4061

Views

969

Downloads |

Testing the characteristics of macroprudential policies’ differential impact on foreign and domestic banks’ lending in Croatia

Mario Bambulović*

Miljana Valdec*

Miljana Valdec

Affiliation:

Miljana Valdec

Affiliation: European Central Bank, Frankfurt am Main, Germany

0000-0003-2292-8435 0000-0003-2292-8435

Article | Year: 2020 | Pages: 221 - 249 | Volume: 44 | Issue: 2 Received: June 1, 2019 | Accepted: December 10, 2019 | Published online: June 1, 2020

|

FULL ARTICLE

FIGURES & DATA

REFERENCES

CROSSMARK POLICY

METRICS

LICENCING

PDF

Note: Macroprudential measures are grouped into the instrument categories following definitions in Budnik and Kleibl (2018a). Source: Authors’ calculation based on CNB.

Note: More details about policy action definitions in Budnik and Kleibl (2018a). Source: Authors’ calculation based on CNB and ECB (MaPPED).

|

Sample/Statistics:

|

Liquid Asset

|

TCR

|

Market Share

|

Substitutes

|

NPLR

|

Coverage

|

Net NPLR

|

RIIR on Liabilities

|

LT Liabilities

|

ROA

|

|

Domestic

|

mean

|

31,1

|

19,3

|

0,7

|

0,9

|

18,1

|

49,5

|

9,4

|

1,8

|

31,5

|

0,0

|

|

p25

|

23,7

|

13,5

|

0,2

|

-2,1

|

7,9

|

35,7

|

3,6

|

0,6

|

17,5

|

0,0

|

|

median

|

29,1

|

16,6

|

0,4

|

0,9

|

14,6

|

46,7

|

7,9

|

1,9

|

29,8

|

0,5

|

|

p75

|

35,7

|

23,7

|

0,6

|

4,7

|

24,3

|

62,2

|

13,0

|

3,1

|

45,4

|

1,2

|

|

Foreign

|

mean

|

33,0

|

21,9

|

5,6

|

7,3

|

11,8

|

59,0

|

5,2

|

1,6

|

36,1

|

0,8

|

|

p25

|

24,5

|

14,9

|

0,3

|

-1,3

|

6,0

|

45,1

|

1,8

|

0,2

|

25,2

|

0,3

|

|

median

|

31,1

|

17,6

|

1,0

|

1,4

|

10,4

|

58,9

|

4,0

|

1,3

|

36,4

|

1,1

|

|

p75

|

38,9

|

22,3

|

8,2

|

5,2

|

15,8

|

72,0

|

7,1

|

2,5

|

45,2

|

1,8

|

|

Total

|

mean

|

32,1

|

20,8

|

3,4

|

4,5

|

14,6

|

54,8

|

7,1

|

1,7

|

34,0

|

0,4

|

|

p25

|

24,0

|

14,2

|

0,3

|

-1,7

|

6,6

|

39,7

|

2,3

|

0,4

|

20,4

|

0,1

|

|

median

|

30,1

|

17,1

|

0,5

|

1,2

|

11,8

|

54,0

|

5,3

|

1,6

|

34,5

|

0,8

|

|

p75

|

37,4

|

22,8

|

3,3

|

4,9

|

19,5

|

67,7

|

9,5

|

2,8

|

45,3

|

1,6

|

Note: The size of the sample, i.e. the number of bank-event combinations used to estimate the CAAGR is marked in the figure. Source: Authors’ calculations based on CNB data.

|

|

Time period to event (1 period equals 10

days)

|

|

|

-6

|

-5

|

-4

|

-3

|

-2

|

-1

|

0

|

1

|

2

|

3

|

4

|

5

|

6

|

|

|

Policy tightening

|

|

All banks

|

0,01

|

-0,01

|

0,04

|

0.80**

|

0.80**

|

0.70*

|

1.70**

|

0.94**

|

0.85*

|

0,74

|

0,37

|

0,45

|

0,31

|

|

(0.96)

|

(0.97)

|

(0.85)

|

(0.02)

|

(0.02)

|

(0.06)

|

(0.01)

|

(0.04)

|

(0.06)

|

(0.14)

|

(0.47)

|

(0.39)

|

(0.62)

|

|

Domestic

|

0,01

|

-0,01

|

-0,20

|

0,66

|

0.92*

|

0,60

|

0,86

|

0,75

|

0,45

|

0,46

|

-0,01

|

0,06

|

0,01

|

|

(0.97)

|

(0.97)

|

(0.47)

|

(0.21)

|

(0.09)

|

(0.26)

|

(0.18)

|

(0.26)

|

(0.49)

|

(0.52)

|

(0.99)

|

(0.94)

|

(0.99)

|

|

Foreign

|

0,00

|

-0,01

|

0,24

|

0.91**

|

0,70

|

0,75

|

1.24**

|

1.09*

|

1.17*

|

0,96

|

0,69

|

0,78

|

0,55

|

|

(0.98)

|

(0.99)

|

(0.49)

|

(0.03)

|

(0.13)

|

(0.13)

|

(0.03)

|

(0.07)

|

(0.06)

|

(0.16)

|

(0.34)

|

(0.31)

|

(0.5)

|

|

|

Policy loosening

|

|

All banks

|

0,07

|

-0,02

|

-0,09

|

-0,29

|

-0,30

|

0,01

|

0,10

|

0,18

|

0,29

|

0,46

|

0,41

|

0,48

|

0,66

|

|

(0.61)

|

(0.89)

|

(0.62)

|

(0.18)

|

(0.2)

|

(0.96)

|

(0.73)

|

(0.58)

|

(0.38)

|

(0.21)

|

(0.28)

|

(0.22)

|

(0.12)

|

|

Domestic

|

-0,01

|

-0,11

|

-0,21

|

-0.51*

|

-0,49

|

-0,13

|

-0,16

|

0,12

|

0,19

|

0,28

|

0,31

|

0,16

|

0,35

|

|

(0.97)

|

(0.54)

|

(0.36)

|

(0.1)

|

(0.12)

|

(0.69)

|

(0.69)

|

(0.79)

|

(0.66)

|

(0.6)

|

(0.58)

|

(0.77)

|

(0.58)

|

|

Foreign

|

0,13

|

0,05

|

0,01

|

-0,11

|

-0,14

|

0,13

|

0,31

|

0,24

|

0,36

|

0,61

|

0,50

|

0,75

|

0,93

|

|

(0.37)

|

(0.84)

|

(0.98)

|

(0.72)

|

(0.68)

|

(0.72)

|

(0.44)

|

(0.62)

|

(0.44)

|

(0.23)

|

(0.35)

|

(0.17)

|

(0.11)

|

|

|

Other and with ambiguous impact

|

|

All banks

|

-0,07

|

-0,16

|

0,34

|

0.78**

|

0.54*

|

0,41

|

0,44

|

0,09

|

0,22

|

0,16

|

0,43

|

0,83

|

0,31

|

|

(0.7)

|

(0.44)

|

(0.25)

|

(0.01)

|

(0.1)

|

(0.22)

|

(0.39)

|

(0.87)

|

(0.69)

|

(0.79)

|

(0.52)

|

(0.24)

|

(0.68)

|

|

Domestic

|

-0,33

|

-0,21

|

0,57

|

0.98*

|

0,74

|

0,54

|

0,86

|

0,57

|

1,17

|

0,89

|

1,19

|

1,94

|

1,30

|

|

(0.36)

|

(0.55)

|

(0.29)

|

(0.05)

|

(0.15)

|

(0.3)

|

(0.37)

|

(0.55)

|

(0.23)

|

(0.39)

|

(0.3)

|

(0.11)

|

(0.3)

|

|

Foreign

|

0,14

|

-0,12

|

0,15

|

0.62*

|

0,37

|

0,31

|

0,09

|

-0,31

|

-0,55

|

-0,44

|

-0,19

|

-0,07

|

-0,49

|

|

(0.45)

|

(0.62)

|

(0.63)

|

(0.1)

|

(0.37)

|

(0.48)

|

(0.86)

|

(0.6)

|

(0.39)

|

(0.5)

|

(0.81)

|

(0.93)

|

(0.59)

|

Note: P-value of two-sided cross-sectional t-test of CAAGR significance in parentheses. The null hypothesis of the test assumes that the CAAGR is equal to zero. *** p < 0.01, ** 0.01 < p < 0.05, * 0.05 < p < 0.1. Source: Authors’ calculations based on CNB data.

