|

|

|

Abstract

Since increases in public pensions are generally related to prices or wages or combinations of them, the impact of inflation on the real value of benefits can often be neglected, especially in the case of indexation to prices. With high and accelerating/ decelerating inflation like that currently prevailing in Hungary, however, this is not the case. (i) With fast inflation of basic necessities, the proportional indexation of benefits in progress devalues the lowest benefits, which have to pay for above-the-average consumption share of these goods. (ii) Annual “lumpy” increases of these benefits entail too high an intra-year drop in the real value of benefits. (iii) With accelerating inflation, the declining real value of delayed initial benefits may incentivise immediate retirement. (iv) With unindexed parameter values (like progressivity bending points), the initial benefits’ structure unintentionally changes.

Keywords: inflation; public pensions; indexation; progressivity of initial benefits; delayed retirement

JEL: E31, H55

1 Introduction

For a long time, public pensions in progress have been indexed to prices or wages or a combination of the two (Whitehouse,  2009). At the moderate inflation characteristic of the last two decades, politicians and pensioners have been inclined to neglect the issues of pension indexation, especially in the case of indexation to prices. This complacency has been shattered by the recent worldwide surge in inflation. In December of 2022, the 12-month inflation rate reached 11% in EU27; exceeded 24% in Hungary and 16% in Czechia. The annual inflation was more modest, being 14% in Hungary and 15% in Czechia. 2009). At the moderate inflation characteristic of the last two decades, politicians and pensioners have been inclined to neglect the issues of pension indexation, especially in the case of indexation to prices. This complacency has been shattered by the recent worldwide surge in inflation. In December of 2022, the 12-month inflation rate reached 11% in EU27; exceeded 24% in Hungary and 16% in Czechia. The annual inflation was more modest, being 14% in Hungary and 15% in Czechia.

It is worth quoting some key observations of OECD ( 2022) on how inflation challenges pensions. (a) “[D]ue to falling real wages, price indexation has become a more favourable protection for pensioners than wage indexation, while being more costly than initially anticipated.” (b) “[A]lternatives for full price adjustment for all include a combination of: a flat rate payment; full adjustment up to a threshold and partial adjustment, potentially up to a cap beyond which no adjustment would apply.”

From now on, we shall confine our attention to Hungary, mostly to recent developments. Just before the national elections in April 2022, the Hungarian government introduced several significant budgetary measures to increase its popularity. One of them was the accelerated introduction of the 13th month pension. The cost of the acceleration and the total impact amounted to about 0.3 and 0.6% of GDP, respectively. The cost of this and other measures approached 3% of GDP, explaining a large part of the extra inflation.

Hungary has a public pension system in which initial benefits are almost proportional to lifetime contributions but 10 and 20% of the pension base, lying in the higher brackets, are progressively deducted. (Another progressive factor is that the marginal accrual rate is U-shaped, almost halving the impact of the first 20 years of contribution in the second 20 years: 27% < 53%.) Benefits in progress are indexed to prices, meaning that in January of the current year, all benefits are raised by the annual inflation rate forecasted by the government. If the forecast is below the actual inflation rate, then at the end of the year, the difference is made up; if the forecast is above the actual rate, then pensioners retain the surplus.

Between 2013 and 2021 the reported rise of nationwide real wages was very fast, partially fuelled by the forced reduction of contribution rates. On the one hand, through indexation of initial benefits, this raised the real value of these benefits quite substantially. On the other hand, the relative value of older benefits dropped, resulting in a declining ratio of benefits to net earnings from 67 to 50%. Though the genuine real wage rise was much lower (say 30 rather than 50%), the initial benefits rose by this overestimated value and the relative loss of benefits to wages looked much greater than it was in reality. (For a text in Hungarian, see Oblath and Simonovits, 2023.)

Turning to the actual subject of our study, the unexpected acceleration of inflation in 2022 made the initial 5% increase of benefits in progress unsatisfactory, and it was completed by 3.9 and 4.5% in July and in November, respectively. Using a multiplicative rule, this has led to a total increase of 1.05 × 1.039 × 1.045 = 1.140, i.e., +14%, slightly lower than the final index.

