|

(0.690)

|

(0.258)

|

(0.216)

|

(0.404)

|

(0.343)

|

(0.315)

|

|

clothing*

|

8.225

|

5.901

|

3.294

|

3.419

|

2.121

|

4.385

|

7.374

|

|

(0.005)

|

(0.014)

|

(0.202)

|

(0.174)

|

(0.441)

|

(0.094)

|

(0.005)

|

|

housing

|

1.024

|

-0.102

|

-1.555

|

-4.839

|

-5.390

|

-4.619

|

-3.682

|

|

(0.878)

|

(0.911)

|

(0.648)

|

(0.225)

|

(0.207)

|

(0.225)

|

(0.286)

|

|

furn*

|

1.463

|

1.014

|

0.181

|

-1.211

|

0.699

|

1.165

|

2.154

|

|

(0.061)

|

(0.197)

|

(0.817)

|

(0.117)

|

(0.380)

|

(0.131)

|

(0.019)

|

|

health

|

2.561

|

2.029

|

1.754

|

1.802

|

3.153

|

5.098

|

5.287

|

|

(0.178)

|

(0.272)

|

(0.315)

|

(0.347)

|

(0.136)

|

(0.019)

|

(0.019)

|

|

transport

|

0.143

|

1.034

|

1.717

|

0.866

|

-0.112

|

1.376

|

2.172

|

|

(0.958)

|

(0.568)

|

(0.333)

|

(0.554)

|

(0.948)

|

(0.352)

|

(0.160)

|

|

commun

|

-2.028

|

-2.431

|

-2.058

|

-0.566

|

-0.586

|

-1.993

|

0.860

|

|

(0.239)

|

(0.169)

|

(0.258)

|

(0.700)

|

(0.695)

|

(0.263)

|

(0.592)

|

|

recr*

|

-0.802

|

-2.032

|

-3.410

|

-3.965

|

-4.310

|

-3.545

|

-0.533

|

|

(0.549)

|

(0.188)

|

(0.056)

|

(0.033)

|

(0.023)

|

(0.075)

|

(0.789)

|

|

educ

|

1.564

|

1.156

|

1.313

|

1.476

|

1.178

|

1.577

|

2.260

|

|

(0.319)

|

(0.451)

|

(0.390)

|

(0.366)

|

(0.446)

|

(0.324)

|

(0.188)

|

|

rest

|

4.222

|

3.531

|

4.176

|

5.265

|

6.417

|

8.837

|

6.821

|

|

(0.028)

|

(0.052)

|

(0.042)

|

(0.042)

|

(0.009)

|

(0.005)

|

(0.009)

|

|

misc

|

1.808

|

0.682

|

0.737

|

0.985

|

1.521

|

0.618

|

0.770

|

|

(0.099)

|

(0.455)

|

(0.418)

|

(0.300)

|

(0.127)

|

(0.488)

|

(0.413)

|

Note: Table entries are gaps between actual and synthetic values of corresponding variables. Positive gaps imply that actual values are greater than the synthetic ones. P-values are given in parentheses. Bold entries are significant at the 5% level. * Denotes specifications with no MSPEs three times larger than the Croatian one (leaving the baseline ASCM results intact). Source: Author’s calculation.

|

January

|

February

|

March

|

April

|

May

|

June

|

July

|

|

hicp

|

2.678

|

1.626

|

2.478

|

0.853

|

0.506

|

1.174

|

1.298

|

|

(0.355)

|

(0.595)

|

(0.397)

|

(0.769)

|

(0.81)

|

(0.636)

|

(0.554)

|

|

food

|

4.521

|

3.286

|

2.543

|

3.220

|

3.441

|

4.811

|

3.721

|

|

(0.157)

|

(0.306)

|

(0.372)

|

(0.215)

|

(0.149)

|

(0.025)

|

(0.074)

|

|

nonalc

|

1.124

|

-3.245

|

-3.583

|

-3.264

|

-2.031

|

0.215

|

-1.607

|

|

(0.736)

|

(0.339)

|

(0.413)

|

(0.463)

|

(0.62)

|

(0.95)

|

(0.463)

|

|

alc

|

2.783

|

1.040

|

-0.778

|

-0.455

|

-0.454

|

0.287

|

0.141

|

|

(0.215)

|

(0.579)

|

(0.678)

|

(0.851)

|

(0.843)

|

(0.959)

|

(0.992)

|

|

clothing

|

8.871

|

6.440

|

2.785

|

3.413

|

1.813

|

4.148

|

7.803

|

|

(0.008)

|

(0.033)

|

(0.421)

|

(0.174)

|

(0.636)

|

(0.083)

|

(0.008)

|

|

housing

|

-22.051

|

-16.597

|

-12.641

|

-27.614

|

-29.643

|

-20.988

|

-15.951

|

|

(0.612)

|

(0.562)

|

(0.653)

|

(0.388)

|

(0.372)

|

(0.397)

|

(0.512)

|

|

furn

|

6.726

|

5.535

|

4.894

|

3.677

|

3.762

|

3.114

|

3.022

|

|

(0.008)

|

(0.008)

|

(0.008)

|

(0.008)

|

(0.008)

|

(0.008)

|

(0.008)

|

|

health

|

-4.891

|

-5.445

|

-4.343

|

-5.334

|

-3.745

|

-1.526

|

-2.173

|

|

(0.099)

|

(0.066)

|

(0.165)

|

(0.215)

|

(0.355)

|

(0.711)

|

(0.57)

|

|

transport

|

-0.613

|

-0.533

|

-0.916

|

-0.845

|

-1.627

|

-0.587

|

0.558

|

|

(0.727)

|

(0.744)

|

(0.694)

|

(0.645)

|

(0.463)

|

(0.744)

|

(0.835)

|

|

commun

|

-0.076

|

-0.094

|

0.471

|

1.884

|

1.886

|

-0.362

|

3.159

|

|

(0.975)

|

(0.975)

|

(0.818)

|

(0.405)

|

(0.397)

|

(0.851)

|

(0.207)

|

|

recr

|

-6.616

|

-7.152

|

-8.661

|

-9.315

|

-8.989

|

-5.424

|

2.099

|

|

(0.231)

|

(0.165)

|

(0.14)

|

(0.058)

|

(0.033)

|

(0.149)

|

(0.545)

|

|

educ

|

13.190

|

13.044

|

13.313

|

12.737

|

12.811

|

13.079

|

13.782

|

|

(0.223)

|

(0.231)

|

(0.223)

|

(0.24)

|

(0.248)

|

(0.231)

|

(0.223)

|

|

rest

|

12.742

|

12.243

|

13.025

|

11.675

|

11.423

|

12.661

|

9.611

|

|

(0.033)

|

(0.033)

|

(0.033)

|

(0.033)

|

(0.025)

|

(0.017)

|

(0.025)

|

|

misc

|

3.894

|

2.993

|

2.967

|

2.476

|

2.331

|

1.888

|

1.904

|

|

(0.017)

|

(0.05)

|

(0.025)

|

(0.05)

|

(0.074)

|

(0.091)

|

(0.099)

|

Note: Table entries are gaps between actual and synthetic values of corresponding variables. Positive gaps imply that actual values are greater than the synthetic ones. P-values are given in parentheses. Bold entries are significant at the 5% level. Source: Author’s calculation.