|

|

Sample:

Variables

|

Foreign

|

|

Model 1

|

Model 2

|

Model 3

|

Model 4

|

Model 5

|

Model 6

|

Model 7

|

|

MPP

|

MPP stance_HR

|

-1.02***

|

-1.04***

|

-1.10***

|

|

|

|

|

|

(0.15)

|

(0.17)

|

(0.15)

|

|

|

|

|

|

MPP

stance_Homea

|

|

|

|

-1.15***

|

-1.10***

|

-1.16***

|

|

|

|

|

(0.36)

|

(0.35)

|

(0.27)

|

|

|

Macro

variables

|

GDP growth

|

0,22

|

|

|

1.04***

|

|

|

|

|

(0.24)

|

|

|

(0.31)

|

|

|

|

|

Consumption

growth

|

|

-0,03

|

|

|

0.99**

|

|

|

|

(0.31)

|

|

|

(0.35)

|

|

|

|

Macro factor

|

|

|

0,17

|

|

|

1.17**

|

|

|

|

(0.35)

|

|

|

|

|

|

Bank

variables

|

Liquid asset

|

0.15*

|

0.14*

|

|

0.27**

|

0.25**

|

|

0,11

|

|

(0.08)

|

(0.08)

|

|

(0.1)

|

(0.1)

|

|

(0.11)

|

|

TCR

|

|

|

-0,14

|

|

|

0,14

|

|

|

|

(0.13)

|

|

|

(0.13)

|

|

|

Market share

|

-1.30*

|

-1.29*

|

-1.44**

|

-0,59

|

-0,68

|

-0,68

|

-1.46*

|

|

(0.66)

|

(0.68)

|

(0.65)

|

(1.06)

|

(1.05)

|

(1.36)

|

(0.73)

|

|

Substitutes

|

0.31**

|

0.30**

|

0.30**

|

0.32**

|

0.32**

|

0.39**

|

0.31**

|

|

(0.13)

|

(0.13)

|

(0.12)

|

(0.14)

|

(0.14)

|

(0.15)

|

(0.12)

|

|

NPLR

|

-0,12

|

-0,07

|

|

0,01

|

0,06

|

|

0

|

|

(0.23)

|

(0.23)

|

|

(0.23)

|

(0.23)

|

|

(0.31)

|

|

Coverage

|

0,03

|

0,03

|

|

0.15***

|

0.15***

|

|

0,03

|

|

(0.06)

|

(0.06)

|

|

(0.05)

|

(0.04)

|

|

(0.06)

|

|

Net NPLR

|

|

|

-0,13

|

|

|

-0,13

|

|

|

|

(0.47)

|

|

|

(0.49)

|

|

|

RIIR on

liabilities

|

-1.97***

|

-2.10***

|

-1.97***

|

-0,01

|

0,27

|

0,51

|

-1.28**

|

|

(0.55)

|

(0.61)

|

(0.57)

|

(0.44)

|

(0.44)

|

(0.46)

|

(0.44)

|

|

LT

liabilities

|

0.24*

|

0.23*

|

0.18**

|

0,19

|

0,21

|

0,12

|

0,23

|

|

(0.12)

|

(0.12)

|

(0.08)

|

(0.13)

|

(0.13)

|

(0.12)

|

(0.13)

|

|

ROA

|

-0,69

|

|

|

-0,21

|

|

|

-0,57

|

|

(0.5)

|

|

|

(0.52)

|

|

|

(0.5)

|

|

|

Constant

|

25.48**

|

25.82**

|

37.82***

|

-8,9

|

-9,08

|

7,58

|

29.34*

|

|

(10.44)

|

(11.5)

|

(7.43)

|

(10.19)

|

(10.09)

|

(9.21)

|

(16.29)

|

|

|

Observations

|

1,052

|

1,052

|

1,052

|

1,052

|

1,052

|

1,052

|

1,063

|

|

R-squared

|

0,35

|

0,35

|

0,35

|

0,25

|

0,25

|

0,21

|

0,38

|

|

Number of

Banks

|

17

|

17

|

17

|

17

|

17

|

17

|

17

|

|

Bank FE

|

YES

|

YES

|

YES

|

YES

|

YES

|

YES

|

YES

|

|

Year FE

|

NO

|

NO

|

NO

|

NO

|

NO

|

NO

|

YES

|

*** p < 0.01, ** 0.01 < p < 0.05, * 0.05 < p < 0.1. Source: Authors’ calculations.

|

|

Sample:

Variables

|

Foreign

|

|

Model 1

|

Model 2

|

Model 3

|

Model 4

|

Model 5

|

Model 6

|

Model 7

|

|

MPP

|

MPP stance_HR

|

-0.35***

|

-0.45***

|

-0.32**

|

|

|

|

|

|

(0.1)

|

(0.12)

|

(0.11)

|

|

|

|

|

|

MPP

stance_Homea

|

|

|

|

-0.54**

|

-0.60**

|

-0.54**

|

|

|

|

|

|

(0.23)

|

(0.25)

|

(0.2)

|

|

|

Macro variables

|

GDP growth

|

-0,37

|

|

|

-0,09

|

|

|

|

|

(0.28)

|

|

|

(0.24)

|

|

|

|

|

Consumption

growth

|

|

-0.60*

|

|

|

-0,15

|

|

|

|

|

(0.3)

|

|

|

(0.25)

|

|

|

|

Macro factor

|

|

|

-0.391

|

|

|

-0.105

|

|

|

|

|

(0.36)

|

|

|

(0.33)

|

|

|

Bank

variables

|

Liquid asset

|

0.47***

|

0.48***

|

|

0.53***

|

0.57***

|

|

0.52***

|

|

(0.15)

|

(0.16)

|

|

(0.15)

|

(0.16)

|

|

(0.15)

|

|

TCR

|

|

|

0.35**

|

|

|

0.49***

|

|

|

|

|

(0.14)

|

|

|

(0.12)

|

|

|

Market share

|

-5,26

|

-4,57

|

-9.13*

|

-4,28

|

-3,57

|

-7.98**

|

-1,67

|

|

(3.43)

|

(3.54)

|

(4.31)

|

(2.5)

|

(2.36)

|

(3.11)

|

(3.67)

|

|

Substitutes

|

0.31*

|

0.31*

|

0.33*

|

0.32*

|

0.32*

|

0.36**

|

0.37**

|

|

(0.16)

|

(0.15)

|

(0.16)

|

(0.16)

|

(0.15)

|

(0.15)

|

(0.17)

|

|

NPLR

|

-0.34***

|

-0.39***

|

|

-0.25***

|

-0.31***

|

|

-0.26***

|

|

(0.06)

|

(0.05)

|

|

(0.07)

|

(0.06)

|

|

(0.07)

|

|

Coverage

|

0,06

|

0,07

|

|

0,1

|

0.11*

|

|

0,08

|

|

(0.06)

|

(0.06)

|

|

(0.06)

|

(0.06)

|

|

(0.07)

|

|

Net NPLR

|

|

|

-0.61***

|

|

|

-0.51**

|

|

|

|

|

(0.18)

|

|

|

(0.18)

|

|

|

RIIR on

liabilities

|

-0.64*

|

-1.01***

|

-0.94***

|

0,04

|

0,02

|

-0,22

|

-0.81*

|

|

(0.33)

|

(0.3)

|

(0.29)

|

(0.47)