Though the benefit increases are generally proportional to the last benefits, there are strong arguments for nonproportional raises for pensioners with low benefits when the prices of basics like food and household energy increase much faster than the average, while their shares are higher in such baskets than on average. For example, in December 2022, in Hungary the price levels of certain groups of goods were much higher than they were 12 months previously – food: 45%, energy: 62%, heating gas: 121%. Note that the shares of food and of energy expenditures of the lowest quantile were 33 and 14 rather than the corresponding averages of 26 and 12%, respectively.

The real values of the initial benefits have also been affected by the accelerated inflation. On the one hand, the acceleration reduced or even eliminated the gain from delayed retirement. On the other hand, through nominally fixed progressivity bending points, inflation diminished high benefits relative to expectations or past benefits.

These changes justify the discussion of the following pension measures: (i) In addition to introducing special heating subsidies, low benefits deserve temporary special increases. (ii) Smoothing out the path of the real values of pensions in progress within a given year by intra-year rises if necessary. (iii) Dampening the impact of accelerating inflation on delayed retirement with proper indexation. (iv) Making the progressivity of higher benefits inflation-free by indexing the bending points of the progressive initial benefit formula. Adding up the impacts of these apparently minor measures may imply important changes.

Considering the literature, we start with the classic paper of Fischer ( 1982) on the pros and cons of indexation in general. We single out few earlier discussions of various issues of pension indexation: Simonovits ( 2003, Chapter 6) emphasized the obvious problem of backward- or forward-looking indexation of benefits in progress and the delayed valorisation of initial benefits during the transition period in Hungary. Barr and Diamond ( 2008, Chapter 5) clearly differentiated between indexing initial benefits and benefits in progress; and analysed the so-called over-indexation of US Social Security benefits and of the UK state pension. Lovell ( 2009) very thoroughly examined various pitfalls in the indexation of US Social Security benefits. Though payday lending, i.e., very expensive short-term loans (Stegman, 2007), may seem unrelated to pensions, it can still be an option for pensioners who cannot cope with the fast-decreasing real value of monthly benefits within a year. Domonkos and Simonovits ( 2017) surveyed pension design problems of post-socialist countries. Simonovits ( 2020) studied the role of indexation in the relative devaluation of older pensions with respect to newer pensions and current wages. Checherita-Westphal ( 2022) is the latest analysis of the indexation of public pensions (and of public wages) in the current period of higher inflation.

The structure of the remaining part of the paper is as follows. Section 2 justifies special increases of low benefits. Section 3 compares actual annual and proposed monthly indexation. Section 4 evaluates the impact of accelerating inflation on the yield of delayed retirement. Section 5 studies the impact of wage and price inflation on the progressivity of a nominally framed initial benefit. Section 6 concludes. An appendix supplies the details of the Hungarian pension system skipped in the main text.

2 Special increases of low benefits

For a long time, inflation rates have been moderate and quite uniform among the various categories. Since 2021, however, not only has the general inflation accelerated but food and energy prices have risen especially fast. Since these categories have a higher share in the consumption of households of lower incomes, these households deserve extra income support. Traditionally, low-income pensioners enjoy greater support than the average low-income population, therefore any pension study must tackle the issue. Table 1 displays the aforementioned tendency among the ten deciles for food and income and five quantiles for household energy in Hungary, in 2020. Note that as we move from the poorest to the richest decile and quantile, the shares of food and energy expenditures decline from 33 to 21% and from 14 to 9%, respectively

Table 1Shares of expenditure on food and household energy, Hungary, 2020 (in %) DISPLAY Table

The explosion of food prices is menacing but it appears to be simpler to address than that of household energy prices. The government fixed the latter between 2012 and July 2022, but since last August, only the part of consumption below a cap has been supported, separately for energy and heating gas. Any unit of consumption above the corresponding cap costs twice as much for electricity and 7.6 times as much for heating gas. As a result, in September 2022, the average electricity and heating gas prices grew by 29 and 121%, respectively. As a first approximation, we assume uniform distribution below and above the cap, then the average electricity and heating gas consumption grew by 14 and 16%, respectively. (In fact, 1 + 0.14 × 2 = 1.28 and 1 + 0.16 × 7.6 = 2.16, respectively.) It is evident that within every decile, a significant share of households is unaffected, while the remaining shares are heavily affected. It is a tricky question how to treat this problem. Perhaps heating should be taken out from the pensioners’ price index and an additional heating support should be introduced but this needs a special study.