|

January

|

February

|

March

|

April

|

May

|

June

|

July

|

|

hicp

|

3.285

|

2.245

|

2.821

|

1.683

|

2.210

|

3.117

|

2.998

|

|

(0.005)

|

(0.038)

|

(0.043)

|

(0.215)

|

(0.048)

|

(0.01)

|

(0.005)

|

|

food

|

1.832

|

1.994

|

2.338

|

4.398

|

4.890

|

5.469

|

3.203

|

|

(0.378)

|

(0.359)

|

(0.282)

|

(0.033)

|

(0.01)

|

(0.005)

|

(0.067)

|

|

nonalc

|

2.052

|

-0.339

|

0.642

|

2.290

|

3.811

|

4.546

|

3.525

|

|

(0.297)

|

(0.809)

|

(0.727)

|

(0.301)

|

(0.062)

|

(0.014)

|

(0.053)

|

|

alc

|

0.946

|

-0.674

|

-2.200

|

-1.948

|

-1.599

|

-1.388

|

-1.437

|

|

(0.627)

|

(0.756)

|

(0.278)

|

(0.321)

|

(0.459)

|

(0.536)

|

(0.512)

|

|

clothing

|

7.889

|

5.817

|

3.118

|

3.143

|

2.098

|

3.728

|

7.265

|

|

(0.005)

|

(0.019)

|

(0.187)

|

(0.158)

|

(0.373)

|

(0.091)

|

(0.005)

|

|

housing

|

5.608

|

4.200

|

1.014

|

-2.075

|

-2.172

|

-1.993

|

-0.969

|

|

(0.474)

|

(0.565)

|

(0.938)

|

(0.689)

|

(0.651)

|

(0.641)

|

(0.77)

|

|

furn

|

2.542

|

1.932

|

1.136

|

-0.299

|

1.425

|

1.600

|

2.469

|

|

(0.01)

|

(0.033)

|

(0.196)

|

(0.684)

|

(0.1)

|

(0.043)

|

(0.005)

|

|

health

|

2.516

|

1.926

|

1.670

|

1.929

|

2.990

|

4.239

|

4.506

|

|

(0.182)

|

(0.301)

|

(0.388)

|

(0.349)

|

(0.172)

|

(0.024)

|

(0.019)

|

|

transport

|

-0.216

|

-0.013

|

-0.837

|

-1.878

|

-1.846

|

-0.042

|

0.702

|

|

(0.809)

|

(0.952)

|

(0.574)

|

(0.244)

|

(0.263)

|

(0.947)

|

(0.651)

|

|

commun

|

-1.781

|

-1.922

|

-0.374

|

0.529

|

0.879

|

-0.322

|

2.579

|

|

(0.254)

|

(0.23)

|

(0.852)

|

(0.742)

|

(0.569)

|

(0.861)

|

(0.124)

|

|

recr

|

-1.670

|

-2.882

|

-4.296

|

-4.707

|

-4.951

|

-4.009

|

-0.692

|

|

(0.378)

|

(0.163)

|

(0.053)

|

(0.033)

|

(0.024)

|

(0.067)

|

(0.77)

|

|

educ

|

1.971

|

1.721

|

2.179

|

2.330

|

1.919

|

2.477

|

3.333

|

|

(0.603)

|

(0.636)

|

(0.569)

|

(0.541)

|

(0.612)

|

(0.522)

|

(0.397)

|

|

rest

|

7.230

|

6.572

|

7.063

|

7.692

|

9.500

|

11.415

|

9.530

|

|

(0.01)

|

(0.01)

|

(0.01)

|

(0.014)

|

(0.01)

|

(0.005)

|

(0.01)

|

|

misc

|

3.126

|

1.891

|

1.727

|

1.115

|

1.649

|

1.383

|

1.158

|

|

(0.01)

|

(0.11)

|

(0.11)

|

(0.268)

|

(0.1)

|

(0.201)

|

(0.273)

|

Note: Table entries are gaps between actual and synthetic values of corresponding variables. Positive gaps imply that actual values are greater than the synthetic ones. P-values are given in parentheses. Bold entries are significant at the 5% level. Source: Author’s calculation.

|

January

|

February

|

March

|

April

|

May

|

June

|

July

|

|

hicp

|

1.988

|

1.196

|

1.884

|

0.768

|

1.429

|

2.275

|

2.234

|

|

(0.024)

|

(0.212)

|

(0.108)

|

(0.472)

|

(0.189)

|

(0.028)

|

(0.005)

|

|

food

|

0.280

|

0.353

|

1.023

|

2.935

|

4.014

|

4.961

|

3.604

|

|

(0.901)

|

(0.882)

|

(0.559)

|

(0.113)

|

(0.024)

|

(0.005)

|

(0.028)

|

|

nonalc

|

-0.018

|

-2.062

|

-1.764

|

-0.213

|

1.533

|

2.949

|

2.625

|

|

(0.981)

|

(0.255)

|

(0.354)

|

(0.896)

|

(0.382)

|

(0.108)

|

(0.132)

|

|

alc

|

1.103

|

-0.491

|

-2.010

|

-1.754

|

-1.148

|

-1.276

|

-1.362

|

|

(0.571)

|

(0.844)

|

(0.288)

|

(0.368)

|

(0.509)

|

(0.552)

|

(0.524)

|

|

clothing

|

8.193

|

6.030

|

3.455

|

3.351

|

2.372

|

4.265

|

7.397

|

|

(0.005)

|

(0.009)

|

(0.16)

|

(0.156)

|

(0.349)

|

(0.08)

|

(0.005)

|

|

housing

|

4.264

|

3.606

|

0.971

|

-1.116

|

-1.014

|

-0.719

|

-0.274

|

|

(0.335)

|

(0.462)

|

(0.939)

|

(0.741)

|

(0.741)

|

(0.802)

|

(0.915)

|

|

furn

|

1.755

|

1.190

|

0.488

|

-0.790

|

0.936

|

1.357

|

2.262

|

|

(0.028)

|

(0.156)

|

(0.491)

|

(0.349)

|

(0.264)

|

(0.118)

|

(0.009)

|

|

health

|

2.431

|

1.840

|

1.588

|

1.836

|

2.889

|

4.155

|

4.422

|

|

(0.184)

|

(0.311)

|

(0.382)

|

(0.358)

|

(0.17)

|

(0.024)

|

(0.019)

|

|

transport

|

-0.822

|

-0.596

|

-1.142

|

-2.081

|

-1.851

|

-0.048

|

0.814

|

|

(0.566)

|

(0.632)

|

(0.472)

|

(0.217)

|

(0.259)

|

(0.892)

|

(0.608)

|

|

commun

|

-1.749

|

-1.682

|

-0.932

|

-0.004

|

0.254

|

-0.966

|

1.789

|

|

(0.269)

|

(0.311)

|

(0.604)

|

(1.000)

|

(0.868)

|

(0.594)

|

(0.269)

|

|

recr

|

-0.868

|

-2.090

|

-3.474

|

-4.006

|

-4.354

|

-3.561

|

-0.498

|

|

(0.528)

|

(0.203)

|

(0.057)

|

(0.033)

|

(0.024)

|

(0.075)

|

(0.811)

|

|

educ

|

1.980

|

1.726

|

2.335

|

2.504

|

2.130

|

2.737

|

3.618

|

|

(0.245)

|

(0.292)

|

(0.203)

|

(0.193)

|

(0.245)

|

(0.179)

|

(0.066)

|

|

rest

|

4.950

|

4.365

|

4.982

|

5.787

|

7.391

|

9.592

|

7.653

|

|

(0.024)

|

(0.033)

|

(0.028)

|

(0.028)

|

(0.009)

|

(0.005)

|

(0.009)

|

|

misc

|

1.963

|

0.501

|

0.695

|

0.594

|

1.495

|

1.238

|

1.218

|

|

(0.028)

|

(0.604)

|

(0.462)

|

(0.495)

|

(0.127)

|

(0.212)

|

(0.212)

|

Note: Table entries are gaps between actual and synthetic values of corresponding variables. Positive gaps imply that actual values are greater than the synthetic ones. P-values are given in parentheses. Bold entries are significant at the 5% level. Source: Author’s calculation.