|

(0.49)

|

(0.36)

|

(0.42)

|

|

LT

liabilities

|

0.29*

|

0.29*

|

0,23

|

0.31*

|

0.31*

|

0,27

|

0.31**

|

|

(0.14)

|

(0.14)

|

(0.2)

|

(0.15)

|

(0.15)

|

(0.2)

|

(0.14)

|

|

ROA

|

0.52***

|

|

|

0.72***

|

|

|

0.77***

|

|

(0.16)

|

|

|

(0.23)

|

|

|

(0.21)

|

|

|

Constant

|

-3,74

|

-1,34

|

11,91

|

-16.37*

|

-17.38*

|

0,43

|

-11,34

|

|

(10.15)

|

(10.43)

|

(7.81)

|

(9)

|

(9.1)

|

(6.67)

|

(14.72)

|

|

|

Observations

|

837

|

837

|

837

|

837

|

837

|

837

|

850

|

|

R-squared

|

0,27

|

0,28

|

0,24

|

0,26

|

0,25

|

0,23

|

0,31

|

|

Number of

Banks

|

14

|

14

|

14

|

14

|

14

|

14

|

14

|

|

Bank FE

|

YES

|

YES

|

YES

|

YES

|

YES

|

YES

|

YES

|

|

Year FE

|

NO

|

NO

|

NO

|

NO

|

NO

|

NO

|

YES

|

a MPP_stance_EU represents simple average of individual EU countries’ macroprudential policy stance indexes. Note: All RHS variables are lagged one year. Robust standard errors in parentheses. *** p < 0.01, ** 0.01 < p < 0.05, * 0.05 < p < 0.1 Source: Authors’ calculations.

|

Sample:

Variables

|

Foreign

|

Domestic

|

|

Pre-crisis

|

Crisis

|

Pre-crisis

|

Crisis

|

|

MPP

|

MPP stance_HR

|

-0.948***

|

|

-0.935

|

|

-0.178

|

|

-0.302

|

|

|

0,261

|

|

0,615

|

|

0,212

|

|

0,613

|

|

|

MPP stance_Home*

|

|

-5.633**

|

|

0.330

|

|

-7.121*

|

|

0.127

|

|

|

2,056

|

|

0,354

|

|

3,728

|

|

0,59

|

|

Macro

|

GDP growth

|

0.443

|

-0.557

|

0.171

|

-0.197

|

-0.370

|

-0.0991

|

-0.576

|

-0.725***

|

|

0,918

|

1,084

|

0,224

|

0,371

|

0,835

|

0,837

|

0,462

|

0,233

|

|

Bank

variables

|

Liquid asset

|

0.393*

|

0.625***

|

0.112

|

0.0873

|

0.304

|

0.286

|

0.523**

|

0.524**

|

|

0,221

|

0,208

|

0,0991

|

0,124

|

0,274

|

0,264

|

0,196

|

0,203

|

|

Market share

|

-1.911

|

-1.402

|

-1.294

|

-1.524

|

-8.276*

|

-7.374

|

-3.180

|

-2.783

|

|

1,151

|

1,395

|

1,196

|

1,338

|

4,258

|

4,417

|

10,53

|

11,75

|

|

Substitutes

|

0.167

|

0.212

|

0.370***

|

0.380***

|

0.419*

|

0.423*

|

0.199

|

0.205

|

|

0,231

|

0,285

|

0,121

|

0,118

|

0,203

|

0,207

|

0,128

|

0,133

|

|

Net NPLR

|

-0.735

|

-0.646

|

0.0233

|

0.169

|

-0.547**

|

-0.610**

|

-0.367*

|

-0.357*

|

|

0,52

|

0,654

|

0,676

|

0,722

|

0,242

|

0,24

|

0,189

|

0,18

|

|

RIIR on liabilities

|

-2.859

|

-0.170

|

-1.503

|

-0.984

|

-0.609

|

-0.866

|

-0.236

|

-0.106

|

|

1,814

|

1,695

|

1,019

|

0,799

|

0,389

|

0,504

|

0,594

|

0,511

|

|

LT liabilities

|

0.330

|

0.256

|

-0.0702

|

-0.0399

|

0.591

|

0.617

|

0.155

|

0.158

|

|

0,222

|

0,261

|

0,214

|

0,232

|

0,436

|

0,447

|

0,102

|

0,124

|

|

ROA

|

-0.0616

|

0.286

|

0.0550

|

0.0346

|

0.458

|

0.456

|

0.710**

|

0.707**

|

|

0,808

|

0,899

|

1,438

|

1,415

|

0,323

|

0,334

|

0,254

|

0,246

|

|

Constant

|

18.47

|

2.288

|

34.40**

|

7.721

|

-3.224

|

-1.906

|

-4.585

|

-13.93

|

|

17,38

|

15,6

|

15,06

|

10,53

|

16,45

|

16,16

|

23,31

|

10,67

|

|

Observations

|

443

|

443

|

609

|

609

|

364

|

364

|

473

|

473

|

|

R-squared

|

0.214

|

0.169

|

0.065

|

0.054

|

0.140

|

0.155

|

0.179

|

0.178

|

|

Number of Banks

|

17

|

17

|

17

|

17

|

14

|

14

|

14

|

14

|

|

Bank FE

|

YES

|

YES

|

YES

|

YES

|

YES

|

YES

|

YES

|

YES

|

|

Year FE

|

NO

|

NO

|

NO

|

NO

|

NO

|

NO

|

NO

|

NO

|

Note: All RHS variables are lagged one year. Robust standard errors in parentheses. *** p < 0.01, ** 0.01 < p < 0.05, * 0.05 < p < 0.1. Source: Authors’ calculations.

|

|

|

Abstract

In the aftermath of the 2008 financial crisis, macroprudential measures were labelled as policymakers’ best response to systemic risk and macro-financial imbalances, with their effectiveness still largely unknown due to limited use of such measures. The purpose of this paper is to clarify the potentials and limitations of these measures by evaluating both the immediate and the overall impact of macroprudential policies on banks’ lending to the non-financial private sector in Croatia. The findings reveal the divergent impact of macroprudential measures on banks’ lending with regards to their direction, i.e. tightening or loosening. Policy makers should bear this in mind when opting for a tightening of their policy stance as the reversal of that action may not match the initial impact of its introduction. Additionally, from a policymaker perspective, this paper provides potential evidence of cross-border policy spillovers, which should be taken into account in order to conduct an effective macroprudential policy.

Keywords: bank lending; cross-border policy spillovers; effectiveness; impact study analysis; limitations; macroprudential measures; potential; systemic risk

JEL: C23, E44, F42, G14, G21, G28

1 Introduction

The global financial crisis showed that excessive bank lending can lead to impaired financial stability, which, if not addressed promptly and adequately, can have serious economic and social costs. Therefore, it is necessary to understand the underlying drivers of credit growth, especially in the case of emerging market economies with bank-centric financial systems, such as Croatia, where credit is the predominant channel of financial transmission. The impact of macroprudential (MP) policy actions on bank lending has gained in importance in the post-crisis period, as growing numbers of authorities have recognised the limitations of conventional policies in safeguarding financial stability and decided to take their policy toolbox into more unconventional, i.e. macroprudential territory.

Following the growing body of literature that recognizes both the importance of credit flows for the smooth functioning of the economy and their potential for major disruptions if proven to be unsustainable, numerous central banks put the preservation of financial stability among their main goals. In the pre-crisis period the vast majority of macroprudential measures were conducted by developing countries and were oriented at taming rapid and excessive credit growth. The introduction and application of macroprudential measures among developed countries intensified only after the crisis and with the introduction of the Basel III framework. Nevertheless, as these measures are still rather a new phenomenon, little is known about their effectiveness and they are still under-researched (Claessens, Kose and Terrones,  2011 2011).