Claeys et al. ( 2023) report the impact of income-dependent consumption weights on the inflation of the lowest and the highest quantile’s inflation in the EU in general, and Hungary in particular. Earlier the impact was quite small but from September 2022, the gap opened wide.

Figure 1Inflation rates for top and bottom quintiles, Hungary (in %, year-on-year) DISPLAY Figure

From now on we shall neglect inflation inequality.

3 Indexation of benefits in progress

The indexation of benefits in progress is probably the most important single measure of the pension policy. And it becomes an especially hot topic when inflation is as high as it is in Hungary now. To understand the impact of accelerating inflation we must go beyond annual inflation. We shall show that under once-a-year increases of benefits, high inflation causes huge temporary losses (and gains) to pensioners. But we must make it clear that if high inflation is only a transitory phenomenon, and the indexation rules are sensible, then these losses (and gains) are only temporary; and in the long-run, they are netted out.

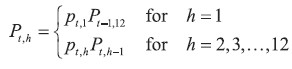

We shall first describe the various inflationary indices and then discuss the benefit increases. We start from the monthly price index pt,h, where t and h stand for the year and the month, respectively. We shall need the price level Pt,h, cumulating the monthly price indices from an arbitrary period, say year 0 and month 12, starting with P0,12 = 1, it is

We shall start from year t = 2021 and display the actual Hungarian data of 2021- 2022 in table 2 and supplement them by a forecast made by Éva Palócz (Kopint) for year 2023 (personal communication).

Table 2Annual and monthly price indices (actual and forecast) DISPLAY Table

Columns 1 and 2 stand for the year and the month, respectively. Column 3 shows the monthly change in the price level. For example, 1.009 in row 2021:1 shows that the price level rose by 0.9% from 2020:12 to 2021:1.

Column 4 displays the accumulated price level Pt,h, P2020,12 = 1. For example, 1.442 in the last row shows that the price level is expected to be 44.2% higher in December 2023 than it was in December 2020.

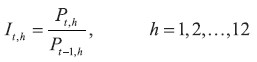

Next we introduce the year-on-year inflation index of 12 months:  Entries of column 5 show these numbers. By the forecast, this indicator will drop from 1.245 (2022:12) to 1.077 (2023:12).

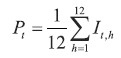

Finally, the arithmetic average of 12 monthly year-on-year indices of a year is called the inflation index of year t:

This index can be rationalized as follows: if in every month of years t−1 and t, the consumer buys quantity y, she spends Pt times more in year t than in year t−1. Column 6 displays this index. For example, 1.15 stands for the price index of 2022 to 2021. This plays a prominent role in macroeconomics in general and in pension economics.

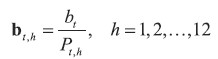

Turning from inflation to benefits, we repeat: the main problem with the “lumpy” annual increase is that it only preserves the purchasing power of the benefits spread over the whole year but it tolerates steep declines within the year. Assuming that the annual forecast is perfect and no intra-year compensation is needed, the uniform monthly nominal value of the benefit in year t can be denoted by bt. By definition,

bt = bt-1Pt t = 1, 2 b0 = P0

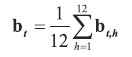

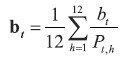

The next question is: how to define the real values of the monthly payments? One possibility of defining them is to discount the nominal values to the last month of year 0:  | (1) |

We shall need the annual average of these benefits in real terms:

| (2) |

Inserting (1) into (2) yields  | |

Typically the price level rises every month, therefore the real value of the monthly benefits is decreasing except for January:

bt,1 > bt,2 > ··· > bt,11 > bt,12.