|

January

|

February

|

March

|

April

|

May

|

June

|

July

|

|

meat

|

-1.283

|

-2.973

|

-0.734

|

2.335

|

0.091

|

0.432

|

-1.780

|

|

(0.521)

|

(0.178)

|

(0.770)

|

(0.362)

|

(0.986)

|

(0.915)

|

(0.484)

|

|

fish

|

-1.923

|

-3.275

|

-4.825

|

-5.100

|

-1.459

|

1.442

|

-0.095

|

|

(0.404)

|

(0.146)

|

(0.070)

|

(0.047)

|

(0.535)

|

(0.559)

|

(0.972)

|

|

milk

|

-2.491

|

-1.951

|

0.767

|

0.471

|

4.049

|

4.818

|

1.808

|

|

(0.352)

|

(0.507)

|

(0.803)

|

(0.854)

|

(0.164)

|

(0.117)

|

(0.432)

|

|

fruit

|

-4.303

|

-3.349

|

1.101

|

2.744

|

3.368

|

4.127

|

2.787

|

|

(0.277)

|

(0.380)

|

(0.779)

|

(0.455)

|

(0.366)

|

(0.296)

|

(0.455)

|

|

veg

|

-8.104

|

-4.751

|

2.806

|

3.644

|

4.121

|

7.153

|

7.649

|

|

(0.136)

|

(0.357)

|

(0.601)

|

(0.446)

|

(0.408)

|

(0.178)

|

(0.141)

|

|

coffee

|

-1.677

|

-1.464

|

-2.774

|

2.215

|

6.952

|

5.684

|

4.821

|

|

(0.371)

|

(0.441)

|

(0.211)

|

(0.329)

|

(0.014)

|

(0.014)

|

(0.023)

|

|

juice

|

0.157

|

-1.986

|

-0.516

|

-1.538

|

1.077

|

2.895

|

2.394

|

|

(0.901)

|

(0.441)

|

(0.831)

|

(0.592)

|

(0.685)

|

(0.244)

|

(0.300)

|

|

wine

|

-0.528

|

-0.290

|

0.727

|

2.099

|

5.995

|

3.565

|

5.966

|

|

(0.770)

|

(0.869)

|

(0.709)

|

(0.329)

|

(0.005)

|

(0.080)

|

(0.005)

|

|

beer

|

3.788

|

3.975

|

-0.751

|

-1.279

|

-0.452

|

0.967

|

3.097

|

|

(0.047)

|

(0.052)

|

(0.718)

|

(0.521)

|

(0.812)

|

(0.568)

|

(0.080)

|

|

tobacco

|

-0.927

|

-1.655

|

-2.002

|

-2.913

|

-2.302

|

-1.474

|

-3.132

|

|

(0.765)

|

(0.545)

|

(0.502)

|

(0.357)

|

(0.446)

|

(0.592)

|

(0.347)

|

|

cloth

|

8.285

|

6.095

|

3.391

|

3.044

|

1.403

|

3.844

|

6.031

|

|

(0.005)

|

(0.028)

|

(0.239)

|

(0.291)

|

(0.610)

|

(0.192)

|

(0.028)

|

|

foot

|

7.504

|

3.174

|

1.657

|

1.126

|

2.055

|

2.582

|

7.947

|

|

(0.014)

|

(0.310)

|

(0.582)

|

(0.681)

|

(0.512)

|

(0.385)

|

(0.009)

|

|

cater

|

4.486

|

3.314

|

3.236

|

4.180

|

4.397

|

5.376

|

5.883

|

|

(0.005)

|

(0.014)

|

(0.014)

|

(0.009)

|

(0.005)

|

(0.005)

|

(0.005)

|

|

rest_caf

|

5.289

|

3.131

|

3.325

|

4.224

|

4.380

|

5.399

|

5.818

|

|

(0.005)

|

(0.014)

|

(0.014)

|

(0.005)

|

(0.005)

|

(0.005)

|

(0.005)

|

|

accomm

|

2.670

|

4.605

|

4.833

|

-0.029

|

6.069

|

13.572

|

8.008

|

|

(0.399)

|

(0.150)

|

(0.131)

|

(0.977)

|

(0.066)

|

(0.014)

|

(0.033)

|

Note: Table entries are gaps between actual and synthetic values of corresponding variables. Positive gaps imply that actual values are greater than the synthetic ones. P-values are given in parentheses. Bold entries are significant at the 5% level. Source: Author’s’calculation.

Source: Author’s calculation.

Note: y-o-y annual HICP inflation rates are depicted on the horizontal axis, and measures of market concentration are on the vertical axis. Both panels refer to the period of 2006-2021, conditioned by data availability. Source: Author’s calculation based on data from the Agency for the Protection of Market Competition.