The macroprudential experience of Croatia from the beginning of 2000 is especially rich and still relatively unexplored. The Croatian National Bank (CNB) is one of just a few central banks during the last two decades to have relied heavily on the use of countercyclical macroprudential policy in order to smooth out the financial cycle and safeguard the stability of the banking system (Lim et al., 2011; Dumičić, 2017; Budnik and Kleibl, 2018a). In the years preceding the global financial crisis, the CNB employed a great variety of measures in order to limit rapid credit growth and to increase the resilience of the financial system. Therefore, Croatia is an interesting candidate for a case study on the analysis of the potential effect of macroprudential policies on credit growth. Given the high share of foreign-owned banks 1 in the Croatian financial system (Figure 1), we investigate whether some differential effects of macroprudential policies can be observed for domestic and foreign banks. Differences in the business practices of foreign and domestic banks are well documented in the literature (Claessens, Demirguc-Kunt and Huizinga, 2001; Kraft, 2002; De Haas and Lelyveld, 2006; Arakelyan, 2018), but the effects of macroprudential policies on their lending are still underexplored, which motivated us to differentiate the analysis on these two subsamples of banks.

Furthermore, taking into account the share of foreign banks in the Croatian financial system, the prudential policies conducted by authorities from countries that represent the home countries of foreign credit institutions should also matter (Emter, Schmitz and Tirpak, 2018). We shall explore the possible existence of outward macroprudential policy spillovers, which can be defined as effects of a macroprudential policy action carried out by foreign country on the domestic economy (ESRB, 2014). Therefore, we also include in the model the macroprudential stance of home authorities of Croatian banks in foreign ownership and explore their effects on lending activities in Croatia.

Figure 1Ownership structure of the Croatian banking system DISPLAY Figure

A micro data set containing highly granular supervisory data collected by the Croatian National Bank, spanning 19 years and taking in 31 banks is utilized in the analysis. The immediate impact of MP measures on bank lending was estimated on high-frequency 10-day data by employing event study analysis. To assess the overall effect of MP measures on bank lending, we used a fixed effects panel model on quarterly data; panel regression is particularly valuable as it allows us to examine the effects of macroprudential actions while also controlling for idiosyncratic characteristics of banks, unobserved heterogeneity among banks, and macroeconomic developments. We also looked for any shifts in bank behaviour during the crisis by looking at the pre-crisis and crisis periods separately.

Event study analysis reveals the asymmetric impact of MP measures with respect to direction, as the introduction of tightening MP measures had a statistically significant impact on banks’ lending, whereas loosening MP actions of the central bank did not cause a significant shift in banks’ lending behaviour. The results show that a few periods prior to the introduction of policy tightening measures, banks reacted procyclically, that is they increased their lending in anticipation of regulatory tightening. Through a series of estimations, we find that the regulatory environment was one of the major factors influencing lending in Croatia, and that this effect varies depending on individual bank ownership characteristics. Our findings suggest that the tightening of the aggregate macroprudential policy stance in Croatia primarily influenced foreign banks’ lending and had only a limited effect on domestic banks. In addition, we provide some preliminary evidence for policy spillovers from regulatory policies in other European countries on lending activity in Croatia. Results show that regulatory spillovers are not only present through a direct parent-daughter channel, but also through indirect channels.

The rest of the paper is organized as follows: section 2 reviews the related literature. Section 3 describes the dataset and methodology used in empirical analysis. In section 4 the main results are presented and, finally, section 5 concludes.

2 Literature overview

Although the popularity of macroprudential measures has greatly increased since the global financial crisis, a proper evaluation of the effectiveness of these kinds of policies is still rather scarce. On one hand, in developing countries, where experience with the use of macroprudential policies is richer, there are still restrictions in terms of data availability thus limiting the possibility of evaluating the effects of different policies. On the other hand, in many developed countries macroprudential measures have been introduced only in response to the recent crisis, which also makes it difficult to assess empirically their effectiveness and transmission channels. Even if the literature on the effectiveness of macroprudential policies is still in an early stage, there is an increasing interest in evaluating the impact of different instruments through theoretical models or empirical examples.

In the theoretical literature related to evaluation of the impact of macroprudential policies on different economic dimensions, authors mostly use Dynamic Stochastic General Equilibrium Models (DSGE). Most of their findings show that macroprudential policies have a potential role in dampening the credit cycles and that they are more effective if used to complement monetary policies (Angelini, Neri and Panetta, 2011; Agénor, Alper and da Silva, 2012; Brunnermeier and Sannikov, 2014 etc.).

The empirical literature dealing with assessments of the impact of macroprudential policies on a wide array of economic variables of interest can broadly be divided into several areas depending on the information used. One strand of the literature employs aggregate information at the country level, where most of the papers have used aggregate macro data to evaluate the impact of different policies on some variable of interest like credit growth, housing prices or macroeconomic variables and they commonly use panel data regressions at the country level or event studies. They find that the tightening of macroprudential policies is associated with lower bank credit growth and house price inflation (Bruno, Shim and Shim, 2015 ; Cerutti, Claesens and Laeven, 2017; Akinci and Olmstead-Rumsey, 2018) and that these effects appear to be smaller in more financially developed and open economies (Cerutti, Claesens and Laeven, 2017). Moreover, macroprudential policies seem to be more successful when they complement monetary policy by reinforcing monetary tightening than when they act in opposite directions (Bruno, Shim and Shim, 2015 ). Regarding the second strand of the literature, authors use information at bank level to evaluate the impact of various macroprudential policies on individual banking indicators. Authors have mainly found that borrower-based measures like loan-to-value (LTV) and debt-to-income (DTI) caps seem to be somewhat more effective than capital requirements in containing credit growth (Akinci and Olmstead-Rumsey, 2018; Claessens, Ghosh and Mihet, 2013 and Lim et al., 2011). Other than that, Cerutti, Claesens and Laeven ( 2017) find negative effects of dynamic provisioning, reserve requirement measurements, limits on FX loans, and concentration limits on credit growth. Other papers find that the implementation of macroprudential policies can generate spillover effects. For instance, Aiyar, Calomiris and Wieladek ( 2014) study the effects of bank capital regulation in the UK and found that regulated banks reduce lending in response to tighter capital requirements while at the same time unregulated banks increase lending. More recently, to estimate the impact of macroprudential policies authors have used information that is more granular at the bank-debtor relationship level or credit registry data but there are still relatively few papers in the literature that have used this information to evaluate certain policies. For example, Jiménez et al. ( 2015) examine the effect of countercyclical provisions on credit growth in Spain and find that they were successful in reducing the effects of a credit crunch but they were not as successful in curbing the pre-crisis credit boom.

Empirical studies focusing on the effects of regulatory policies on specific institutions depending on their ownership status are still in their infancy and are mostly focused on their role on financial stability and transmission channels of shocks. Papers focusing on the period prior to the crisis find evidence of a stabilizing role of foreign banks as they are a source of diversification and act as a shock absorber during local crises (De Haas and van Lelyveld, 2006; Arena, Reinhart and Vazquez, 2007; Havrylchyk and Jurzyk, 2011; Cull, Martínez Pería and Verrier, 2017). In the post-crisis studies, foreign ownership of banks showed a more divergent face. Some authors find supporting evidence for the view that foreign banks can act as a source of contagion, increase volatility and import economic or financial shocks from home to host countries (Cull and Martinez Peria, 2013; Cull, Martínez Pería and Verrier, 2017). Arakelyan ( 2018) adds to this strand of literature by using data on 16 CESEE economies and stresses the importance of monitoring the health of foreign parent banks as well as the potential regulatory changes in their home jurisdictions. On the other hand, authors also find that in some countries foreign banks continue to support a high overall degree of banking sector stability (Barboni, 2017).