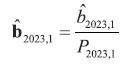

We shall argue that in the case of high inflation, to smooth out this drop, it is worth having a more frequent, even monthly increase, also preserving the real value of the monthly benefits from 2023:

where the real value of the reformed January benefit (bold) is the ratio of the nominal monthly benefit and the corresponding price level:  | |

Of course, the extraordinary increase in January should be determined to preserve the real value of the annual benefits. Having the equality of the past and future annual benefits in real terms, this yields

With rearrangement,

If this rule implies a nominal drop in benefits, skip it and credit it against future nominal raises. For example, if a 2% nominal drop is implied, then fix the nominal values of the benefits until inflation eats it up.

Like table 2, table 3 also has a double year and month index. Columns 3 and 4 display the traditional sequence of fixed nominal benefits and the resulting decreasing real benefits, respectively. Note the great drop of the benefit’s real value in December from January 2022: 0.901 < 1.105. (It was a mixed blessing that due to the rough underestimation of the 2022 inflation, the actual loss was smaller.) Confining our attention to the year 2023, columns 5 and 6 present the proposed monthly rise in nominal benefits and the resulting constant real benefits, respectively.

Table 3Annual vs. monthly benefit raise, 2021-2023: counterfactual exact forecast DISPLAY Table

4 Delay of retirement

When the annual inflation rates were moderate and stable, the initial pension benefits followed the corresponding reported average real wage dynamics with a one-year lag with a good approximation (Simonovits, 2020). Between 2015 and 2020, inflation was moderate and reported average real wages rose by 7-10% per year, therefore, the initial benefits grew similarly (see table 5). Though the Hungarian Statistical Office significantly overestimated real wage growth because it used a distorted sample of fulltime-employed workers, the real growth of initial benefits was genuine. Because the individual benefits in progress have stagnated in real terms, the tension between newer and older beneficiaries has become stronger. This changed in 2021/2022, when the real wage dynamics slowed down and the inflation rate accelerated. (It is worth citing Fischer (1982:169): “variability of inflation matters because uncertainty about the inflation rate creates as serious economic difficulties as those caused by high inflation itself”.)

To model the problem, we consider an extreme case: a worker considers retiring either on the last day of year t or on the first day of year t+1. Denoting the growth index of the average nominal wage by Gt, and the inflationary index of the next year by Pt+1 (apart from complications with progressivity, discussed in the next section), the one-day delay multiplies the initial benefit by Gt (extra year of valorisation) and divides it by Pt+1 (lack of indexation as benefit in progress in the new year). Therefore, the simplest indicator of the delay’s yield is  |

|

If Gt > Pt+1, then the delay is advantageous; if Gt < Pt+1, then the delay is disadvantageous; if Gt = Pt+1, then the delay is neutral. Of course, most workers retire earlier than December 31 or later than January 1, but for our discussion, the analysis of this decision is sufficient. (In Hungary, since 2011/2012, early retirement has been abolished except for females with 40 years of entitlements, and very few employees work beyond the normal retirement age, therefore the actuarial reduction/addition can be safely ignored.)

Note that to forecast the annual inflation index can be difficult not only for the employees but also for the government. For example, as mentioned above, the subsequent expected annual rate has been increasing in 2022 (from 5 to 14%), eliminating the expected advantage of the one-day delay. Table 4 presents the calculation for three distinct months. The actual inflation rate was around 14%, turning the expected gain of 1.087/1.05 − 1 = +0.035 into an actual loss of 1.087/1.14 − 1 = −0.046.

Table 4Three forecasts DISPLAY Table Note, however, that in some of my earlier studies (e.g. Simonovits, 2020), I have been using a simpler estimator, naively replacing future inflation with past inflation. If Pt+1 is estimated by Pt, then the corresponding yield collapses to the annual real wage index: Table 5The estimations of the impact of delaying retirement, 2010-2022 DISPLAY Table Table 5 shows the difference between the “rational” and naive estimations. According to the rational forecast, delay was advantageous even in 2012, when the naive forecast made delay disadvantageous. In 2021, it was the opposite. (In fact, here we neglect that overestimation of inflation in the period 2013-2016, mentioned above.)