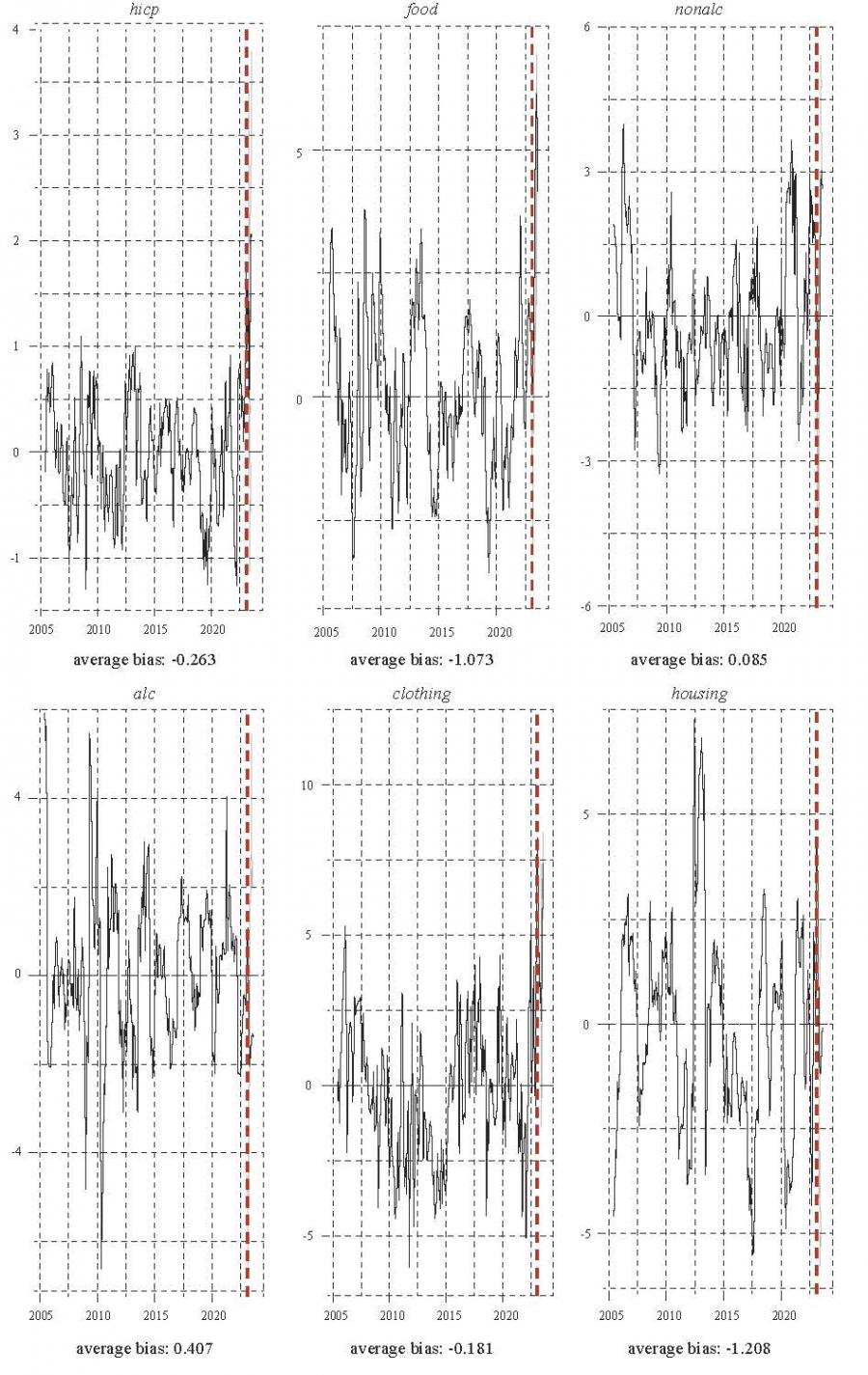

Note: Vertical axis captures the gaps between actual and synthetic values of corresponding variables (in percentage points). Positive gaps imply that actual values are greater than the synthetic ones, i.e. the currency changeover induced an inflation hike. Horizontal axis denotes time. Vertical dashed line denotes the date of currency changeover (January 2023). Grey shaded area after the currency changeover corresponds to the 95% confidence interval. Hicp and health models are estimated without auxiliary covariates. Food model is estimated with exp, gap, hicp, beer, fish, and milk as covariates. Nonalc, clothing, and housing models use exp, gap, and hicp as covariates. Furn and commun utilize fuel, exp, gap, and hicp; while recr, educ, rest, misc, and alc use fuel, exp, and gap as covariates. For the transport model we used exp and gap. Source: Author’s calculation.

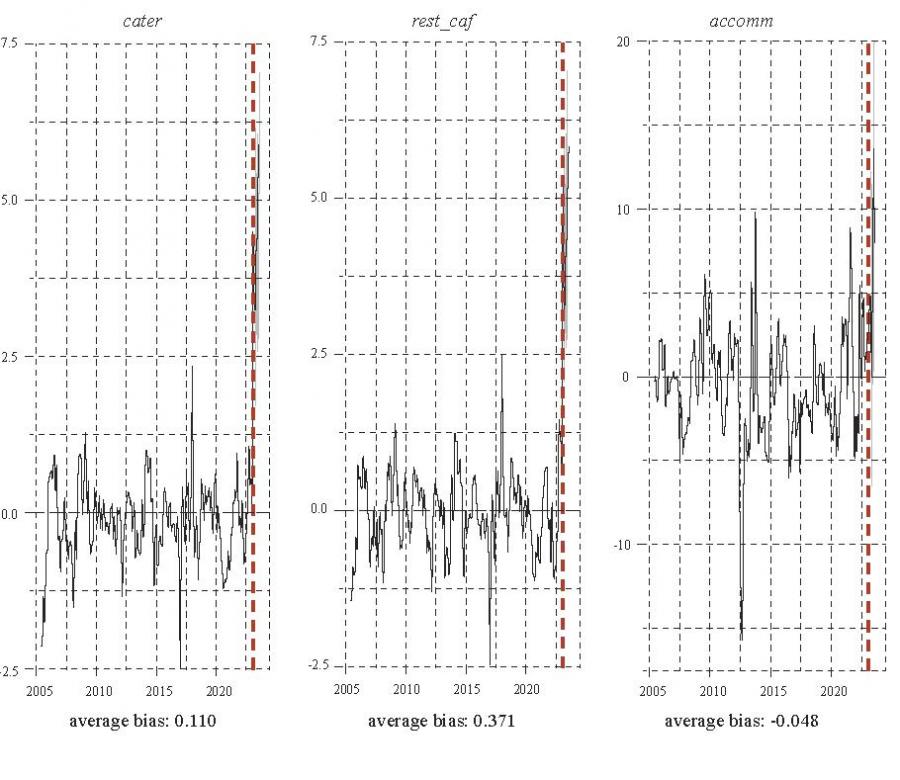

Note: Vertical axis captures the gaps between actual and synthetic values of corresponding variables (in percentage points). Positive gaps imply that actual values are greater than the synthetic ones, i.e. the currency changeover induced an inflation hike. Horizontal axis denotes time. Vertical dashed line denotes the date of currency changeover (January 2023). Grey shaded area after the currency changeover corresponds to the 95% confidence interval. Meat, fish, fruit, veg, foot, rest_solo, and accomm models are estimated without auxiliary covariates. Wine and cloth models use exp, gap, and hicp as covariates. Milk, juice, beer, tobacco, and cater utilize fuel, exp, gap, and hicp as covariates. For the coffee model we used exp and gap. Source: Author’s calculation.  Note: Vertical axis captures the gaps between actual and synthetic values of corresponding variables (in percentage points). Positive gaps imply that actual values are greater than the synthetic ones, i.e. the currency changeover induced an inflation hike. Horizontal axis denotes time. Vertical dashed line denotes the date of currency changeover (January 2023). Grey shaded area after the currency changeover corresponds to the 95% confidence interval. Meat, fish, fruit, veg, foot, rest_solo, and accomm models are estimated without auxiliary covariates. Wine and cloth models use exp, gap, and hicp as covariates. Milk, juice, beer, tobacco, and cater utilize fuel, exp, gap, and hicp as covariates. For the coffee model we used exp and gap. Source: Author’s calculation.

|

January

|

February

|

March

|

April

|

May

|

June

|

July

|

|

hicp

|

1.048

|

0.434

|

0.847

|

0.000

|

0.702

|

1.652

|

1.823

|

|

(0.089)

|

(0.174)

|

(0.352)

|

(0.826)

|

(0.568)

|

(0.023)

|

(0.014)

|

|

food

|

-0.522

|

-0.716

|

-0.232

|

1.993

|

3.079

|

3.914

|

2.744

|

|

(0.413)

|

(0.423)

|

(0.793)

|

(0.775)

|

(0.460)

|

(0.249)

|

(0.709)

|

|

nonalc

|

-0.507

|

-2.834

|

-2.613

|

-1.084

|

1.189

|

2.076

|

2.150

|

|

(0.765)

|

(0.197)

|

(0.202)

|

(0.634)

|

(0.427)

|

(0.122)

|

(0.113)

|

|

alc

|

1.436

|

0.294

|

-1.040

|

-0.518

|

-0.103

|

0.553

|

0.109

|

|

(0.432)

|

(0.822)

|

(0.305)

|

(0.441)

|

(0.577)

|

(0.690)

|

(0.690)

|

|

clothing

|

6.406

|

4.039

|

1.820

|

1.070

|

0.093

|

1.796

|

4.496

|

|

(0.005)

|

(0.023)

|

(0.263)

|

(0.305)

|

(0.498)

|

(0.192)

|

(0.005)

|

|

housing

|

0.391

|

-0.587

|

-1.036

|

-5.251

|

-5.417

|

-4.636

|

-3.567

|

|

(0.117)

|

(0.146)

|

(0.362)

|

(0.789)

|

(0.704)

|

(0.606)

|

(0.573)

|

|

furn

|

1.784

|

1.233

|

0.046

|

-1.423

|

0.143

|

0.882

|

1.607

|

|

(0.028)

|

(0.174)

|

(0.521)

|

(0.324)

|

(0.615)

|

(0.282)

|

(0.033)

|

|

health

|

2.026

|

1.316

|

0.594

|

0.278

|

1.040

|

2.156

|

2.361

|

|

(0.502)

|

(0.728)

|

(0.728)

|

(0.573)

|

(0.329)

|

(0.197)

|

(0.192)

|

|

transport

|

-1.009

|

-0.596

|

-0.339

|

-1.726

|

-1.209

|

0.655

|

1.183

|

|

(0.761)

|

(0.488)

|

(0.840)

|

(0.596)

|

(0.643)

|

(0.488)

|

(0.315)

|

|

commun

|

0.368

|

-0.245

|

0.629

|

1.562

|

0.928

|

-0.252

|

1.924

|

|

(0.516)

|

(0.526)

|

(0.667)