For the case of Croatia, there are several papers but they mostly consider various aspects of credit growth analysis (Čeh, Dumičić and Krznar, 2011; Pintarić, 2016; Dumičić and Ljubaj, 2017). Other than that, some papers also discuss the role of policy makers on credit growth. Ljubaj ( 2012) confirmed the existence of a longrun relation between household loans, the macroeconomic environment factor and the monetary policy indicator, while no such relation was confirmed for corporate loans. The author concluded that it was probably due to the fact that enterprises raised substantial funds from abroad, while households were financed predominantly by domestic banks. Furthermore, Dumičić’s ( 2017) estimation shows that macroprudential policies in CEE countries, including Croatia, were more effective in slowing credit to households than credit to the non-financial corporate (NFC) sector. This again can be attributed to the NFC sector’s having had access to non-bank and cross-border credit in addition to domestic bank credit.

Even though, the issue of effects of regulatory policies on lending dynamics in Croatia is not new in the literature, we re-examine it by conducting an extensive analysis focusing on differences between foreign and domestically owned banks and by introducing a novel variable that takes into account the impact of the regulatory environment on credit intermediation, namely the macroprudential stance index.

Literature that employs event-study methodology to assess the impact of central banks’ actions mainly focuses on the impact these measures have on financial markets. In recent years this stream of literature predominantly focussed on the impact of the ECBs’ unconventional monetary policy on financial conditions in the Euro Area (Ambler and Rumler, 2017; Briciu and Lisi, 2015; McQuade, Falagiarda and Tirpák, 2015; Rivolta, 2014). To the best of our knowledge this is the first paper that deals with the issue of the immediate impact of macroprudential measures on banks’ behavior, more specifically on banks’ lending to private sector.

3 Data and methodology

3.1 Experience with macroprudential policies in Croatia

The beginning of the 2000s in Croatia was marked by rapid credit growth, which lasted until 2008. Conditions that contributed to the strong growth can be found in stable inflation and stable exchange rates that lowered the risk perception of the Croatian economy which, accompanied by a widened gap between expected return on investment in Croatia and the EU, attracted foreign capital and therefore positively contributed to credit growth (Rohatinski, 2015). Moreover, competition between banks for new clients became fiercer, as Croatia was seen as a country with a big financial deepening potential. On the demand side, the tendency towards spending and consumption was rapidly growing in both public and private sectors. Therefore, all the preconditions were met for the rapid credit expansion that followed. In the 2000-2003 period, according to CNB data, bank credit grew on average by 23.7% on a yearly basis, which was mainly financed by foreign capital inflows (Figure 2).

Figure 2Real and financial cycle development (y-o-y in %) DISPLAY Figure

In 2003, it was obvious that a lending boom was underway in Croatia and what is more, it was followed by increasing asset prices, implying the creation of a vicious cycle between financial and macroeconomic aggregates. Specifically, credit expansion led to increased asset prices, and this encouraged investors and raised the value of collateral, which furthermore fuelled credit growth (Figure 2). The central bank decided to act with a broad set of relatively unconventional measures, which at that time were not even known as “macroprudential”, in order to curb booming credit growth. There were several reasons for the use of macroprudential measures instead of more conventional monetary tightening measures. The inherent characteristics of domestic economy with respect to size, openness, high euroization level, strong capital inflows and relatively high foreign indebtedness severely limited the scope for a conventional monetary policy. This was additionally boosted by global developments characterized by financial liberalization, convergence process of emerging markets, high global liquidity and low risk aversion. In order to address these issues, different measures were implemented, but those used the most frequently were related to limits to credit growth and volume (Figure 3). The most important pre-crisis measures were the high level of the general reserve requirement, administrative restriction of loan growth, introduction of marginal reserve requirements, special reserve requirement and minimum required foreign currency claims. Other than that, the CNB increased capital requirements for currency induced credit risk and capital adequacy requirements. For more details about the macroprudential policy of the CNB in the pre-crisis period, the reader is referred to Kraft and Galac ( 2011), Dumičić and Šošić ( 2014), Dumičić ( 2017) and Vujčić and Dumičić ( 2016).

Figure 3Frequency of CNB macroprudential policy actions by type of instrument category, 2000-2018 DISPLAY Figure

Other than in Croatia, a somewhat greater use of macroprudential policies in the pre-crisis period can also be observed in Central and Eastern European (CEE) countries 2 than elsewhere in Europe which is largely explained by the financial sector structure and the overall level of financial development in these countries (Figure 4). Other than the use of a great variety of macroprudential tools within countries, the data also show that CEE countries were active in changing the intensity of measures as well and Croatia is again one of the most active countries. Nonetheless, empirical studies focusing on the nature of macroprudential policies find evidence that only a few CEE countries in pre-crisis period used countercyclical macroprudential policies. These countries are Croatia, Bulgaria and Romania (Lim et al., 2011; Dumičić, 2017; Budnik and Kleibl, 2018a).

Macroprudential measures were able to partially slow down the accumulation of systemic risk, while strengthening banks’ resiliency through a build-up of liquidity and capital buffers. It should also be noted that the efficiency of these measures was partially reduced due to their circumvention through the less regulated parts of the financial system or by the transference of operations from local banks to their parent banks. They also motivated banks to raise capital rather than borrow from abroad (Kraft and Galac, 2011; Vujčić and Dumičić, 2016). As a result of all these efforts, the Croatian banking system did not experience the fate of some other banking systems, as it remained sound, resilient and without major bank failures throughout the global financial crisis. After the onset of the global financial crisis, the CNB gradually released the previously accumulated reserves and credit growth restrictions were removed. Despite the fact that Croatia sidestepped the financial crisis in 2008, the economy experienced the longest recession of all EU countries; it lasted for six years until 2015. On the other hand, credit growth has only recently showed signs of recovery.

Figure 4Frequency of policy actions by objective of the policy measure for CEE countries, 2000-2018 DISPLAY Figure

3.2 Data

To evaluate the effects of aforementioned macroprudential policies on domestic and foreign banks’ lending we use supervisory data reported by banks operating in Croatia at the unconsolidated level. The use of unconsolidated data enables us to explore solely developments in the domestic market, which is in the focus of this paper. The event study analysis of MP measures’ impact was estimated on the most frequent available (10-day) data, while panel regression analysis was employed on quarterly data. This data is highly granular and it allows us to use a wide number of variables to control for various factors of banking activity. Other than that, we use the different macroeconomic variables reported by the different institutions, such as CBS, EC, CNB, etc.

This analysis focuses on a 19 year-period (December 1999 to September 2018) by using a panel dataset covering 31 banks. We impose the restriction that a bank must have been present in the market for at least half of the observed time period to enter into the sample. As not all banks were active during the overall observed period, the resulting panel is unbalanced. Furthermore, in panel regression analysis simple outlier treatment to dataset is applied. We eliminate outliers 3 from the sample across banks and time periods if the value of the annual credit growth to private sector exceeds 100%.

3.3 Methodology

3.3.1 Event study analysis

The immediate impact of CNB macroprudential policies on banks’ lending is estimated by applying event study methodology, where we check for a potential differential impact on domestic and foreign banks by splitting up the sample into two subsamples. We also differentiate according to policy action direction as we separately estimate the impact of tightening, loosening and other measures with ambiguous impact. In order to setup the event-study methodology, certain facets of the study design have to be specified. First off, we have to define what constitutes an event. Because MP actions of the CNB in certain instances occurred in clusters (i.e. they occurred in the same month), we treat the interventions in the same cluster as a single event. When this definition of an intervention cluster is used, the sample of events is reduced to 54 out of the initial 113 events. We assume that the direction of that event is tightening if more tightening measures occurred than loosening measures and vice versa. Next, we have to define the length of an event window on which the effect of MP measures’ introduction on banks’ lending is tested. Longer event windows allow for the possibility of a more gradual effect of an event, but at the same time banks’ lending can be influenced by other drivers over longer event windows. We chose a window that starts 6 periods (2 months) before the event and ends 6 periods after the event. Moreover, in order to measure the effect of an event on bank lending, we have to calculate abnormal growth rates of bank loans to the non-financial private sector at individual bank level. We define them as the difference between observed growth rates and the “normal” growth rates of bank lending. For the estimation of normal growth rates, we chose the mean adjusted returns model which assumes that the expected growth rate of loans in the event window differs across banks and is equal to the average return of a bank observed in the estimation window, which in our case is defined as 36 periods (1 year) prior to event window. Even though the mean adjusted returns model is relatively simple compared to other models, Brown and Warner (1980; 1985) show that results based on this model do not systematically deviate from results based on more sophisticated models in short-term event studies. Finally, the statistical significance of MP events at period τ are estimated on cumulative average abnormal growth rate (CAAGR) statistics that can be defined as:

| (1) |

where τ ∈{–6, 6} is a period from event window, Nτ is a number of banks active at date corresponding to period τ, CAGRiτ is cumulative abnormal growth rate of bank i in period τ, AGRiτ, NGRiτ and GRiτ are respectively abnormal, normal and the observed 10-day growth rates of bank i loans to non-financial private sector in period τ.