5 Progressivity of initial benefits under inflation

Fischer 1982: 170) underlined the cost of government’s “failure to adjust the tax laws for inflation”. This also applies to the real impact of inflation on the progressivity of Hungarian initial benefits. Let t = 2012, 2013, ... stand for the index of year, wt and wt* for the nominal average (reference) wage and bending point in year t, respectively. For a reference wage below or at the bending point, the initial benefit is proportional to the reference wage, β1 > 0 being the accrual rate. For a reference wage above the bending point, a second, lower accrual rate enters: 0 < β2 < β1. (As explained in appendix, there are two, close bending points with two lower accrual rates, but to simplify the exposition, we unify them into one and choose the lower accrual rate.)

With good approximation, the progressive nominal benefits first granted from early January of year t are described by

We describe the real values of wages and benefits as functions of the corresponding nominal variables and the annual price level Pt, recursively defined by Pt = Pt−1Pt, with P0 = 1:

The “real” benefit-real earning link is as follows:

Table 6The impact of the declining real value of bending point on high initial pensions, Hungary, 2012-2023 DISPLAY Table

Column 2 of table 6 displays the accumulated inflation index, ending at 1.65 in 2023. Column 3 presents the real average wage, rising from 100 (2012) to 163 (2023). Inflation depressed the relative value of the bending point from 277.8 (2012) to 199.6 (2022) (both in terms of the average wage in 2012). Compare two beneficiaries, one having a reference wage equal to the average wage and the other triple that amount in year t, respectively; the corresponding benefits are denoted by bt(1) and bt(3), respectively. Those retiring in 2013, receive benefits of 78.7 and 232.5 units, respectively, their ratio being 2.95. Those retiring in 2022, due to the real wage explosion, receive benefits of 116.6 and 311.7 units, respectively, their ratio being 2.637, showing stronger progressivity than before. Moreover, the high initial benefit is lower than that awarded a year before: 311.7 < 332.7! In a certain sense, the accidental strengthening progressivity partially makes up for the elimination of the cap from 2013, though the cap concerns earnings in individual years, while progressivity concerns the average earnings of the assessment period.

6 Summary

At the end of the paper, we shortly summarize the conclusions. Accelerating inflation exposes certain errors in pension indexation rules in general and in Hungary in particular. (i) The higher shares of food and of energy expenditures of households with lower rather than higher incomes call for extended government help when the prices of these basic items grow much faster than the average. (ii) With accelerating inflation, the annual increases of benefits generate large intra-year drops in the real value of those benefits. This can be eliminated by a quarterly or monthly raise, simultaneously diminishing the “lumpiness” of the adjustment. (iii) Under the current imperfect rules, accelerating inflation may weaken or even undermine the incentives of delayed retirement. (iv) Though the strengthening of progressivity is welcome, it is illogical to make the real value of initial pensions depend on the accumulated inflation. (v) If Hungary had retained its pure or mixed wage indexation, while adding a sustainability factor and improving its wage statistics, then the inflationary shock on the pension system would have been weaker. It is disappointing that there is no official discussion of these problems and only an EU initiative requiring public discussion of the Hungarian pension system provides grounds for optimism.

To conclude, we note that Hungary may have one of the worst-designed pension systems in the OECD but other countries may also have similar problems with indexation under fast inflation. Since 2021, the ex-socialist countries have been suffering in particular from two-digit inflation, and the annual indexation of pensions in progress may put a temporary burden on their pensioners’ shoulders. This burden can be diminished by introducing intra-year indexation if necessary!

Appendix

DETAILS OF THE HUNGARIAN PENSION SYSTEM

This appendix elaborates certain details of the Hungarian pension system, skipped in the main text.

Starting with the benefits in progress, since 2010, in January of the given year, they are raised by the inflation rate forecast. If the forecast was pessimistic, then the gain is retained by the pensioners; if the forecast was optimistic, then the government completes the undervalued benefits in November. It is to be underlined that a more sensible solution would be to withhold the extra raise in next years. For example, when 2013, the initial raise was 5.3% and the actual inflation rate was only 1.5%, the arising extra raise of 3.7% should have been credited for future raises.