|

(0.887)

|

(0.991)

|

(0.526)

|

(0.380)

|

|

recr

|

0.700

|

-0.570

|

-2.035

|

-2.597

|

-2.989

|

-2.664

|

-0.735

|

|

(0.967)

|

(0.338)

|

(0.146)

|

(0.056)

|

(0.047)

|

(0.033)

|

(0.085)

|

|

educ

|

0.353

|

-24.000

|

0.186

|

0.011

|

-0.190

|

0.395

|

1.052

|

|

(0.981)

|

(0.873)

|

(0.808)

|

(0.704)

|

(0.624)

|

(0.761)

|

(0.958)

|

|

rest

|

3.341

|

2.776

|

2.863

|

3.088

|

4.725

|

7.510

|

5.811

|

|

(0.028)

|

(0.033)

|

(0.028)

|

(0.042)

|

(0.014)

|

(0.005)

|

(0.005)

|

|

misc

|

1.042

|

-0.355

|

-0.237

|

-0.418

|

-0.380

|

-0.318

|

0.014

|

|

(0.028)

|

(0.695)

|

(0.376)

|

(0.254)

|

(0.164)

|

(0.047)

|

(0.038)

|

Note: Table entries are gaps between actual and synthetic values of corresponding variables. Positive gaps imply that actual values are greater than the synthetic ones. P-values are given in parentheses. Bold entries are significant at the 5% level. Source: Author’s calculation.

|

January

|

February

|

March

|

April

|

May

|

June

|

July

|

|

hicp

|

2.130

|

1.686

|

1.660

|

0.683

|

1.086

|

2.256

|

2.379

|

|

(0.089)

|

(0.174)

|

(0.352)

|

(0.826)

|

(0.568)

|

(0.023)

|

(0.014)

|

|

food

|

1.317

|

1.103

|

1.866

|

2.682

|

3.121

|

3.462

|

1.893

|

|

(0.413)

|

(0.423)

|

(0.793)

|

(0.775)

|

(0.46)

|

(0.249)

|

(0.709)

|

|

nonalc

|

1.229

|

-1.142

|

2.255

|

-0.191

|

1.816

|

2.812

|

1.673

|

|

(0.765)

|

(0.197)

|

(0.202)

|

(0.634)

|

(0.427)

|

(0.122)

|

(0.113)

|

|

alc

|

0.253

|

-1.483

|

-3.047

|

-2.157

|

-2.005

|

-1.661

|

-1.648

|

|

(0.432)

|

(0.822)

|

(0.305)

|

(0.441)

|

(0.577)

|

(0.69)

|

(0.69)

|

|

clothing

|

6.200

|

4.550

|

0.759

|

1.946

|

0.806

|

3.057

|

6.611

|

|

(0.005)

|

(0.023)

|

(0.263)

|

(0.305)

|

(0.498)

|

(0.192)

|

(0.005)

|

|

housing

|

6.506

|

5.691

|

2.228

|

0.138

|

0.341

|

0.600

|

-0.541

|

|

(0.117)

|

(0.146)

|

(0.362)

|

(0.789)

|

(0.704)

|

(0.606)

|

(0.573)

|

|

furn

|

-3.466

|

-3.012

|

-3.861

|

-4.883

|

-3.060

|

-1.630

|

-0.530

|

|

(0.028)

|

(0.174)

|

(0.521)

|

(0.324)

|

(0.615)

|

(0.282)

|

(0.033)

|

|

health

|

1.483

|

0.804

|

1.072

|

1.593

|

0.537

|

3.578

|

3.578

|

|

(0.502)

|

(0.728)

|

(0.728)

|

(0.573)

|

(0.329)

|

(0.197)

|

(0.192)

|

|

transport

|

1.844

|

1.932

|

-0.292

|

-1.231

|

-1.572

|

0.027

|

1.589

|

|

(0.761)

|

(0.488)

|

(0.84)

|

(0.596)

|

(0.643)

|

(0.488)

|

(0.315)

|

|

commun

|

-2.172

|

-1.698

|

-0.956

|

-0.133

|

-0.398

|

-1.550

|

1.175

|

|

(0.516)

|

(0.526)

|

(0.667)

|

(0.887)

|

(0.991)

|

(0.526)

|

(0.38)

|

|

recr

|

-3.983

|

-5.523

|

-7.025

|

-7.190

|

-6.930

|

-6.538

|

-4.478

|

|

(0.967)

|

(0.338)

|

(0.146)

|

(0.056)

|

(0.047)

|

(0.033)

|

(0.085)

|

|

educ

|

6.853

|

6.611

|

6.372

|

5.934

|

5.669

|

5.962

|

6.387

|

|

(0.981)

|

(0.873)

|

(0.808)

|

(0.704)

|

(0.624)

|

(0.761)

|

(0.958)

|

|

rest

|

2.290

|

1.822

|

2.142

|

2.303

|

4.345

|

7.273

|

5.867

|

|

(0.028)

|

(0.033)

|

(0.028)

|

(0.042)

|

(0.014)

|

(0.005)

|

(0.005)

|

|

misc

|

-1.425

|

-2.578

|

-2.593

|

-2.417

|

-2.143

|

-1.117

|

-0.310

|

|

(0.028)

|

(0.695)

|

(0.376)

|

(0.254)

|

(0.164)

|

(0.047)

|

(0.038)

|

Note: Table entries are gaps between actual and synthetic values of corresponding variables. Positive gaps imply that actual values are greater than the synthetic ones. P-values are given in parentheses. Bold entries are significant at the 5% level. Source: Author’s calculation.

|

January

|

February

|

March

|

April

|

May

|

June

|

July

|

|

hicp

|

0.851

|

0.634

|

1.218

|

-0.527

|

-0.425

|

0.459

|

0.948

|

|

food

|

-2.481

|

-1.535

|

-0.590

|

0.548

|

1.102

|

1.167

|

0.343

|

|

nonalc

|

0.218

|

-1.857

|

-1.481

|

-0.360

|

1.590

|

1.664

|

2.326

|

|

alc

|

2.164

|

-0.168

|

-1.283

|

-1.377

|

0.283

|

1.941

|

1.028

|

|

clothing

|

7.069

|

4.907

|

3.035

|

4.122

|

2.867

|

3.736

|

7.044

|

|

housing

|

-6.476

|

-4.073

|

-3.834

|

-9.746

|

-11.619

|

-10.590

|

-8.810

|

|

furnish

|

4.001

|

2.770

|

2.731

|

0.847

|

1.593

|

1.723

|

2.154

|

|

health

|

-0.227

|

-0.686

|

-0.945

|

-1.839

|

-0.615

|

-0.386

|

-0.062

|

|

transport

|

-1.400

|

-1.975

|

-1.969

|

-2.962

|

-4.194

|

-2.425

|

-0.019

|

|

commun

|

-2.808

|

-3.525

|

-3.162

|

-1.544

|

-0.892

|

-1.316

|

0.756

|

|

recr

|

3.000

|

1.630

|

0.586

|

-1.504

|

-1.260

|

-1.679

|

-2.002

|

|

educ

|

-5.692

|

-6.128

|

-6.146

|

-5.223

|

-5.587

|

-5.525

|

-5.425

|

|

rest

|

4.238

|

3.424

|

2.932

|

0.292

|

3.928

|

6.773

|

4.584

|

|

misc

|

2.999

|

1.364

|

2.649

|

3.161

|

3.476

|

2.990

|

3.050

|

Note: Table entries are gaps between actual and synthetic values of corresponding variables. Positive gaps imply that actual values are greater than the synthetic ones. P-values are given in parentheses. Bold entries are significant at the 5% level. Source: Author’s calculation.

|

|

|

Abstract

This paper aims to shed some light on the issue of euro-induced inflation in the case of the Croatian euro changeover. Applying the synthetic control method, we were unable to find unambiguous and robust evidence of such an impact on the aggregate level. Focusing on a wide array of products and services, we found no impact of the euro on most price subcategories except those related to food, clothes and restaurant prices. The findings for the latter two categories seem particularly robust, surviving a battery of alternative specifications such as the generalized synthetic control and matrix completion method. Placebo tests reveal considerable ambiguity vis-à-vis the exact timing of the euro effect on prices, probably reflecting the fact that Croatia had been a highly euroized economy years before the de iure changeover.