3.3.2 Panel regression analysis

In order to estimate the through-the-cycle effect of the cumulative macroprudential stance we use a panel regression model as panel data, with their cross-sectional and time dimensions, provides us with the necessary variability in data that is indispensable to be able to estimate the impact of macro variables such as macroprudential policy stance on bank lending, while avoiding the occurrence of spurious regression. Additionally, a panel data model allows us to test the hypothesis that the macroprudential policy actions of a central bank unevenly affect domestic and foreign banks by splitting the full sample into two subsamples. Specifically, we use panel regressions with fixed effects4, since fixed effects estimation allows for arbitrary correlation between the unobserved bank specifics and the observed explanatory variables (Wooldridge, 2002). Furthermore, under the assumption of strict exogeneity, it also takes into account bank-specific differences. We prefer a static to a dynamic model due to the relatively low correlation between current and lagged values of credit growth. The static panel data model with fixed effects can be specified as:

| Ci,t = α + βXit + γZt + δMPPt + ui + εi,t | (2) |

where the subscripts i and t are indices for bank and time, Ci,t denotes the dependent variable (quarterly credit growth on annual basis), α is the intercept, MPPt captures the overall macroprudential policy stance of the country, Xit is a vector of bank specific variables, Zt is a vector of macro variables, ui is a bank fixed effect that enables us to control for unobserved bank-level characteristics and εi,t is the idiosyncratic error term.

In order to check for any unspecified macro effect, time specific fixed effects are included in complementary specifications:

| Ci,t = α + βXit + ui + λt + εi,t | (3) |

where, along with other variables mentioned above, λt captures time fixed effects. Depending on the model specification, the exact choice of control variables differs. In order to minimize any endogeneity problems between explanatory bank specific variables and the dependent variable, we lag all RHS variables by four quarters. To control for possible multicollinearity issues between regressors, we include highly correlated variables in separate model specifications. We use banklevel clustered, robust standard errors to correct for heteroscedasticity. Any possible shift in banks behaviour in the crisis 5 period, relative to the pre-crisis period, is also examined in this paper. We use December 2008 as a cut-off date based on Wald structural break test 6.

3.4 Description of variables

The dependent variable of interest is the year on year real credit growth to households and non-financial corporation sectors, i.e. the private sector. The nominal growth rate of credit to the private sector calculated from balance sheet stocks can be highly influenced by non-performing loan write-offs and, in the case of a banking system that is characterized by a high share of foreign currency lending such as the Croatian, by sudden changes in exchange rates. Therefore, in order to capture “pure credit growth”, data on nominal credit growth was cleansed from these effects. Additionally, this variable is transformed into real terms to correct for the effect of price level change on lending (Figure 5).

Figure 5Nominal and adjusted growth of total credit to private sector (%) DISPLAY Figure

In the measurement of policy intensity, several options are possible. The macroprudential policy index can be represented as a dummy variable, a number of instruments in place or as a cumulated index of net tightening. In this setting, the aggregate index used characterizes the macroprudential policy stance of a country by cumulating the number of tightening and easing events since end-1999 (Akinci and Olmstead-Rumsey, 2018; Budnik and Kleibl, 2018a), which can be defined as:

| (4) |

where Tτ is the number of tightening measures introduced in quarter τ, Lτ is number of loosening measures introduced in quarter τ and t0 denotes the end of 1999 as a starting point in the sample. MPP stance_HR represents the simple CNB macroprudential policy stance (MPP stance) index.

As the goal of this research is to find some evidence on whether macroprudential measures had a significant effect in reducing bank risk-taking we employ this aggregate macroprudential policy stance. By using the simple index, we have overcome the problem of heterogeneity of instruments and multi-dimensionality of their calibration. At the same time, the information from higher precision of the measurement are not taken into account. As this paper assesses mostly the time dimension of systemic risk, we find that it is appropriate to use the simple index.

The index is created according to the ECB’s Macroprudential Policies Evaluation Database (MaPPED 7). An increase in the constructed index signals net tightening while decline signals net loosening of macroprudential stance (Figure 6). Furthermore, in the sub-sample of foreign banks we also consider the evolution of MPP stance in countries that represent home countries for foreign credit institutions operating in Croatia ( MPP_stance_Home) to check for possible macroprudential policy outward spillovers from foreign banks’ home authorities. We also check for possible macroprudential policy spillovers from foreign countries onto domestic banks by constructing the variable of the MPP stance of EU countries constructed as the weighted average of individual countries’ macroprudential policy stances, where the annual GDPs of the respective economies are used as weights.

Figure 6Macroprudential policy stance index DISPLAY Figure

As mentioned above we divide control variables into two groups: macroeconomic and bank-specific variables. Descriptive statistics of bank-specific variables for the two bank sub-samples and the whole are given in Table 1.

3.4.1 Macroeconomic variables

GDP growth. Annual growth rate of quarterly real GDP serves as a proxy for demand factors in an economy. Higher GDP growth should be translated into higher demand for credit as both expectations of future developments and clients’ perceived creditworthiness improve. Moreover, we were looking into subcomponents of GDP growth, particularly focusing on private Consumption growth.

Macro factor. Although real GDP growth is a relatively suitable proxy of economic development, this can also be described by other variables such as asset price growth, unemployment dynamics and growth in wages (as can be seen in Figure 2). Unfortunately, these variables are highly correlated to each other and therefore cannot be simultaneously included into the model. In order to capture the effect of the real cycle on credit growth as accurately as possible, we estimated a latent variable Macro factor that captures the dynamics of the real cycle. The macro factor was estimated by means of time series factor analysis using the following variables: real GDP growth, real estate price growth, stock exchange indeks growth (CROBEX) and nominal net wage growth. We use time series factor analysis 8 to perform a reduction in the dimensionality of the data and combine several variables into a latent variable that represents a macroeconomic aggregate.

3.4.2 Bank-specific variables

Liquid Asset. The share of liquid assets in total assets represents the size of credit institutions’ liquidity conditions. Higher levels of liquidity in the previous period should translate into elevated lending activity in the following period. Nonetheless, this might also reflect banks’ willingness to take on risk, or their lack of it.

TCR. The bank total capital ratio represents the ratio between banks’ own funds and total risk weighted exposure. Banks with higher levels of TCR have higher credit potential as they are able to increase their credit exposure and still meet their regulatory capital requirement without the needs for recapitalization. Therefore, the expected sign of the relation is positive.

Market Share. Share of assets in total banking sector assets is a measure of a bank’s size. Market share is, in a way, a measure of bank inertia as it is much harder for larger banks to obtain high rates of credit growth than it is for smaller banks. Therefore, we expect a negative effect on credit growth.

LT Liabilities. The ratio of long-term liabilities to total liabilities, where liabilities are considered long-term if their initial maturity is longer than one year, is a measure of bank funds stability.

RIIR on Liabilities. The real implicit interest rate on liabilities is calculated as ratio of interest rate expenditures in bank’s total liabilities. It is anticipated that higher cost of funding sources would have a negative effect on credit growth.