Turning to the initial benefits, individual net earnings from 1988 (or the start of the carrier if it is later) to the year of retirement are taken into account. First parts of the earnings above the cap are deducted, then they are multiplied the nationwide average growth factors of the previous year except the current year. Having the individual valorised annual wages, their arithmetical average is calculated and transformed by the progressive formula presented as a one-part formula in section 5 above and discussed here as the actual two-part progression.

Since 2013, there have been two bending points to be denoted by w1*< w2* and three aggregated accrual rates to be denoted by β1 > β2 > β3 , implying a progressive benefit function

Numerically, w1*=372,000 HUFs and w2*=421,000 HUFs; β2 = 0.9β1 and β3 = 0.8β1.

Another complication, just mentioned in the main text, is that marginal accrual rates are stepwise linear function of the length of contribution S, rounded-off. Avoiding the details, β1 is an increasing function of S, having several historically determined bending points S1 = 10, S2 = 25, S3 = 36, S4 = 40 and S5 = 50 years starting at β1(10) = 0.33 with annual accrual rates γ1 = 0.02, γ2 = 0.01, γ3 = 0.015, γ4 = 0.02 and ending with γ5 = 0.

Notes

* The author expresses his debt to Hans Fehr, Ádám Reiff, Balázs Reizer and two anonymous referees for their careful remarks on earlier versions.

* The author expresses his debt to Hans Fehr, Ádám Reiff, Balázs Reizer and two anonymous referees for their careful remarks on earlier versions.

Disclosure statement

There is no conflict of interest.

References

Barr, N. and Diamond P., 2008. Reforming Pensions: Principles and Policy Choices. Oxford: Oxford University Press [ CrossRef]

CSO, 2021. Statistical Yearbook. Budapest: Central Statistics Office.

Domonkos, S. and Simonovits, A., 2017. Pension Reforms in EU11 Countries: An Evaluation of Post-socialist Pension Policies. International Social Security Review, 70(2), pp. 109-128 [ CrossRef]

Fischer, S., 1982. Adapting to Inflation in the United States Economy. In: R. Hall, ed. Inflation, Cause and Effects, pp. 169-188.

Lovell, M. C., 2009. Social Security’s Five OASI Inflation Indexing Problems. Economics, 3(1) [ CrossRef]

OECD, 2022. How Inflation Challenges Pensions. Paris: OECD.

Simonovits, A., 2003. Modeling Pension Systems. Oxford: Palgrave Macmillan [ CrossRef]

Stegman, M. A., 2007. Payday Lending. Journal of Economics Perspective, 21(1), pp. 169-190 [ CrossRef]

Whitehouse, E., 2009. Pensions, Purchasing-Power Risk, Inflation and Indexation. OECD Social, Employment and Migration Working Papers, No. 77 [ CrossRef]

Barr, N. and Diamond P., 2008. Reforming Pensions: Principles and Policy Choices. Oxford: Oxford University Press [ CrossRef]

CSO, 2021. Statistical Yearbook. Budapest: Central Statistics Office.

Domonkos, S. and Simonovits, A., 2017. Pension Reforms in EU11 Countries: An Evaluation of Post-socialist Pension Policies. International Social Security Review, 70(2), pp. 109-128 [ CrossRef]

Fischer, S., 1982. Adapting to Inflation in the United States Economy. In: R. Hall, ed. Inflation, Cause and Effects, pp. 169-188.

Lovell, M. C., 2009. Social Security’s Five OASI Inflation Indexing Problems. Economics, 3(1) [ CrossRef]

OECD, 2022. How Inflation Challenges Pensions. Paris: OECD.

Simonovits, A., 2003. Modeling Pension Systems. Oxford: Palgrave Macmillan [ CrossRef]

Stegman, M. A., 2007. Payday Lending. Journal of Economics Perspective, 21(1), pp. 169-190 [ CrossRef]

Whitehouse, E., 2009. Pensions, Purchasing-Power Risk, Inflation and Indexation. OECD Social, Employment and Migration Working Papers, No. 77 [ CrossRef]

|