Keywords: Euro changeover; Euro area; Croatia; inflation; synthetic control method; causal inference

JEL: C54, E31, E52

1 Introduction

On January 1, 2023, Croatia officially entered the eurozone, becoming its 20th member state. Although the entire process of Croatian euro integration has been extensively debated through the prism of Optimum Currency Area theory (Deskar-Škrbić, Kotarac and Kunovac,  2020; Brkić and Šabić, 2018) as well as of the expected reduction in the cost of borrowing (Kunovac and Pavić, 2018), and the stimulus for international trade (Bukovšak, Ćudina and Pavić, 2018), the attention of the general public has been directed mainly to the potential inflationary effects of the euro changeover (Pufnik, 2018). 2020; Brkić and Šabić, 2018) as well as of the expected reduction in the cost of borrowing (Kunovac and Pavić, 2018), and the stimulus for international trade (Bukovšak, Ćudina and Pavić, 2018), the attention of the general public has been directed mainly to the potential inflationary effects of the euro changeover (Pufnik, 2018).

Unlike all previous euro area enlargements, the changeover in Croatia was managed in conditions of extreme inflationary pressures. The circumstances were highly conditioned by the prolonged and substantial quantitative easing by the FED and ECB after the global financial crisis, the recent disruption of supply chains, as well as a considerable base effect due to abrupt and stringent lockdown policies around the globe.

This type of setting has been particularly problematic in a country such as Croatia. Its past experiences with hyperinflation episodes have heavily determined the general framework of monetary policy, using the nominal HRK/EUR exchange rate as an anchor to stabilize inflation expectations. On the other hand, in recent months the Harmonized Index of Consumer Prices (HICP) inflation rate has spiked. Croatian consumers reacted to this shock by gradually increasing their inflation expectations to a historical maximum. This pattern is clearly visible in figure 1.

Figure 1HICP inflation (year-on-year) rates and inflation expectations in Croatia DISPLAY Figure

Ever since the stabilization program in October 1993, Croatian monetary authorities have successfully maintained price stability, so the newcoming double-digit inflation rate seemed a black swan event for Croatian consumers. They rightly noticed the correlation between these inflationary pressures and the timing of the Croatian euro changeover. For example, European Commission ( 2022) reports that, among the EU countries outside the euro area, Croatia had the highest share of citizens who were concerned about abusive price setting and malpractice during the euro changeover (81% of respondents fully or partially agreed with that claim). Likewise, the same percentage of Croatian citizens firmly believed that the euro would increase prices. However, does this correlation between an inflation spike and the timing of the euro introduction indeed imply causality? Did the euro changeover itself trigger abusive price setting and rounding effects?

Under the conditions of the just described inflationary pressures, it seems extremely complex to conduct a proper signal extraction study and quantify the exact extent to which the Croatian inflation can be attributed to other tendencies, and how much it is a direct consequence of euro-related factors such as menu costs, rounding of prices to increase retail profits, etc.

This paper provides an initial attempt to examine if there are direct causal effects of the 2023 euro changeover on inflation in Croatia. In doing so, we examine a wide set of 14 price categories to enable a granular perspective on the issue. Our results reveal than the euro conversion did not have a robustly significant effect on aggregate inflation. The same holds for most inflation subcategories considered, except for food, clothing and restaurant charges, which significantly increased at the beginning of the conversion.

The remainder of this paper is organized as follows. Section 2 reviews the well-established reasons for the common (mis)perception that previous euro changeovers acted as inflation triggers. Section 3 discusses data specificities and the methodological framework, while Section 4 presents the empirical results of the study. Finally, section 5 provides some policy implications and directions for future research.

2 Euro changeover as a potential inflation trigger

On the first day of 2002, euro coins and banknotes were introduced in 12 European countries with a total population of more than 300 million people. This was the largest-ever monetary changeover operation in the world (Stenkula, 2004). As such, it attracted wide attention from the general public, the media, and the academia. Although the official inflation rate in 2003 remained fairly stable, consumers’ perceptions of inflation were significantly upward-biased (Antonides, 2008). In subsequent years, there was a proliferation of empirical studies on the topic. Four major factors were shown to have led the consumers to overestimate the importance of euro changeover in driving the general price increase (see e.g. Sturm et al. (2009) for an excellent literature review). This section will briefly pinpoint the main empirical findings.

2.1 Media effect

At the outset of the 2002 euro changeover, the media started to build up public expectations vis-à-vis the inflationary effects of euro introduction. The general atmosphere could be best described through the German lens, and their extremely frequent usage of the word “Teuro”, a portmanteau term composed of “teur” (expensive) and the word “euro” (Lamla and Lein, 2015). And indeed, formal econometric studies identified a significant media effect on the accuracy of inflation expectations. Lamla and Lein (2014) found that negatively toned media reports about inflation (describing inflation as “bad”) triggered an upward bias of consumers’ inflation expectations.In the context of such media reports, an expectation was formed in the general public that retailers would seize the opportunity to unduly increase prices in order to boost their profit margins. Experimental evidence speaks in favor of such a selffulfilling prophecy (Traut-Mattausch et al., 2004; Greitemeyer et al., 2005), finding inflation expectations to be a significant driver of inflation perceptions and of the noticed gap between actual and perceived inflation rate.

Dräger ( 2014) also found a marginally significant media effect, establishing a causal chain from negatively toned media articles to inflation expectations, and then to actual inflation developments. Lamla and Lein ( 2015) similarly detected that agents’ inflationary perceptions were highly dependent on the news about rising inflation. Lamla and Lein ( 2015) clearly establish the euro introduction as a structural break in the observed relationship. The media effect is negligible before 2002, and highly significant afterwards.

2.2 Frequently bought goods hypothesis

Although the general price increase was not significantly influenced by euro introduction, some effects were noticed for frequently bought goods (Lunn and Duffy, 2015). Del Giovane and Sabbatini (2006) defined frequently bought goods as those purchased at least once a month: food, tobacco, everyday household products, newspapers, fuels, and services such as local transport, postal and banking services, restaurants and coffee shops, recreational and cultural services. The prices of these goods did indeed spike in 2002 (Del Giovane and Sabbatini, 2006; Lunn and Duffy, 2015). Some of these inflationary pressures were caused by menu charges, while in other cases retailers were seen to have rounded off their prices upwards. As a consequence, agents seem to have attached too large a weight to these categories of goods, producing largely and systematically biased perceptions of actual inflation rates.

This pattern is possibly a result of the availability heuristic (Kahneman and Tversky, 1979), meaning that agents systematically overweight the price changes of low-cost goods purchased on a frequent basis, often via out-of-pocket purchases (Del Giovane and Sabbatini, 2006; Dziuda and Mastrobuoni, 2009).

2.3 Methodological issues concerning inflation measurement

In euro area countries, inflation is measured via the Harmonised Index of Consumer Prices (HICP). A Laspeyres-type index, HICP is calculated by attaching consumption weights to individual item categories. However, these weights are updated rather infrequently, i.e. every five years (Antonides, 2008). Therefore, it comes as no particular surprise that the price indices of only a few item subcategories significantly explain the general consumers’ inflation perceptions. Nota bene, some of the most prominent frequently bought goods (such as food and drinks) are not among them.