Substitutes. Year on year change in loans and debt securities to sectors other than HH’s and NFC’s, normalized by banks’ total assets in the previous year. This variable is used to test for the existence of the crowding-out effect that can occur if lending to government and other financial institutions reduces lending to private sector. This effect could be especially pronounced in crisis period, as creditworthiness of private sector worsened while at the same time interest rates on sovereign loans and securities rose, which influenced some banks to increase sovereign lending. If the crowding-out effect is present, the expected sign is negative.

NPLR. The non-performing loan ratio is a share of partly recoverable and fully irrecoverable loans in total bank loans and represents banks’ loan quality. Increased share of distressed loans on banks’ balance sheets is expected to hamper future loan growth as they employ resources that could alternatively be used for granting new loans, so the expected sign is negative. In order to fully capture the effect of asset quality on future loan growth, the provisioned part of NPLs (Coverage) should also be taken into account. The expected sign is positive as, conditional on a certain level of NPLR, NPLs with higher coverage ratio have smaller negative effect on bank capitalization and consequently on lending activity. Moreover, we also include a Net NPLR variable that represents the share of unprovisioned NPLs in total loans and the higher values of this variable should negatively affect credit activity.

ROA. Return on assets is a measure of bank profitability, defined as ratio of income before taxes and total bank assets. The expected sign is positive as banks with better profitability can use their retained earnings to fund future loan expansion.

Table 1Descriptive statistics of bank-specific variables DISPLAY Table

4 Results

4.1 Immediate impact of MP measures on bank lending

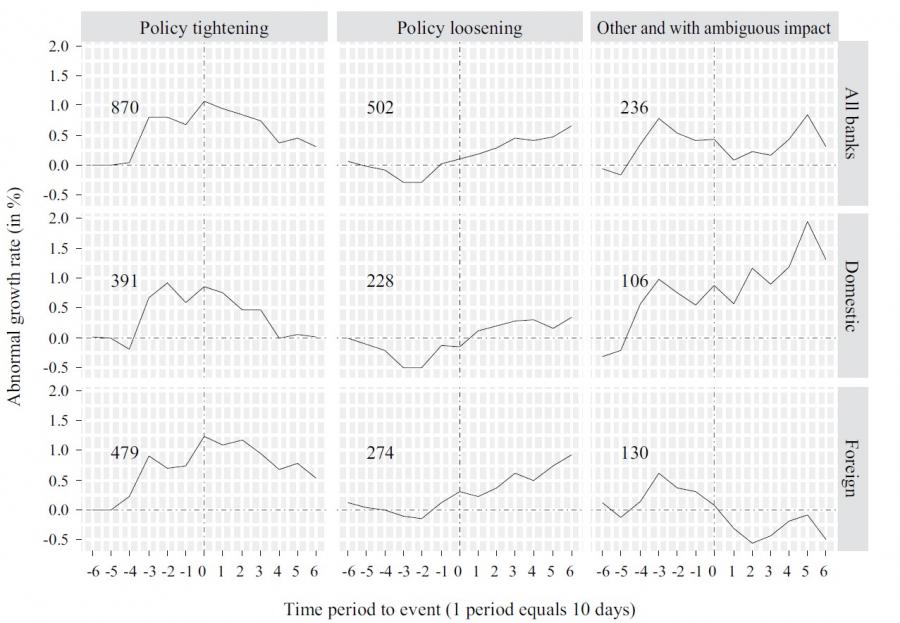

The main results of the impact analysis explained above can be found in Figure 7 and Table 2 below. Figure 7 clearly shows difference in banks’ reactions to the introduction of MP measures according to whether it was a loosening or a tightening event. The analysis also shows that the reaction of foreign owned banks was more pronounced than that of domestically owned banks, which is in line with the systemic objective of macroprudential policy. This was the case in both loosening and tightening measures. It can be seen that a few periods prior to the introduction of policy tightening measures, banks reacted procyclically, that is they increased their lending in anticipation of regulatory tightening. This temporary lending surge gradually subsided in periods after the event and the same dynamics is observed both for domestic and foreign banks, whereas a lending surge is statistically significant only for foreign banks (Table 2). A similar reaction was also observed in cases in which the CNB introduced loosening measures; foreign and domestic banks slightly increased their lending immediately after the event, whereas foreign banks reacted in a more agile fashion than domestic banks. However, statistical significance tests do not reject the null hypothesis of CAAGR being equal to zero, which does not exclude the possibility that these measures had a more pronounced impact on banks’ lending in periods that took place after the event window. A third group of measures, labelled other, with ambiguous impacts and without a clear policy direction did not have a statistically significant impact on banks’ lending.

From the policymakers’ perspective, these results affirm the importance of MP measures implementation dynamics, especially in case of policy tightening. On one hand the policymaker should announce the measure long enough in advance in order to minimise potential shocks in the market, but on the other, the longer the period between announcement and implementation, the more the room for banks to make a lending push before the measure enters into force.

Figure 7Cumulative average abnormal growth rate of banks' loans to the domestic non-financial private sector DISPLAY Figure

Table 2Statistical significance of the cumulative average abnormal growth rate of banks' loans to the domestic non-financial private sector DISPLAY Table

4.2 Overall impact of MP measures on bank lending

The main results from panel regression analysis can be found in the tables below. In particular, Table 3 and 4 depict the estimated coefficients from equation (2), while the results for model 7 presented in these tables derive from equation (3). Furthermore, we also evaluated the effect of the global financial crisis and divided the sample into a pre-crisis (1999Q4-2008Q4) and a crisis period (2009Q1-2018Q3) for both bank sub-samples. These results are presented in Table 5.

Table 3Through-the-cycle impact of macroprudential measures on foreign banks' lending DISPLAY Table

Table 4Through-the-cycle impact of macroprudential measures on domestic banks' lending DISPLAY Table

The results show that one of the major factors influencing loan growth in Croatia was the regulatory environment. The change in the MPP index, which captures the aggregate stance of macroprudential policy in Croatia, has a negative and significant effect on credit growth with more pronounced effect on foreign banks’ lending. Tightening of the CNB’s macroprudential stance on average slowed down credit growth of foreign banks by 1 p.p. and for domestic ones only by 0.4 p.p. The CNB’s macroprudential policy mix aimed at slowing down the buoyant credit growth can be rated as relatively more effective for foreign, mainly larger banks with systemic importance, which is in line with the objective of macroprudential measures, i.e. preserving the stability of the financial system. Furthermore, tightening of regulatory policies in home countries also has a significant negative effect on credit growth of foreign owned credit institutions in Croatia and that effect is comparable in size to the effect of domestic macroprudential policy actions. This result suggests that affiliated institutions’ host country regulatory environment affects the behaviour of banking groups at the consolidated level, which eventually spills over into host countries. What is more, the estimation results show that overall tightening of regulatory policies across EU countries also has an impact on the credit activity of domestic banks in Croatia, albeit at a lower intensity, suggesting that regulatory spillovers are present not only through direct the parent-daughter channel, but also through indirect channels.

The relevant macroeconomic controls used in the specification mentioned above show a consistent significant positive impact on loan dynamics only for foreign banks. This is expected, as foreign banks are mainly larger banks with a relatively broad base of customers, while domestic banks are mainly smaller banks operating in specific niches that do not necessarily correlate with macroeconomic movements. Moreover, when looking into different subcomponents of GDP, the only consistent driver of foreign bank loan growth is private consumption, as other subcomponents proved to be insignificant. Additionally, when accounting for other indicators of the real cycle, such as asset prices growth, unemployment dynamics and growth in wages, through the latent variable Macro factor, we find quite similar results.

The complementary specifications robustly confirm that the unspecified macro effect is not present in the observed time period and that with macro variables included the model captured all the relevant information.

As mentioned before, the effect of macroprudential policies can also be affected by different bank-specific variables. The results show that in order to extend credit, banks need to have sufficient liquidity. This is even more pronounced for domestic banks and can be explained by the ability of foreign owned banks to turn to their parent banks when in need of funding, while domestic banks, on the other hand, can increase credit supply only if they have sufficient liquidity reserves. Measures of capitalization, such as total capital ratio are significant only in the case of domestic banks. In addition, as expected, the further increase in credit institutions’ market share would have significantly negative effect on credit growth for both groups of banks. Moreover, the results do not corroborate the hypothesis that that a substitution effect between loans to private sector and placements to other sectors was present in Croatia, while in specifications where this relation is significant it is positive. This suggests that on average, across the sample of all banks, a “crowding in” effect was observed, i.e. along with a growth in lending to the private sector, lending to government and other financial institutions also increased. Furthermore, stable funding, measured as the share of longterm liabilities in total liabilities is somewhat more relevant for domestic banks. On the other hand, the price of banks’ funding sources had a somewhat more significantly negative effect on the credit growth of foreign banks, which is somewhat surprising, considering that domestic banks pay higher interest on their liabilities than foreign banks. This result can be explained by the notion that relatively small domestic banks value their relationships with clients more highly and are looking to extend a loan to that client despite the higher cost of its funding. We also tested how profitability affects credit growth and found out that higher profitability is one of the main prerequisites for the credit expansion of domestic banks. Profitability proves to be insignificant in the case of foreign banks, which is not surprising because they can rely on their parent bank’s support, either by means of increasing liabilities or recapitalization. Asset quality, as documented by many studies in the literature, can have a limiting effect on credit growth. Interestingly results confirm that only domestic banks are constrained by the quality of their credit portfolio, while for foreign banks only the provisioned part of NPLs is statistically significant in some specifications. The robustness of these findings was further verified by testing the relation between net NPLRs and credit growth, which yielded similar results. This is in line with our finding that the level of capitalization impacts lending only in case of domestic banks as domestic banks have on average somewhat lower levels of regulatory capital and need to watch out for possible impact of non-performing loan on their capital reserves.

Table 5Pre-crisis and crisis impact of macroprudential measures on foreign and domestic banks' lending DISPLAY Table

When differentiating between the pre-crisis and the crisis period we find that CNB macroprudential actions primarily influenced foreign banks’ lending to the private sector in the years before the crisis. Furthermore, tightening of regulatory policies in home countries also had a significant negative effect on the credit growth of foreign-owned credit institutions in Croatia in the pre-crisis period. We also confirm macroprudential policy spillovers from EU countries onto domestic banks, but only for the pre-crisis period. Results show that loan dynamics for foreign banks is influenced in years before 2009 by the level of their liquidity. Relation between macroeconomic developments and credit growth is present only in the bust phase of the economic cycle and only for domestic banks. Furthermore, in post-crisis period foreign banks’ exposures to private and other sectors increased and/or contracted in a synchronized fashion. On the other hand, for domestic banks this holds true for the pre-crisis period. Results show that in the pre-crisis period domestic banks’ lending is negatively constrained by deteriorated asset quality and increased market share. The impact of liquidity on domestic banks’ credit growth is significant from 2009 onwards, when better profitability also become relevant.

5 Conclusion

In the aftermath of the 2008 financial crisis, macroprudential measures were labelled policymakers’ best response to systemic risk and financial sector imbalances, with their effectiveness still largely unknown due to the limited use of such measures before the crisis. Croatia is a good example of a country that has employed a great variety of macroprudential measures to manage systemic risks in the economy, especially in the years before the 2008 financial crisis. In this paper, we analysed both the immediate and overall impact of macroprudential policies on foreign and domestic banks’ lending in Croatia in a 19 year period. According to estimation results, CNB macroprudential actions influenced banks’ lending to the private sector, primarily, however, affecting foreign banks’ lending, the effect on domestic banks being limited. However, these measures were primarily aimed at the supply side of lending and were not able fully to address the excessive borrowing demand from the private sector, which through regulatory arbitrage induced stronger activity in other lending sources, outside of the Croatian banking sector. As a result, the private sector incurred relatively high debt levels and this poses one of the main hurdles that need to be resolved for a new lending cycle to be set in motion. Therefore, policy makers should actively monitor both the supply and the demand side of financial intermediation. Impact analysis shows that in a few periods prior to the introduction of policy tightening measures, banks’ reacted procyclically, that is they increased their lending in anticipation of regulatory tightening. At the same time, the tightening of regulatory policies in home countries also contributed negatively to foreign banks’ lending activity in Croatia, suggesting the presence of policy spillovers from other countries’ regulation, because foreign owned banks control 90% of total banking assets in Croatia. An additional important finding is that regulatory spillovers impact not only foreign owned banks through the direct parent-daughter channel, but also other banks through indirect channels. This further emphasizes the importance of reciprocity arrangements and alignment of regulatory practices at the overall EU level.

The main conclusion of our study is that the macroprudential policies that have been heavily used in Croatia to deal with systemic risk have been relatively effective in stabilising credit growth. There is evidence that macroprudential policies have been effective in preventing the build-up of financial risks in particular for bigger banks mostly in foreign ownership. Moreover, there is some evidence that those policies helped decrease the credit risk of domestic banks as well. However, even though the CNB acted countercyclically, i.e. it loosened its macroprudential policy stance, the results show that the effectiveness of these measures in the crisis period were not as effective as in the pre-crisis period. Findings further reveal the dissimilar impact of MP measures on banks’ lending with regards to their direction, i.e. tightening or loosening, and policy makers should bear this in mind when opting for tightening of their policy stance as the reversal of that action may not match the initial impact of the measure’s introduction. These results affirm the importance of MP measures implementation dynamics, especially in the case of policy tightening, as policy makers have to find an optimal strategy that minimises room for banks to make a lending push before a measure enters into force, while avoiding causing shocks in the market. In other words, policymakers should be encouraged by the impact of macroprudential measures in the upturn phase of financial cycle, but also be aware of their limitations in the downturn phase ofcycle. As far as the results indicate, after a crisis has occurred, in order to revive the financial intermediation of banks, one cannot rely only on the loosening of macroprudential policy, as other policies need to be involved.

As a final point, our results suggest that the choice of the macroprudential instrument is non-trivial and should take into account the asymmetric effects of each instrument in order to utilize the most effective policy at hand for the chosen objective. Therefore, further exploration of this topic would be great public interest. In analysing the interconnectedness of macroprudential topics with other policies and their different effect in the boom and bust phases of the economy, data that are more granular would be required. Filling the, still existing, data gaps would also help to develop mechanisms to identify and monitor overall country systemic risk and measure efficiency in a more detailed approach, measure by measure, which is essential to make macroprudential policy operational.

Notes

* The authors would like to thank two anonymous referees for their useful comments and suggestions. The views expressed in this paper are those of the authors and do not necessarily reflect the views of the Croatian Financial Services Supervisory Agency or European Central Bank.

1 In the late 1990s, the government decided to privatize banks. Consequently, the share of foreign owned banks in total assets rose from 6.7% in 1998 to around 90% in 2001 and has remained at this level ever since.

2 CEE countries include Bulgaria, Czech Republic, Estonia, Hungary, Latvia, Lithuania, Poland, Romania, Slovenia and Slovakia.

3 The number of eliminated outliers amounted to 26, which represents around 1.2% of total observations in the full sample. Furthermore, eliminated outliers were scattered across both time and bank dimensions of the sample and therefore it is assessed that their elimination should not impose bias into final results.

4 The Hausman test was performed and statistical evidence for the use of fixed effects approach was found. The results are available on request from the authors.

5 We refer to the whole period from 2009Q1 to 2018Q3 as the crisis period, although not all this period can be considered as crisis. The recession in Croatia lasted until 2015 and credit activity has been showing signs of recovery since 2017 (only on transactional basis).

6 The results are available on request from the authors.

7 More details about MaPPED available in Budnik and Kleibl (2018a and 2018b).