2.4 Comparison effects

A study by Fessel GfK (2004) revealed that even two years after the introduction of euro, as many as 74% of Austrian consumers still mentally converted the euro prices to Austrian schillings. By fixing the reference prices to two years before, they inevitably neglected the secular tendency of price increases, and consequentially generated upwardly biased inflation perceptions.

Similar cognitive biases were noticed in the relationship between the consumers’ perceived inflation rate and the complexity of the conversion rates of their domestic currency vs. the euro. For example, the euro conversion rate of the German mark was 1.95583. Ehrmann ( 2006) suggests that German consumers used a simple rule of thumb when assessing euro prices after the conversion; they multiplied the displayed euro prices by two. This alone, ceteris paribus, induced an overestimation of 2.26%. More complex conversion rates, such as Austrian, Dutch, French, and Italian, triggered their consumers to err much more in their price comparisons.

After explaining the main driving forces of the euro-induced inflation perception gap, the following section will introduce our methodological approach to quantifying the euro effect on Croatian inflation.

3 Methodology and data

Previous studies of the relationship between euro changeover and inflation can mostly be divided into two methodological strands. The first one focuses on time series analysis such as Granger causality and cointegration tests on macroeconomic data (Antonides, 2008; Del Giovane and Sabbatini, 2009; Dziuda and Mastrobuoni, 2009; Dräger, 2014; Lamla and Lein, 2015). The other one is more concerned with micro experiments (Traut-Mattausch et al., 2004; Greitemeyer et al., 2005). Both approaches are perfectly plausible and add to our understanding of the phenomenon at hand. We aim to reconcile the two by offering a setup of a quasinatural experiment using macroeconomic data. In assessing the impact of a policy intervention or an exogeneous shock (such as a currency changeover) on social and economic outcomes, we follow the rationale of biomedical experiments to inspect whether the observed relationship between euro changeover and inflationary pressures can be attributed to pure correlation or causality. In this strand of research, after identifying the treatment sample, researchers should pay particular attention to the choice of proper control (comparison) sample. Ideally, the control units should be exactly the same as the treatment entities vis-à-vis a set of fundamentally important characteristics, but should not be exposed to the treatment of interest. In social sciences, units of analysis are often regions or countries, so appropriate comparison units frequently do not exist (George and Bennet, 2005; Abadie, Diamond and Hainmueller, 2015). In this particular case, Croatia stands out as an exemplar of sub-optimal efficiency of economic transition, a peculiar economic structure dominated by tourism-related activities, and étatism (Stojčić, 2012). Having that in mind, it seems extremely difficult to find proper comparison unit(s) for Croatia. To circumvent this kind of problem, Abadie and Gardeazabal (2003) and Abadie, Diamond and Hainmueller (2010; 2015) had introduced the Synthetic Control Method (SCM), a data-driven procedure aimed at constructing a counterfactual (synthetic control) as a weighted combination of potential comparison entities. Such synthetic control is conceptualized to exhibit the underlying characteristics of the treatment entity of interest better than any other single comparison unit. Within a very short period, SCM became an indispensable tool in many sciences, such as economics (Abadie, 2021; Campos, Coricelli and Moretti, 2019), health studies (Bouttell et al., 2018), sociology (Vagni and Breen, 2021), etc.

3.1 Synthetic control method

Being unable to observe a counterfactual Croatia that did not go through the euro changeover, we use the relevant macroeconomic data from all other EU economies. As the remaining 26 economies share the EU single market with Croatia and have a harmonized set of institutional rule and policy frameworks, they seem potentially plausible candidates for this purpose. Suppose that we observe a panel dataset consisting of J + 1 countries (j = 1, 2,..., J + 1), where the first country (j = 1) is the treated one. In our case, we are interested in the effect of an intervention (euro changeover) on Croatian inflation. Therefore, Croatia is the treated unit. The remaining EU economies (j = 2, 3, ..., 27) are not affected by the treatment, and as such comprise the donor pool, i.e. they are potential candidates for comparison. We observe a balanced panel, i.e. all units are observed across periods t = 1, 2,..., T. To be exact, our dataset spans from 2005M05 to 2023M07 (conditioned by data availability). As the intervention (euro changeover) occurred in January 2023, the time span consists of T0 = 212 monthly pre-treatment periods and T1 = 7 post-treatment monthly periods (T = T0 + T1 = 219).

The goal is to construct a synthetic control that resembles Croatia much more than any individual EU economy in terms of a selected set of variables. As the dependent (target) variables in the model, we use aggregate HICP inflation (hicp hereinafter), and its 13 subcomponents based on the European Classification of Individual Consumption according to Purpose (ECOICOP): food inflation (food hereinafter), inflation of non-acoholic beverages (nonalc), alcoholic beverages, tobacco and narcotics (alc), clothing and footwear (clothing), housing, water, electricity, gas and other fuels (housing), household equipment and routine household maintenance (furnish), health (health), transport (transport), communication (commun), recreation and culture (recr), education (educ), restaurants and hotels (rest), and miscellaneous goods and services (misc). We aim to estimate a separate synthetic control model for each of these 14 variables, constructing 14 different counterfactuals.

We use the following set of inflation covariates: output gap obtained by applying the Hodrick-Prescott filter on the industrial production index (2015=100) ( gap hereinafter), inflation expectations ( exp), and the HICP subcomponent related to the prices of electricity, gas, and other fuels ( fuel hereinafter). The first two variables are commonly found in various sorts of New-Keynesian Phillips curve specifications (e.g. Basistha and Nelson, 2007; Jašová, Moessner and Takáts, 2020; Panovska and Ramamurthy, 2022), while the latter variable proxies energy prices that are also widely accepted as an inflation driver. 1 The target inflation variables, along with energy prices, are expressed as year-on-year ( y-o-y) growth rates. For each of the 14 inflation categories we use gap, exp, and fuel as auxiliary covariates to construct a proper counterfactual.

Inflation expectations are derived from the EU Consumer Survey, in the form of a response balance (weighted difference between the shares of positive and negative answers) on the following survey question (see European Commission ( 2023) for details).

By comparison with the past 12 months, how do you expect that consumer prices will develop in the next 12 months? They will: a) increase more rapidly, b) increase at the same rate, c) increase at a slower rate, d) stay about the same, e) fall, f) don’t know.

Industrial production indices and all inflation data are obtained from Eurostat, while inflation expectations are made publicly available by the European Commission.

The stated predictors of inflation are conceptualized through a k × 1 vector of preintervention values for Croatia (denoted X1), and we introduce X0 as a k × J matrix comprising the same variable observations for other EU economies. Synthetic control is obtained as a weighted average of comparison units (Abadie and Gardeazabal, 2003; Abadie, Diamond and Hainmueller, 2010; 2015). The vector of weights W = (w2 ,w3 ... wJ+1)' comprises nonnegative elements (0 ≤ wj ≤1) for j = 2, 3,..., J + 1 and the weights sum up to 1 (w2 + w3 + ... + wJ+1 = 1). Optimal weights W* are determined as the value of W that minimizes the discrepancy between the pre-changeover characteristics of Croatia and its synthetic control: | (1) |

where X1m is the value of the m-th variable for Croatia, X0m is a 1 × J vector of m-th variable’s values for the comparison units, and vm is the non-negative weight (relative importance) attached to the m-th variable. The latter should take on large values for variables that closely correlate with the outcome variable for the treated entity.

Finally, estimating the causal effect of an intervention  comes down to comparing the post-changeover inflation in Croatia and the post-changeover inflation of its synthetic control:  | (2) |

where Yjt is the outcome of entity j at time t, Y1 is a T1 × 1 vector of post intervention outcomes for the treated entity, and  is the SCM-estimated (synthetic) outcome without the treatment.

Although SCM is a powerful and widely applied tool for policy evaluations, it has its limitations. Most importantly, it does not allow formal econometric testing of the significance of the causal effect. To counteract that, we also use a relatively novel conformal inference method introduced by Ben-Michael, Feller and Rothstein ( 2021): Augmented Synthetic Control Method (ASCM).

In practice, it is often a very hard task to construct a proper counterfactual using SCM. ASCM is specifically designed to correct for the bias of SCM and improve the quality of the counterfactual. Ben-Michael, Feller and Rothstein ( 2021) conceptualized the ASCM framework as follows:  | (3) |

where  is the ASCM synthetic outcome (in this case counterfactual Croatian inflation rate, without the euro changeover), Xj is a vector or pre-changeover outcomes for the j-th EU economy, and X1 is a vector of pre-changeover outcomes of Croatia. This kind of notation is adopted to emphasize that pre-treatment outcomes are used as input (independent variables) in the model. In the same manner, Z1 and Zj are vectors of corresponding auxiliary covariates, while  and  are coefficients obtained through a ridge regression of the control post-treatment outcomes on centered pre-treatment outcomes, with a tuning parameter that penalizes the distance between ASCM weights and the conventional SCM weights. The idea of this estimator is to increase the pre-treatment fit of the classic SCM model (decrease its bias), while minimizing extrapolation from the convex hull (see BenMichael, Feller and Rothstein ( 2021) for details). It is important to highlight that ASCM weights wj*(as opposed to the standard SCM model (Abadie and Gardeazabal, 2003; Abadie, Diamond and Hainmueller, 2010; 2015)) are allowed to take negative values. Going back to our choice of the donor pool (26 remaining EU economies), it would be expected that ASCM attaches very small (or even negative) weights to core EU economies (e.g. Austria, Germany, France, etc.) whose economic sizes and structures do not positively and significantly correlate with the Croatian economy. Instead of handpicking the EU economies with economic structures similar to the Croatian (e.g. with a considerable share of tourism in GDP), we opted for letting the data speak for itself. Should those economies really comprise the optimal donor pool, ASCM would assign them the largest weights.

All estimations are performed in R Studio via packages Synth, augsynth, and MSCMT.

The reliability of ASCM results critically depends on the accuracy of its pre-treatment fit. Our estimates of a post-changeover euro effect on inflation are only as valid as our pre-changover estimate of synthetic counterfactual is similar to the actual Croatian inflation rate. For that purpose, we used the following approach. For the ASCM model with hicp as the dependent variable, we used fuel, exp, and gap as the potential pool of auxiliary covariates. We chose the combination that minimized the average pre-treatment bias (difference between actual and synthetic outcome). Average bias is a standard part of the estimation procedure in augsynth R package. For the remaining 13 inflation categories (food, nonalc, alc, clothing, housing, furnish, health, transport, commun, recr, educ, rest, and misc), we add hicp to the pool of auxiliary covariates, and again choose the combination that minimizes the average pre-treatment bias.

To inspect if the obtained ASCM results are robust enough, reaserchers usually resort to conducting placebo specifications across time and entities. A placebo test implies conducting the exact same analysis for a time period or cross-section unit where the expected effect of the intervention is equal to zero (non-rejection of the null hypothesis). In our case, a placebo test implies testing the effect of euro changeover in a country that has not actually undergone it, or testing its effect in a time period that cannot be related to the actual changeover. Observational studies often tend to under-report the results of placebo tests (so-called i nverse p-hacking) to corroborate their initial results (Dreber, Johannesson and Yifan, 2023). To address this issue properly, we conduct a series of placebo tests, extensively report their results and discuss them in detail.

3.2 Caveats

The end-point of the observed time span is conditioned by the latest available data at the moment of writing. One might question the appropriateness of SCM analysis for a dataset with T1 = 7 post-intervention periods. However, SCM is specifically designed to assess a smaller dataset (Gilchrist et al., 2023) compared to e.g. financial econometrics or machine learning techniques. Having that in mind, previous empirical SCM studies have routinely been conducted on smaller post-intervention sample sizes (e.g. Sills et al., 2015; Tkalec, Žilić and Recher, 2017; Gharehgozli, 2017). Likewise, we postulate that our SCM framework is also economically relevant because empirical studies of the 2002 euro changeover found that the impact of this monetary conversion on inflation (if any) was short-lived (Sturm et al., 2009; Pufnik, 2018).

Additionally, let us briefly discuss the utilization of y-o-y growth rates of all price variables. This step seemed very important in our empirical setting because it takes adequate account of any seasonal effects and working day adjustments, and it conceptually matches inflation expectations derived from consumer surveys (expected price development during the 12 months horizon). Finally, using growth rates of macroeconomic variables in SCM applications is rather standard (Opatrný, 2017; Boiciuc and Orțan, 2020).

4 Empirical results

We start by applying the ASCM framework to synthetize the counterfactual time series of Croatian inflation rate and test its (dis)similarity with the actual inflation rate after the euro changeover.Our baseline ASCM estimates are given in table 1 and figure A1 in the appendix. Our results seem to corroborate the finding from previous euro area enlargements that euro changeovers were specifically related to price increases of food (Brachinger, 2008; and Lunn and Duffy, 2015), clothing (Cavallo, Neiman and Rigobon, 2015; Rõõm and Urke, 2014), and restaurant services (Sturm et al., 2009; Pufnik, 2018). It should be noted that, aiming to shed additional light on these inflation categories and reduce bias as much as possible, we considered an additional set of auxiliary covariates. Inflation in food was (in addition to fuel, exp, gap, and hicp) modelled with lower-level inflation categories related to: meat ( meat), fish and seafood ( fish), milk, cheese and eggs ( milk), fruit ( fruit), vegetables ( veg), coffee, tea and cocoa ( coffee), wine ( wine), beer ( beer), tobacco ( tobacco). Clothing category is further augmented with its corresponding subcategories of inflation: clothing ( cloth) and footwear ( foot), while rest is modelled with the addition of catering services ( cater), restaurants, cafés and the like ( rest_caf), and accommodation services (a ccomm). Detailed specifications of all examined models are given in the note below figure A1.

Table 1ASCM baseline estimations (January to July 2023) DISPLAY Table

A glance at the results suggests that there is not much evidence of a euro effect on inflation. Aggregate HICP inflation reacted mildly in January, and then an intensification of the euro effect is again observed in June and July. Most of the considered subcategories did not react significantly. The only substantial and robust effect is observed for food, clothing, and rest. The reaction of food prices was not instantaneous, but characterized by a delay. It became significant only during the last three months of the sample, with a magnitude of 3.615 to 4.889%. As far as clothing prices are concerned, their difference between the actual and counterfactual Croatia is 8.225% in January, and then 5.901% in the following month. Restaurant prices seem to be roughly 4-9% higher due to the euro changeover, and the euro effect was much more persistent throughout the post-intervention period than was the case with other price categories.

The observed euro effect mostly intensifies in June and July (particularly for the rest category), which is probably related to the general concept of tourism-led inflation (Tkalec and Vizek, 2016).

ASCM chooses donor weights that optimize pre-treatment fit. For brevity, we do not report the full set of results, but provide only the average obtained country weights in figure 2. The highest weights are obtained for Spain (0.136), Slovakia (0.131), Malta (0.117), Portugal (0.0979), and Slovenia (0.090). These are either Mediterranean countries with comparable tourism-oriented economies, or Central and Eastern European post-transition countries that had similar historical, politico-economic and institutional trajectories as Croatia.

Figure 2Average ASCM country weights DISPLAY Figure

However, it remains to be seen whether this phenomenon is causally related or purely fortuitous. In that context, the literature suggests conducting placebo tests across entities and across time. For example, should similar results be observed for food, clothing and rest categories of other countries (that have not adopted the euro in January 2023), this would undermine the plausibility of the observed euroinduced inflation effect.

Table 2ASCM placebo specifications across countries (January to July 2023) DISPLAY Table